Managing your healthcare expenses is a vital part of keeping your retirement years comfortable, secure, and completely blissful. For 2026, the Centers for Medicare & Medicaid Services updated several baseline costs, meaning you need to adjust your financial strategy now. While standard premiums have climbed as expected, the truly hidden expenses lie deeper within your coverage details. You can easily outsmart these hikes by learning exactly where the increases occurred and how they affect your wallet. Understanding these five specific Medicare cost changes empowers you to safeguard your savings and avoid shocking bills. Let us dive directly into the 2026 numbers so you can protect your hard-earned nest egg and focus entirely on enjoying your well-deserved free time.

Tip #1: Prepare for the Part A Hospital Deductible Increase

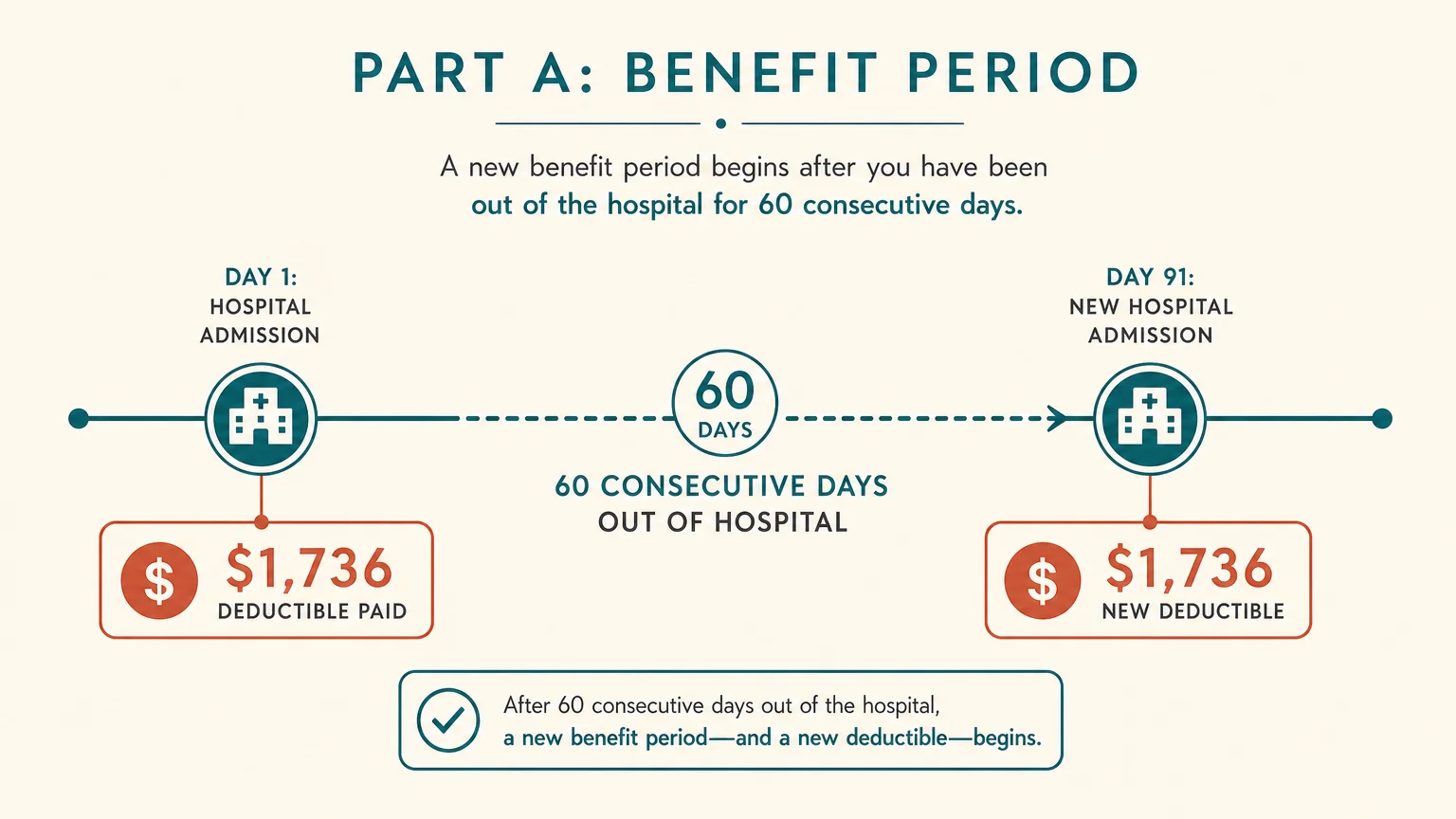

Original Medicare Part A covers inpatient hospital stays, skilled nursing facility care, and some home health services. You likely paid into Medicare during your entire career, which means you enjoy premium-free Part A. However, free premiums do not guarantee a free hospital stay. If you need inpatient care in 2026, you face a new Part A deductible of $1,736 per benefit period.

This represents a notable increase from previous years—and the specific structure of this deductible often confuses retirees. Unlike typical auto or home insurance, Medicare Part A does not use a simple annual deductible. Instead, it relies on benefit periods.

A benefit period begins the day you enter a hospital or a skilled nursing facility. It ends only when you go 60 consecutive days without receiving any inpatient care. Consider a practical scenario. Imagine you enter the hospital in February for a knee replacement. You pay the $1,736 deductible, recover beautifully, and go home. Six months later, you contract severe pneumonia and require another hospital admission. Because more than 60 days passed since your last stay, a brand-new benefit period begins. You owe another $1,736 before Medicare pays a dime.

You can easily protect your savings from this recurring cost. Supplemental insurance policies—commonly known as Medigap—often cover the Part A deductible entirely. If you prefer a Medicare Advantage plan, your hospital costs will convert into daily copayments rather than a single massive deductible.

Review your current coverage to understand exactly how it handles inpatient care. A sudden illness or planned surgery should never derail your financial peace of mind. Knowing your exposure to the $1,736 deductible allows you to set aside emergency funds or purchase the right protective policy. By taking these proactive steps, you guarantee a more relaxed retirement free from medical billing anxiety.

Maintaining a proactive approach to your coverage changes everything.

Tip #2: Adjust Your Budget for the Part B Premium Bump

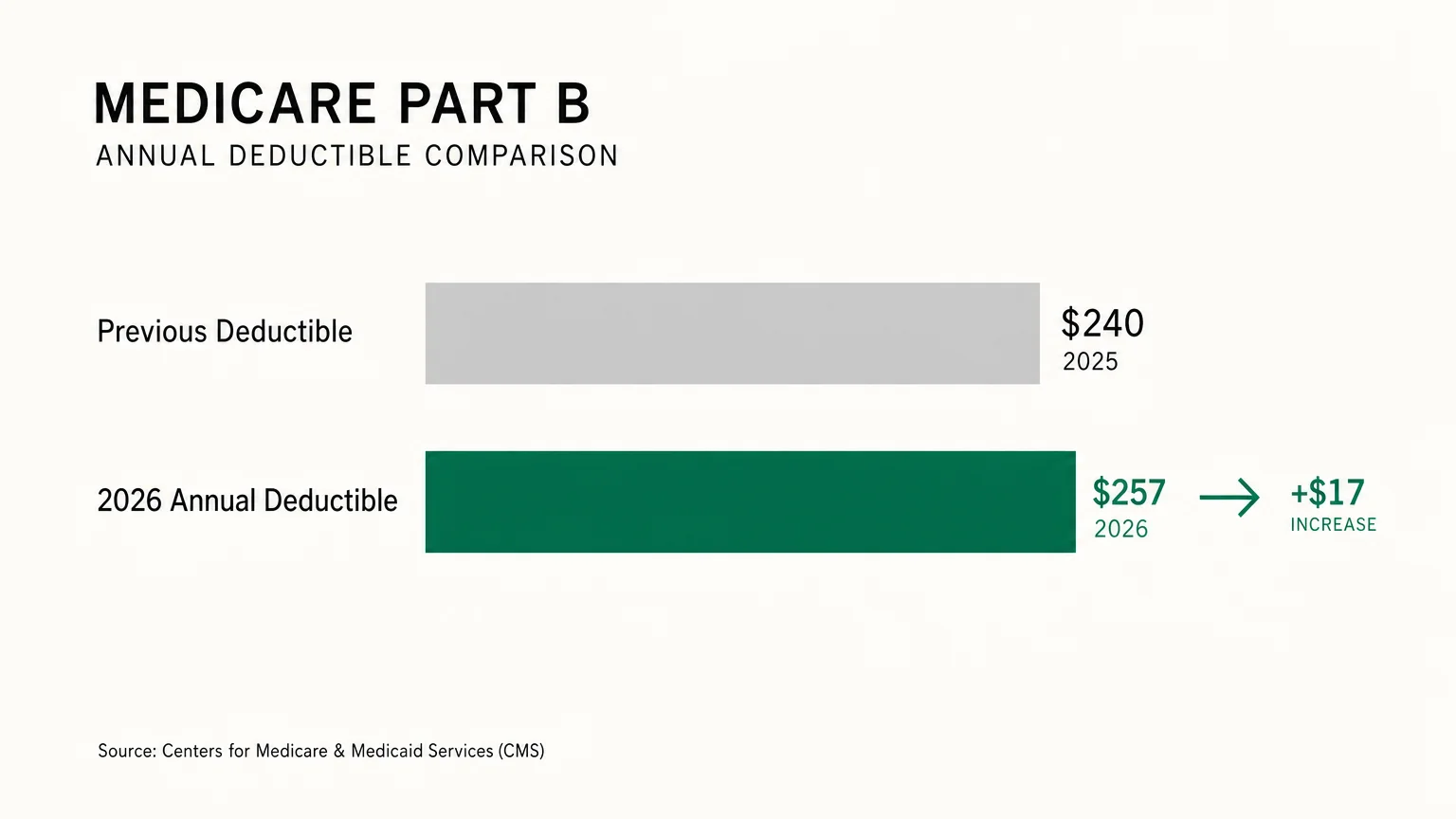

Medicare Part B serves as your primary health insurance for everyday needs. It covers outpatient care, doctor visits, preventive services, and durable medical equipment. Unlike Part A, Part B requires a monthly premium. For 2026, the standard base premium sits at $202.90 per month.

This increase stems from overall inflation and rising medical utilization across the country. The government deducts this premium directly from your monthly Social Security benefit check. When the Social Security Administration announces the annual Cost of Living Adjustment, many retirees celebrate the prospect of a larger check. Unfortunately, the simultaneous increase in the Part B premium quickly swallows a portion of that raise. You might see a lower net increase in your bank account than you originally anticipated.

Do not let this mathematical reality discourage you. You possess several tools to manage this expense. First, reevaluate your monthly household budget to reflect the exact $202.90 deduction. Knowing your precise net income prevents accidental overspending.

Second, investigate Medicare Savings Programs in your state. If you live on a fixed or limited income, your state Medicaid office might pay your Part B premium on your behalf. These programs use specific income and asset thresholds, but they provide massive relief if you qualify.

Finally, keep in mind that skipping Part B enrollment to save money usually backfires. Unless you maintain creditable coverage from a current employer, delaying Part B triggers a permanent late enrollment penalty. Your premium would increase by 10% for every full 12-month period you could have had Part B but chose not to sign up. Paying the $202.90 on time protects you from lifelong financial penalties and ensures your doctors remain accessible whenever you need them.

Staying informed about your responsibilities prevents early-year billing stress.

Tip #3: Factor in the New Part B Annual Deductible

Beyond your monthly premium, Medicare Part B carries its own distinct deductible. For 2026, you must pay $283 out of your own pocket before Original Medicare begins covering its standard share of your medical bills.

While $283 may not sound like a catastrophic amount, it represents a mandatory threshold you must cross at the beginning of every calendar year. If you schedule a specialist visit or order diagnostic lab tests in January, you will bear the full brunt of the bill up to that $283 limit.

Many seniors mistakenly believe their Medigap plans will catch this deductible. However, modern regulations prohibit newly sold Medigap policies from covering the Part B deductible. Popular options like Medigap Plan G cover nearly every other out-of-pocket expense, but they legally cannot pay that initial $283 for you.

Let us look at a real-world scenario. You visit a cardiologist in early February for a comprehensive evaluation, and the approved cost is $400. Because you have not met your Part B deductible yet, you pay the first $283 entirely on your own. The remaining $117 is split between Medicare and you; Medicare pays 80%, and you pay the remaining 20% coinsurance. For all subsequent outpatient visits during the year, that initial $283 barrier disappears.

You can handle this cost smoothly by incorporating it into your post-holiday financial planning. Treat the Part B deductible as an expected January expense. Set aside a small healthcare fund during the previous fall. When the new year arrives, you will pay those early medical invoices without dipping into your grocery or leisure budgets. Anticipating this front-loaded expense keeps your financial anxiety low.

Protecting your assets requires looking closely at income-based rules.

Tip #4: Watch Out for IRMAA Income Surcharges

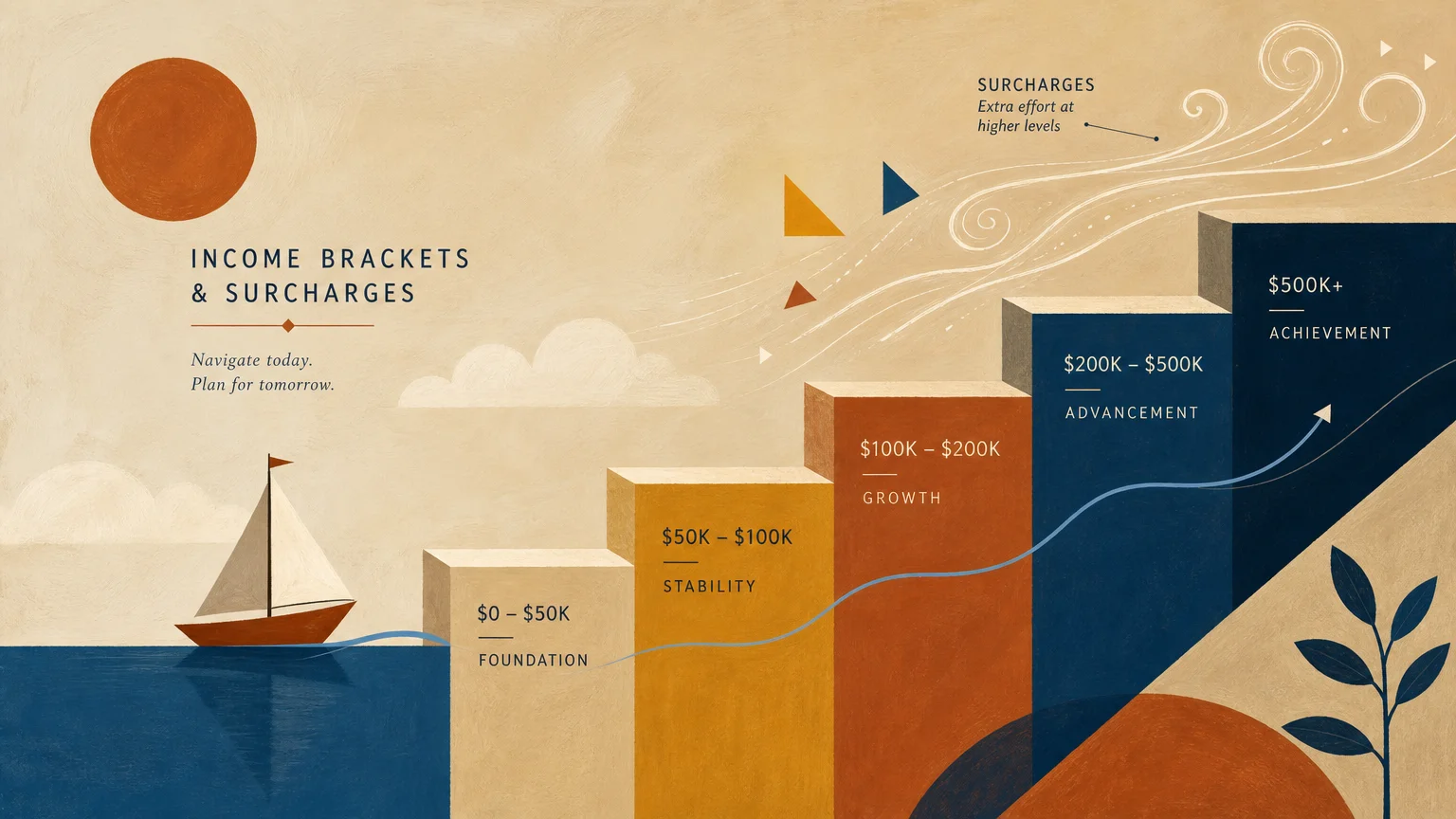

If you worked hard to build a robust retirement portfolio, your financial success might trigger an invisible Medicare penalty. The government uses the Income-Related Monthly Adjustment Amount—commonly known as IRMAA—to charge higher earners more for their Medicare Part B and Part D coverage.

In 2026, IRMAA surcharges kick in if you file an individual tax return with an income above $109,000, or a joint return exceeding $218,000. If you cross these thresholds by even a single dollar, your standard $202.90 premium multiplies rapidly. High earners can easily pay hundreds of dollars more each month for the exact same medical coverage.

The Social Security Administration determines your IRMAA status by looking at your tax returns from two years prior. Therefore, your 2026 premiums depend directly on the income you reported to the IRS in 2024.

This two-year lookback period creates a frustrating trap for new retirees. If you sold a home, converted a traditional IRA to a Roth IRA, or received a large severance package in 2024, your income spiked artificially. The government sees that high number and assigns you a hefty IRMAA surcharge for 2026, even if your current actual income has plummeted.

Fortunately, you do not have to accept this surcharge passively. You can fight an unfair IRMAA assessment by filing form SSA-44. This form allows you to report a life-changing event. Recognized events include retiring from your job, losing a pension, going through a divorce, or experiencing the death of a spouse.

When you file this appeal, you instruct the government to calculate your premiums using your current, lower income rather than your inflated historical tax return. Winning an IRMAA appeal saves you thousands of dollars. Stay vigilant about the letters you receive from Social Security and challenge any surcharges that do not reflect your real financial situation today.

Looking past the standard monthly charges reveals the true cost of care.

Tip #5: The Biggest Surprise? Your Prescription Drug and Coinsurance Gaps

We have examined premiums and deductibles, but these predictable costs are rarely the ones that derail a retiree’s budget. The biggest financial surprises in 2026 stem from uncapped coinsurance and shifting prescription drug limits.

Original Medicare covers 80% of your outpatient costs, leaving you responsible for the remaining 20%. A 20% coinsurance sounds reasonable for a simple blood test. However, if you require weekly chemotherapy, expensive biological injections, or prolonged physical therapy, that 20% transforms into thousands of dollars. Original Medicare contains absolutely no maximum out-of-pocket limit; your liability is essentially infinite.

To cap this financial risk, many seniors turn to Medicare Advantage plans or Medigap policies. While these plans provide a crucial safety net, they introduce their own surprises. In 2026, many Medicare Advantage plans altered their internal cost-sharing structures. You might discover that the copay for a specialist visit doubled; similarly, the out-of-pocket maximum on your Advantage plan may have increased significantly.

Furthermore, Medicare Part D prescription drug coverage brings unique challenges this year. Changes to federal healthcare laws restructured how drug plans handle catastrophic costs and out-of-pocket maximums. While new caps protect you from massive pharmacy bills, insurance companies responded by tweaking their formularies. A medication you took affordably in 2025 might jump to a higher, more expensive pricing tier in 2026.

You must actively defend your budget against these hidden gaps. Never let your Medicare coverage automatically renew without a thorough review. Use the Annual Enrollment Period each fall to compare your current plan against new market offerings. Input your daily medications into the Medicare Plan Finder tool to ensure your specific prescriptions remain affordable. By aggressive shopping, you neutralize the biggest surprises Medicare throws your way.

A few simple adjustments allow you to embrace your golden years fully.

The Takeaway: Living a More Blissful Retirement

Navigating the landscape of 2026 Medicare costs requires attention, but it should never cause you stress. You worked diligently for decades to reach this exciting chapter of life. A few practical adjustments to your healthcare budget simply ensure that your nest egg remains intact and your focus stays exactly where it belongs—on enjoying your freedom.

Remember that you hold the power to control your healthcare expenses. By preparing for the Part A deductible, budgeting for your Part B premium, saving for the Part B deductible, monitoring your IRMAA status, and actively reviewing your prescription drug coverage, you build an impenetrable fortress around your finances.

Take an hour this week to review your medical statements and your current policy documents. Knowledge is your ultimate shield against surprise bills. Once you organize your strategy, you can step outside, enjoy a beautiful afternoon, and truly embrace the blissful, worry-free retirement you deserve.

Reviewing common concerns clarifies the complex world of health coverage.

Frequently Asked Questions

Can I negotiate my Medicare costs?

You cannot negotiate the base premiums or deductibles set by the federal government for Original Medicare. However, you absolutely control your overall healthcare costs for seniors by comparing private Medicare Advantage and Part D plans. Different insurance carriers charge vastly different amounts for copays and drug tiers, giving you the power to choose the most affordable option for your specific needs.

When can I change my Medicare plan to save money?

The best time to adjust your coverage and lower your Medicare expenses is during the Annual Enrollment Period, which runs from October 15 to December 7 every year. Changes made during this window take effect on January 1 of the following year. Additionally, Medicare Advantage enrollees can switch plans during the Medicare Advantage Open Enrollment Period from January 1 to March 31.

Does a Medigap policy cover the Part B deductible?

No currently available Medigap policy covers the $283 Part B deductible for new enrollees. Federal law changed to prohibit first-dollar coverage on Part B. Plans like Medigap Plan G will happily cover your 20% coinsurance and excess charges, but you must pay the initial $283 deductible out of your own pocket.

Will the Social Security adjustment cover my 2026 premium increase?

In most cases, the Social Security Cost of Living Adjustment provides a dollar increase large enough to cover the jump in your retiree healthcare premiums. The standard hold-harmless provision also prevents your standard Part B premium from reducing your net Social Security benefit below what you received the previous year. However, you will likely see a smaller net gain in your check than the full adjustment percentage suggests.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply