Choosing the right Social Security claiming age is the single most powerful lever you have to maximize your guaranteed retirement income. By understanding the profound financial differences between claiming Social Security at 62 versus waiting until 70, you empower yourself to build a strategy that perfectly supports your lifestyle goals. Claiming early offers immediate access to cash for travel or early retirement, while delaying guarantees the absolute highest monthly payout to protect against inflation and outliving your savings. Navigating this decision requires looking closely at your health, your savings, and your long-term vision. The following side-by-side breakdown gives you the clarity you need to confidently step into this exciting new chapter of your life.

Tip #1: Understand the Baseline of Your Full Retirement Age (FRA)

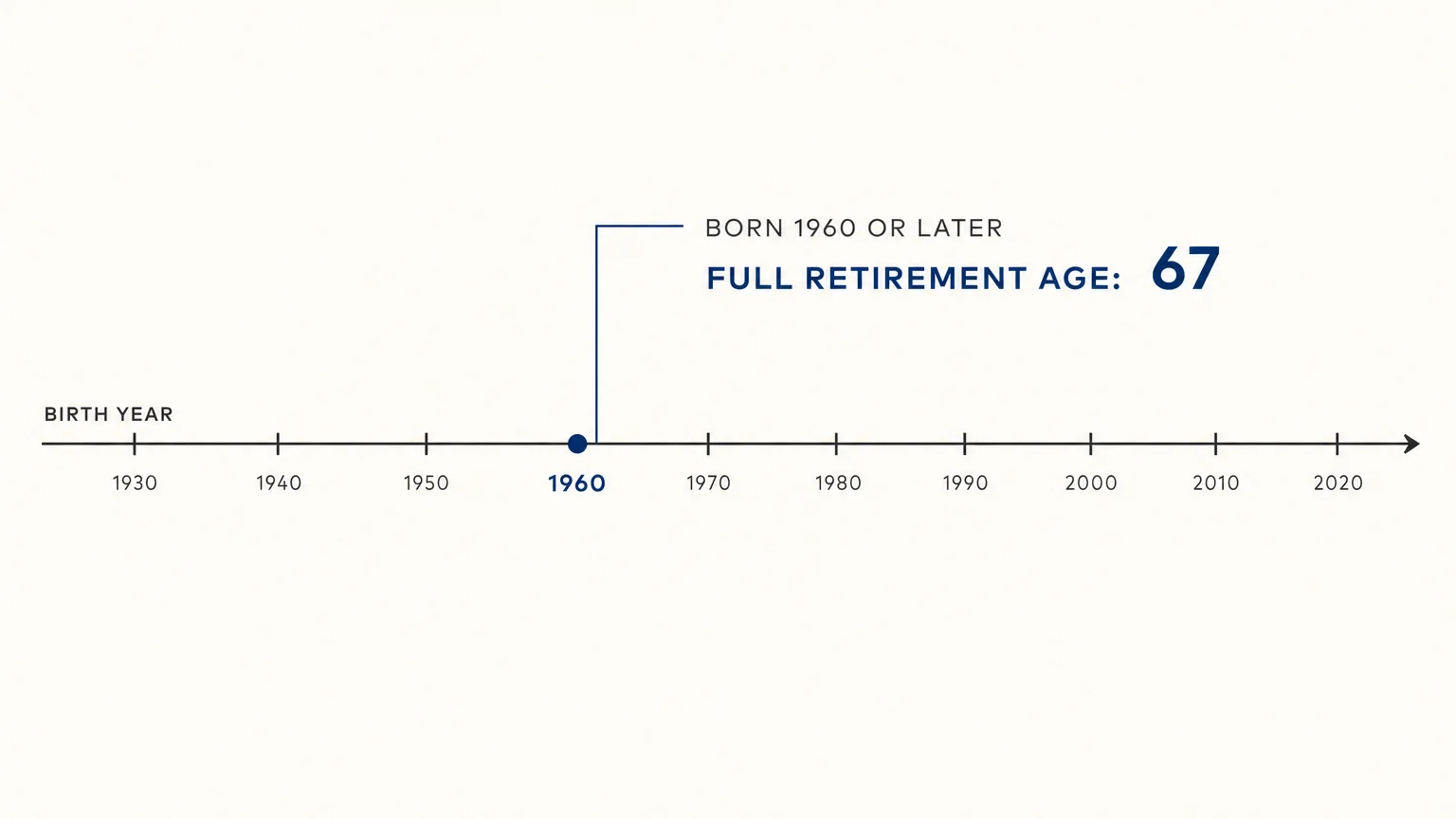

Before you compare the extremes of taking benefits at the earliest or latest possible dates, you must establish your personal baseline. The Social Security Administration uses your Full Retirement Age to determine your primary insurance amount. This specific dollar figure represents the exact monthly benefit you receive if you claim at your designated target age. Depending on your birth year, your Full Retirement Age lands anywhere from 66 to 67. Anyone born in 1960 or later reaches Full Retirement Age at exactly 67.

Knowing this exact age allows you to make an accurate, informed comparison between your various options. Think of your Full Retirement Age as the foundational anchor point of your entire retirement strategy. When you claim earlier than this anchor, you face permanent financial reductions. When you delay past this anchor, you earn permanent financial increases. Without knowing your baseline, calculating your potential future income becomes a guessing game.

You can find your specific Full Retirement Age by creating a free account on the official Social Security website and viewing your personalized statement. Reviewing your statement annually helps you keep track of your earned credits and your projected payouts. Securing this foundational number gives you the confidence to start mapping out your timeline. Taking the time to verify your primary insurance amount completely transforms how you view your future financial landscape.

Many people mistakenly assume they can receive their full benefit at age 65 simply because that is the eligibility age for Medicare. Separating your Medicare timeline from your Social Security claiming age prevents incredibly costly miscalculations. You gain immense peace of mind when you build your plans around accurate, personalized data rather than outdated assumptions.

Tip #2: Calculate the Cost of Claiming Social Security at 62

Choosing to claim Social Security at 62 opens the door to immediate financial freedom, but it comes with a steep, permanent cost. The age of 62 represents the absolute earliest opportunity you have to start receiving your retirement benefits. Stepping away from the workforce at this age gives you the precious time and energy to travel the world, pursue neglected hobbies, or spend irreplaceable years watching your grandchildren grow.

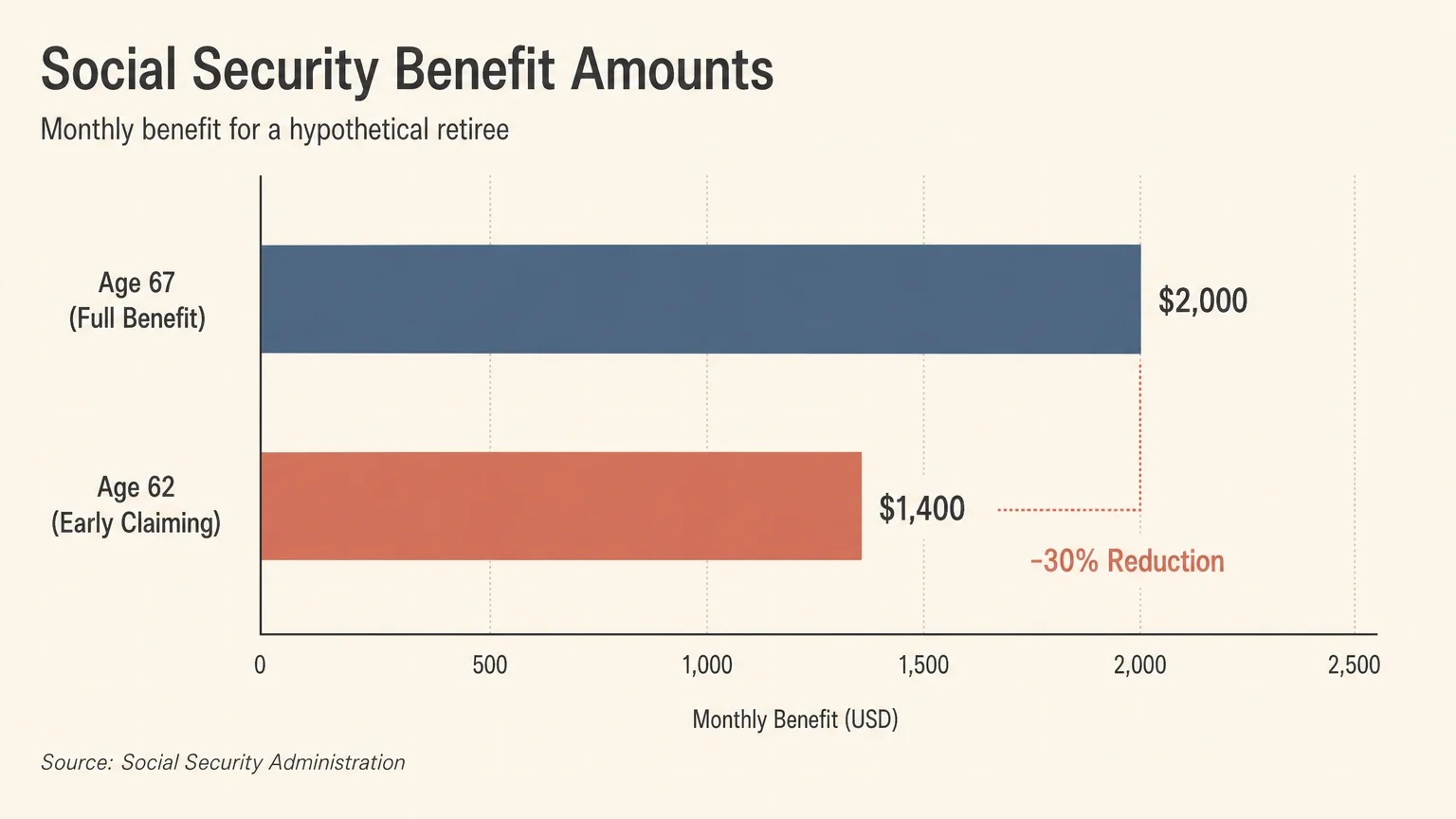

However, the system reduces your monthly payout significantly for every single month you claim before reaching your Full Retirement Age. If your Full Retirement Age is 67, claiming at 62 slashes your monthly checks by a full 30 percent. If your primary insurance amount sits at two thousand dollars, claiming at 62 drops your actual monthly income to just fourteen hundred dollars. You must accept this reduced amount for the rest of your life; it does not automatically reset to the higher amount when you turn 67.

You must also closely consider the annual earnings limit if you plan to continue working while receiving early benefits. The government withholds a portion of your benefits if your income from a job exceeds a specific threshold prior to your Full Retirement Age. This temporary withholding often catches ambitious part-time workers entirely by surprise, disrupting their expected cash flow.

Claiming at 62 works best if you plan to fully retire immediately, have significant health concerns that limit your life expectancy, or possess enough supplementary investments to offset the smaller monthly checks. If you have built a massive nest egg and simply want the government to start paying you back as soon as possible, claiming early provides a steady, immediate stream of supplemental cash.

Tip #3: Measure the Maximum Growth of Social Security at 70

Waiting to claim Social Security at 70 represents the ultimate strategy for maximizing your guaranteed, lifelong monthly income. The government rewards your immense patience by adding delayed retirement credits to your baseline benefit for every single month you wait past your Full Retirement Age. These highly valuable credits accumulate at a guaranteed rate of 8 percent per year.

If your Full Retirement Age is 67, delaying your claim until 70 results in a massive 24 percent increase above your primary insurance amount. Using the previous example, your two thousand dollar baseline benefit surges to two thousand four hundred and eighty dollars per month. This substantially increased amount serves as a powerful defense against inflation, ensuring your purchasing power remains unshakeable well into your later decades.

This guaranteed 8 percent annual growth vastly outperforms the conservative returns you might find in certificates of deposit, standard bonds, or traditional savings accounts. Furthermore, the annual cost-of-living adjustments apply directly to this higher baseline, meaning your yearly raises grow exponentially larger over time. You simply cannot find another guaranteed, government-backed investment that yields such consistent, risk-free growth.

You should heavily consider waiting until 70 if you enjoy excellent physical health, possess a strong family history of longevity, and have the financial means to comfortably support yourself during the gap years. Delaying your claim removes the anxiety of outliving your money, giving you the freedom to spend your savings confidently in your later years.

Tip #4: Factor in Your Break-Even Point

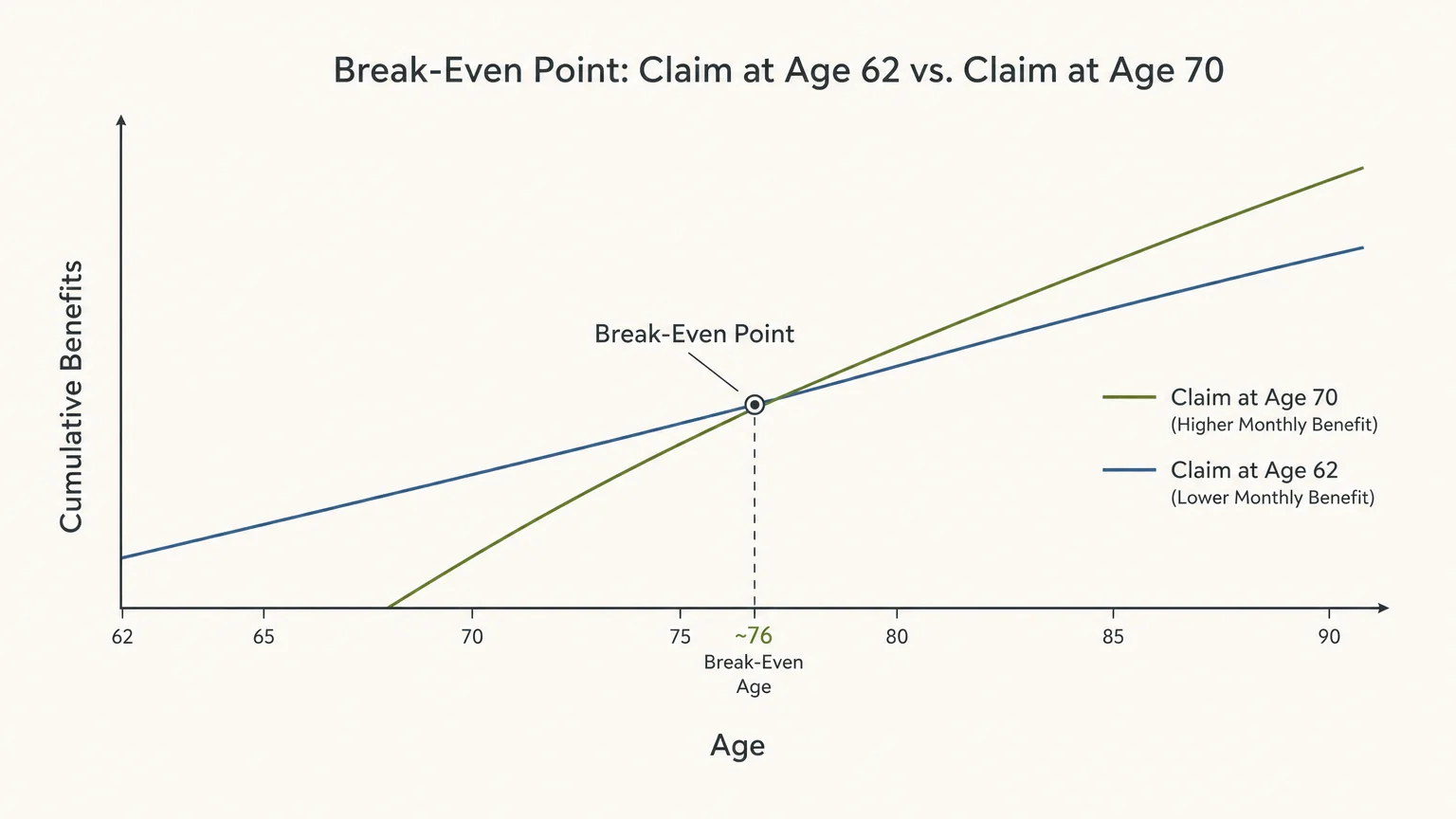

Comparing early and delayed claims requires you to deeply examine the mathematical concept of the break-even point. The break-even point highlights the exact age when the total accumulated dollars from a delayed, higher payout finally surpass the total accumulated dollars from an early, lower payout. Knowing this crossover age allows you to frame your final decision around realistic life expectancy rather than just monthly amounts.

When you claim at 62, you receive eight full years of monthly checks before the 70-year-old claimant receives a single dime. Those eight years of early income create a massive, undeniable financial head start. If you receive fourteen hundred dollars a month starting at 62, you collect over one hundred and thirty-four thousand dollars by the time you reach your seventieth birthday.

The person who bravely waited until 70 must live long enough for their larger monthly checks to make up for that lost time and missed income. In most standard scenarios, the break-even age falls somewhere between 78 and 82. If you expect to live vibrantly well into your late eighties or nineties, delaying to 70 provides far more total wealth over your lifetime.

Conversely, if chronic health issues suggest a significantly shorter life expectancy, claiming early ensures you actually get to enjoy the money you paid into the system over your working career. Understanding the break-even math prevents you from making a purely emotional choice, anchoring your strategy in practical, long-term realities.

Tip #5: Align Your Claiming Age with Your Spousal Benefits and Legacy Goals

Your Social Security claiming age directly impacts your spouse, making this a crucial joint decision rather than an isolated, individual choice. Married couples have the unique opportunity to strategically coordinate their applications to maximize both immediate household income and long-term survivor protection. You must look at how your respective work histories and projected benefit amounts interact with one another.

The survivor benefit rules heavily favor the strategy of having the higher-earning spouse delay their claim for as long as possible. When one spouse passes away, the surviving widow or widower automatically inherits the highest single benefit between the two individuals. If the higher earner waits to claim Social Security at 70, they permanently lock in the absolute highest possible survivor benefit for their partner.

This approach provides incredible security for a surviving spouse who might face decades of living expenses alone, ensuring they do not experience a drastic drop in their standard of living. Meanwhile, the lower-earning spouse might choose to claim their own benefit at 62 to generate immediate, helpful household income, knowing the higher earner’s maximum benefit will eventually protect the surviving partner.

Discussing these profound legacy goals together ensures that both of you feel secure, valued, and confident about your shared financial future. Navigating spousal benefits requires open communication and a clear understanding of how one person’s timeline dictates the other person’s safety net.

Tip #6: Evaluate Your Health and Family Longevity History

Numbers, spreadsheets, and financial calculations only tell half the story when it comes to determining your ideal claiming age. You must take an honest, highly objective look at your personal health profile and your family’s distinct history of longevity. Your body often dictates the most practical timeline for stepping away from the intense demands of full-time employment.

If you face ongoing chronic conditions, experience rapidly declining energy levels, or have a family history of shorter lifespans, claiming early provides the immediate resources you need to enjoy your most active years. You entirely deserve to use your hard-earned benefits to fund memorable vacations, engaging hobbies, and joyful family gatherings while you still have the physical stamina to participate fully.

Ignoring obvious health realities in the rigid pursuit of a larger future payout often leads to deeply regrettable missed opportunities. Your golden years should be defined by the quality of your experiences, not just the quantity of dollars in your bank account.

On the other hand, if your parents and grandparents lived vibrantly into their nineties, you face a significant, legitimate risk of outliving your personal investment portfolio. A long, active life requires a highly robust, inflation-protected income stream. In this scenario, delaying your claim acts as the ultimate longevity insurance—you essentially buy an annuity that pays out indefinitely, safeguarding your lifestyle against the financial drain of an extended, beautifully long retirement.

Tip #7: Build a Strategic Bridge to Support Your Retirement Income

Deciding to delay your benefits requires a remarkably solid, actionable plan to generate cash flow during the inevitable waiting period. You must build a secure income bridge that successfully carries you from your final day of work to the day you finally claim your maximized Social Security check. This bridge strategy protects your current lifestyle while allowing your government benefits to grow untouched behind the scenes.

You can effectively fund this critical gap period by intelligently tapping into your personal investment accounts, such as your 401(k), traditional IRA, or standard brokerage accounts. Drawing down these specific accounts early in retirement reduces your future required minimum distributions, which can drastically lower your overall tax burden later in life. You can work closely with a financial advisor to determine the optimal, safe withdrawal rate that sustains your household without depleting your principal too quickly.

Many modern retirees also successfully choose to work part-time, consult in their former industry, or monetize a lifelong passion project during these bridge years. This gentle, phased approach to retirement provides just enough cash flow to cover your daily expenses without the overwhelming stress of a forty-hour corporate workweek.

By purposefully and carefully designing this financial bridge, you grant yourself immense flexibility. You give your future self the profound, life-altering gift of a fully maximized, stress-free, lifelong retirement income.

The Takeaway: Living a More Blissful Retirement

Navigating the complex landscape of Social Security requires careful thought, highly strategic planning, and a deep understanding of your personal goals. You now possess the absolute clarity needed to intelligently weigh the immediate gratification of an early claim against the immense, long-term financial security of a delayed application. Every rule, mathematical calculation, and percentage points back to one singular, beautiful truth: you have the complete power to design a future that brings you deep joy and unshakeable peace of mind.

Take the necessary time to crunch your personal numbers, review your health realistically, and talk openly with your loved ones about your shared vision. You do not have to rush this monumental decision. By thoughtfully aligning your financial strategy with your most ambitious lifestyle dreams, you enthusiastically set the stage for a deeply rewarding, thoroughly secure, and profoundly blissful next chapter of your life.

Frequently Asked Questions

Can I change my mind after claiming Social Security at 62?

You have a remarkably forgiving safety net if you experience buyer’s remorse after claiming early. The Social Security Administration allows you one strict opportunity to entirely withdraw your application within the first twelve months of receiving benefits. You must completely repay every single dollar you and your family received during that period. Once you repay the funds in full, your record resets entirely, allowing your benefits to grow again as if you had never applied in the first place.

Does working affect my retirement benefits if I claim early?

Working absolutely affects your monthly checks if you claim before reaching your Full Retirement Age. The government imposes a strict annual earnings limit on early claimants. If your job pays you more than this specific, yearly limit, the administration withholds a significant portion of your benefit check. However, these withheld funds do not disappear forever; your monthly payout increases slightly once you finally reach your Full Retirement Age to account for those previously withheld months.

Are Social Security benefits taxed?

Depending on your overall financial picture, the federal government may indeed tax a portion of your benefits. You must accurately calculate your combined income, which includes your adjusted gross income, your nontaxable interest, and exactly half of your Social Security payout. If this combined total exceeds certain IRS thresholds, you could pay income taxes on up to 85 percent of your benefits. Proactive tax planning strongly helps you manage these liabilities effectively.

How does my claiming age affect Medicare eligibility?

Your Medicare eligibility remains completely separate from your personal decision regarding when to claim your retirement income. You become fully eligible for Medicare at age 65, regardless of whether you claimed cash benefits at 62 or bravely plan to wait until 70. You must proactively enroll in Medicare during your initial enrollment period around your 65th birthday to avoid permanent, costly late penalties, even if you are delaying your monthly Social Security checks.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply