Turning 73 marks a major financial milestone that directly impacts your retirement tax planning and overall wealth preservation. Thanks to the recent SECURE 2.0 Act, age 73 is the exact point when the IRS mandates you to begin taking Required Minimum Distributions from your traditional IRAs and 401(k) accounts. Navigating these new RMD rules can feel overwhelming, but smart tax preparation prevents you from paying unnecessary penalties or inflating your Medicare premiums. By strategically managing your account withdrawals and exploring charitable giving strategies, you protect your hard-earned savings. Master these five essential tax moves this year to secure a financially stable, predictable, and thriving retirement.

Tip #1: Calculate and Schedule Your First Required Minimum Distribution

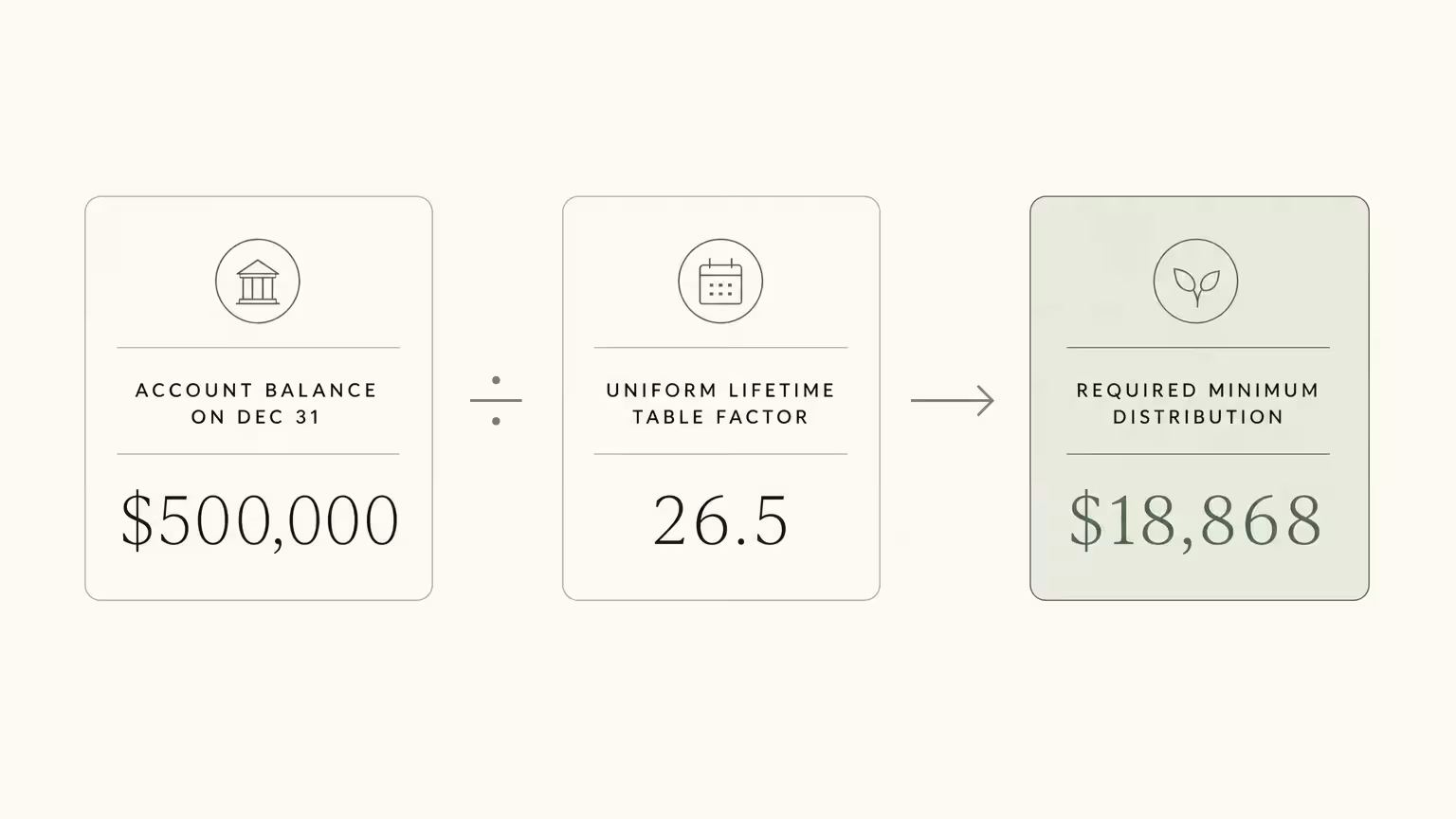

At age 73, the federal government requires you to start withdrawing a specific minimum amount from your tax-deferred retirement accounts each year. This rule applies to traditional IRAs, SEP IRAs, SIMPLE IRAs, and most 401(k) plans. Congress designed these Required Minimum Distributions (RMDs) to ensure that tax-advantaged savings are eventually subject to income tax. The exact amount you must withdraw depends on your account balance on December 31 of the previous year, divided by a life expectancy factor found in the IRS Uniform Lifetime Table.

For example, if your traditional IRA held $500,000 at the end of last year and your distribution period factor is 26.5, your required withdrawal for the current year equals roughly $18,868. You must calculate this figure accurately because the IRS imposes strict penalties for underpayment. Historically, missing an RMD resulted in a punishing 50 percent excise tax on the shortfall. The SECURE 2.0 Act recently reduced this penalty to 25 percent, and it drops further to 10 percent if you correct the mistake within a timely two-year window.

You also face an important decision regarding the timing of your first distribution. The IRS grants you a grace period for your very first RMD, allowing you to delay the withdrawal until April 1 of the year following your 73rd birthday. However, if you choose this delay, you must still take your second RMD by December 31 of that same year. Taking two distributions in a single calendar year can artificially inflate your taxable income; this might push you into a higher tax bracket and trigger other unintended financial consequences. Most financial professionals recommend taking your first distribution during the year you actually turn 73 to spread out your tax liability evenly.

Tip #2: Utilize Qualified Charitable Distributions to Lower Taxable Income

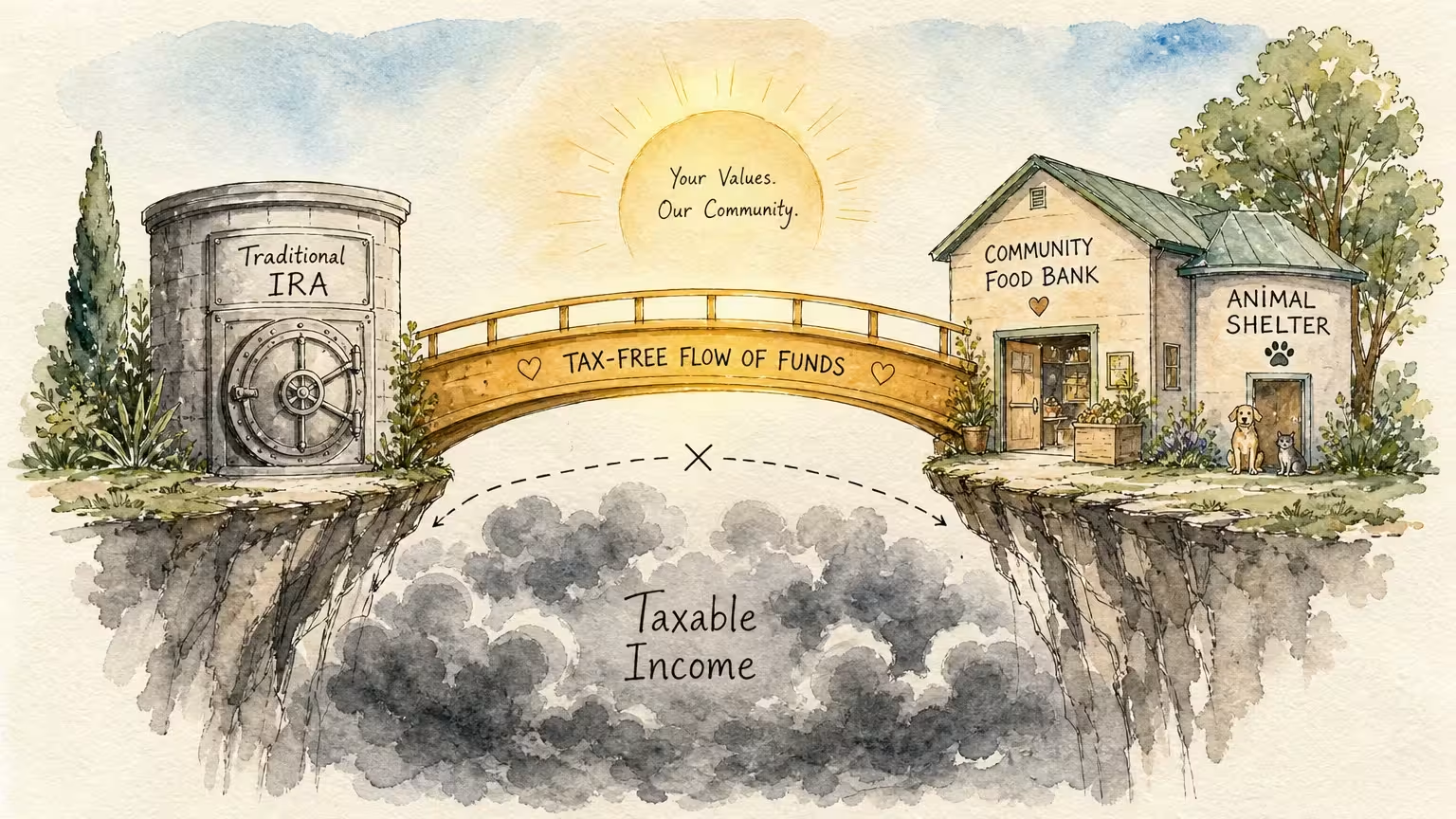

Philanthropy often plays a beautiful role in retirement planning, and reaching age 73 unlocks one of the most powerful charitable tax strategies available. A Qualified Charitable Distribution (QCD) allows you to transfer funds directly from your IRA to an eligible 501(c)(3) nonprofit organization. The IRS permits you to move up to $105,000 annually—a figure now indexed for inflation—completely tax-free.

This strategy shines brilliantly when you reach RMD age. Every dollar you send to charity through a QCD counts toward satisfying your mandatory distribution for the year, but those dollars never appear in your Adjusted Gross Income (AGI). Because recent tax law changes nearly doubled the standard deduction, many retirees no longer itemize their taxes. If you take the standard deduction and write a personal check to a charity, you receive no additional tax benefit. A QCD bypasses this problem entirely by removing the charitable gift from your taxable income before it ever hits your tax return.

Consider a retiree who needs to take a $20,000 RMD but already plans to give $5,000 to a local food bank and an animal shelter. By using a QCD for the $5,000 donation, they only report $15,000 of taxable income from their IRA. To execute this move correctly, the money must flow directly from your IRA custodian to the charity. If the institution deposits the funds into your personal checking account first, the distribution becomes fully taxable, and you lose the unique tax advantage. Reach out to your brokerage firm to request the specific QCD paperwork or a dedicated checkbook tied to your IRA.

Tip #3: Monitor Your Income to Avoid Medicare IRMAA Surcharges

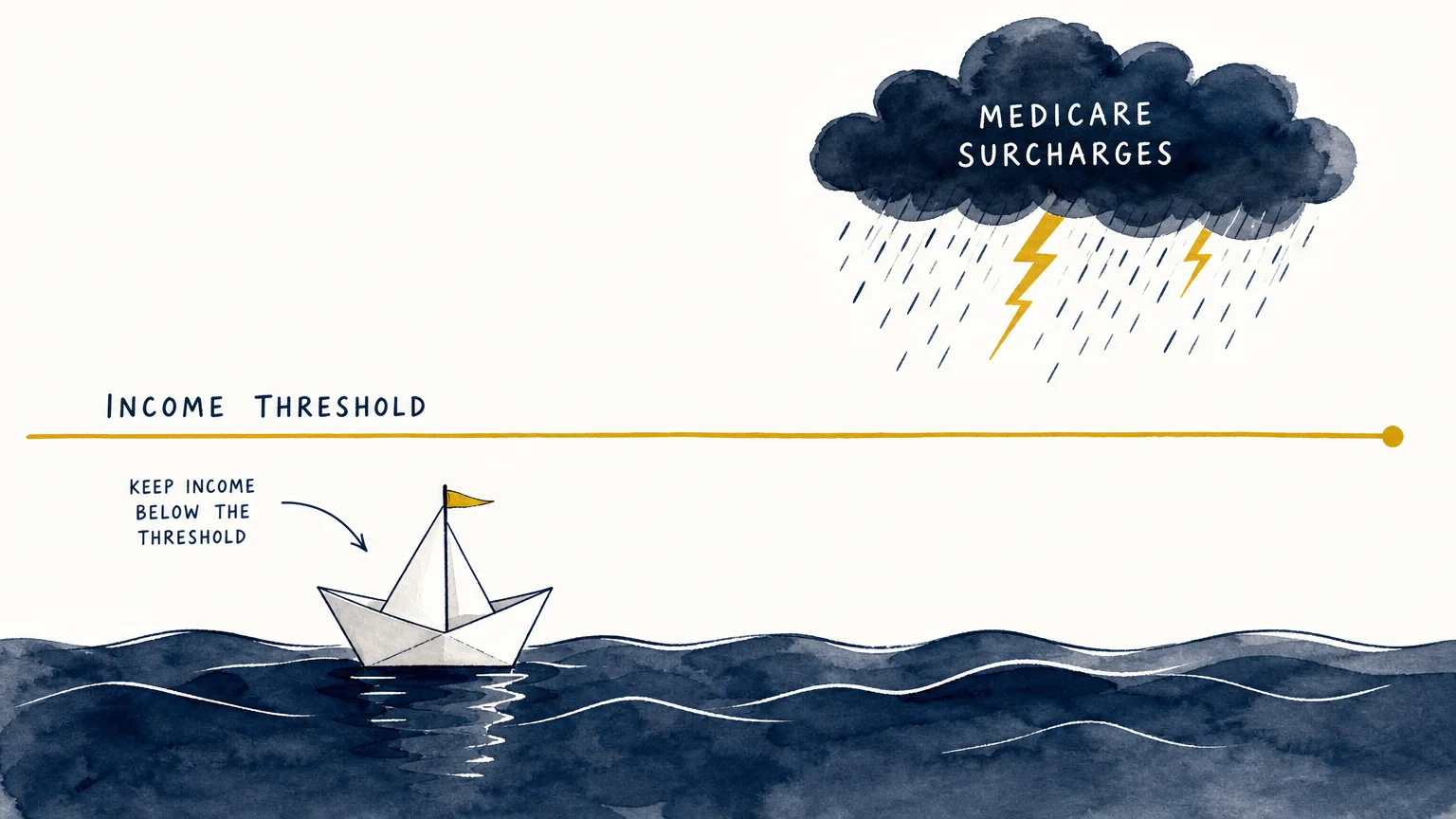

Turning 73 often brings a sudden spike in taxable income due to mandatory IRA withdrawals. This income surge requires you to carefully monitor your Medicare premiums. The Social Security Administration bases your Medicare Part B and Part D costs on your Modified Adjusted Gross Income (MAGI). If your income exceeds specific thresholds, you will be subject to the Income-Related Monthly Adjustment Amount—commonly known as IRMAA.

IRMAA functions as a premium surcharge, and it operates on a strict “cliff” system rather than a gradual phase-in. If your MAGI goes even one single dollar over the limit, your Medicare premiums jump to the next pricing tier for the entire calendar year. For individuals filing a joint tax return in 2024, the first surcharge bracket begins when income exceeds $206,000. Navigating these limits requires precise planning because Medicare utilizes a two-year lookback period; the income you report on your tax return at age 73 will dictate the Medicare premiums you pay at age 75.

To mitigate this hidden tax, you must project your income well before December 31. If you see that your RMD will push you just over an IRMAA cliff, you can deploy targeted strategies to lower your MAGI. As mentioned earlier, shifting a portion of your mandatory distribution to a charity via a QCD is a highly effective way to suppress your taxable income. Alternatively, if you recognize the danger early in the year, you might defer taxable capital gains in your brokerage accounts or harvest investment losses to offset your gains. Keeping a close eye on these thresholds ensures you keep more of your money rather than sending it to the Centers for Medicare and Medicaid Services.

Tip #4: Reassess Your Asset Location and Withdrawal Sequence

Once your tax-deferred accounts mandate withdrawals, your overall withdrawal sequence needs a thorough reassessment. During your earlier retirement years, you maintained total control over which accounts you pulled money from to fund your lifestyle. At age 73, the IRS forces your hand by guaranteeing a baseline of taxable income through your RMDs. You must construct a new portfolio distribution strategy that harmonizes with this forced income.

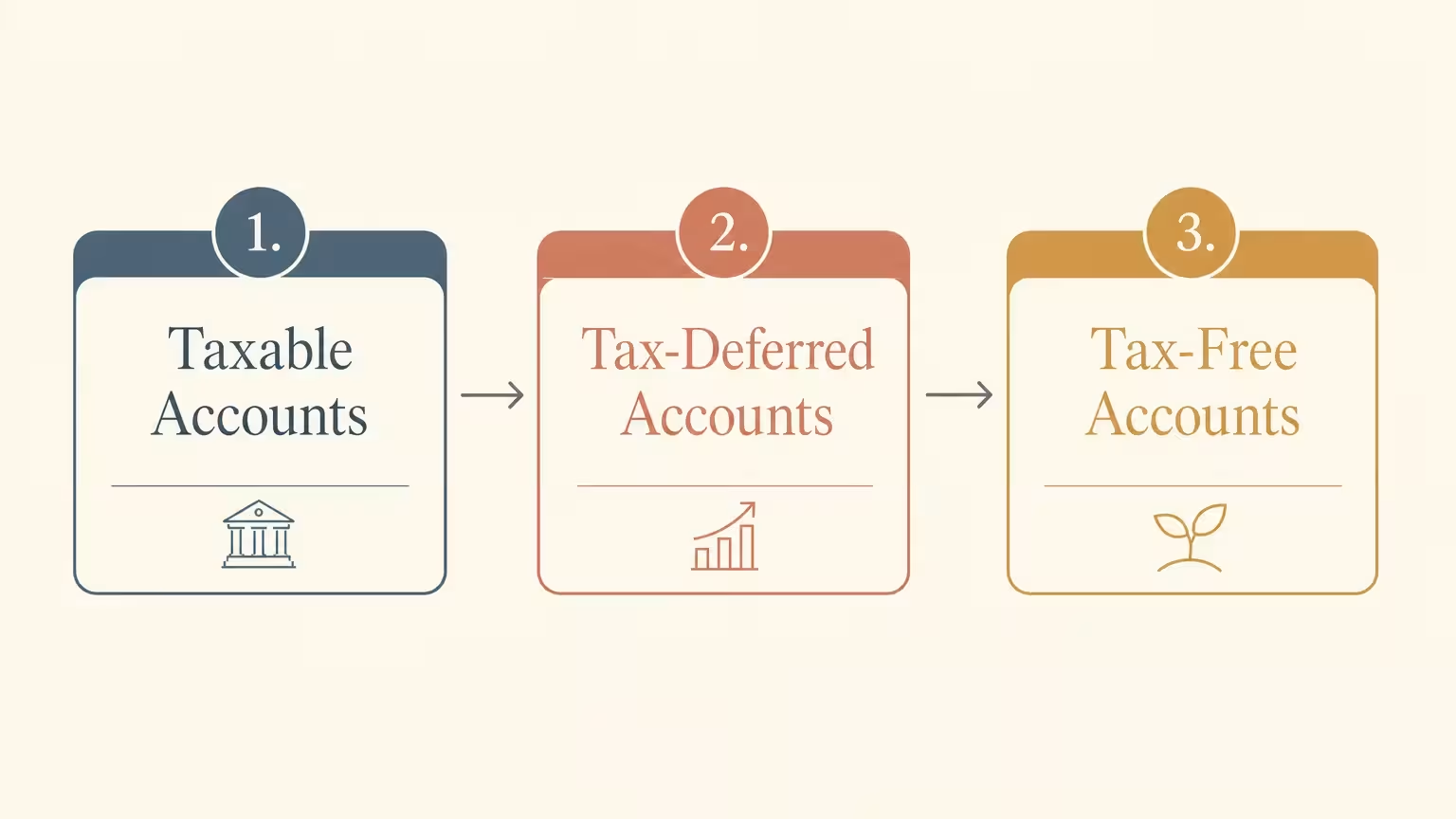

Effective asset location management involves balancing withdrawals across three distinct buckets: taxable brokerage accounts, tax-deferred accounts like traditional IRAs, and tax-free accounts like Roth IRAs. Your mandatory distribution provides your foundational income for the year. If that distribution covers all your living expenses, you simply reinvest any excess cash into a taxable brokerage account. However, if you need additional funds to support your lifestyle, you must choose the next source carefully to minimize your tax burden.

Many savvy retirees utilize a “fill up the bracket” strategy. You calculate exactly how much room remains in your current federal income tax bracket after accounting for your RMD. You can draw from your taxable brokerage accounts—where long-term capital gains enjoy preferential, lower tax rates—to meet your spending needs up to the edge of the next bracket. If you require even more capital for a large purchase like a vehicle or a vacation, you pull those final dollars from your Roth IRA. Because Roth IRA withdrawals are entirely tax-free and do not impact your AGI, you prevent yourself from accidentally leaping into a higher tax bracket or triggering an IRMAA surcharge.

Tip #5: Update Your Tax Withholdings and Estimated Tax Payments

Receiving new streams of mandatory income introduces a new layer of responsibility regarding tax payments. The IRS treats traditional IRA distributions as ordinary income, taxing them at your standard federal and state marginal rates. Unlike a traditional paycheck from an employer, your retirement account custodian does not automatically withhold a perfectly calculated percentage for taxes. You must proactively manage your tax withholdings to avoid a frustrating surprise and potential underpayment penalties when tax season arrives.

When you set up your RMD, your brokerage firm will provide a distribution form that includes a tax withholding election section. The default federal withholding rate is often a flat 10 percent; however, this rarely aligns with a retiree’s actual tax liability. If your total income places you in the 22 percent or 24 percent tax bracket, relying on the default withholding will leave you severely underpaid by the end of the year. You hold the power to select a customized withholding percentage that accurately reflects your effective tax rate.

Alternatively, you can choose to have zero taxes withheld from the distribution and instead make quarterly estimated tax payments directly to the IRS and your state revenue department. This strategy allows your entire RMD to remain invested and generating interest for a few extra months. Whichever method you choose, ensure you satisfy the IRS “safe harbor” rules to dodge underpayment penalties. You generally accomplish this by paying at least 90 percent of your current year’s tax liability or 100 percent of your previous year’s tax liability. Evaluating your tax payments the year you turn 73 establishes a smooth, stress-free routine for the rest of your retirement.

The Takeaway: Living a More Blissful Retirement

Reaching age 73 represents a gateway into a more structured phase of your retirement journey. While mandatory distributions and shifting tax rules might seem complex at first glance, they are entirely manageable when approached with a proactive mindset. Implementing these five tax moves allows you to maintain control over your wealth, minimize your lifetime tax burden, and protect the nest egg you worked so diligently to build.

By calculating your distributions accurately, optimizing your charitable giving, monitoring your Medicare thresholds, balancing your withdrawal sources, and keeping your tax payments current, you build a resilient financial foundation. You possess the tools and the knowledge necessary to navigate this transition smoothly. Take the time to collaborate with your financial advisor or tax professional to customize these strategies for your unique situation. When your financial house is in order, you can focus your energy on the true purpose of your golden years: enjoying your family, pursuing your passions, and living a truly blissful retirement.

Frequently Asked Questions

Can I delay my first RMD to avoid paying taxes this year?

Yes, the IRS provides a one-time grace period for your very first Required Minimum Distribution. You have the option to delay this initial withdrawal until April 1 of the year following the year you turn 73. However, utilizing this delay means you must take two distributions in that subsequent year—your delayed first RMD by April 1, and your second RMD by December 31. Taking two mandatory withdrawals in a single calendar year often pushes your taxable income into a higher tax bracket and can trigger Medicare premium surcharges. Many retirees find it more tax-efficient to take their first distribution during the year they actually turn 73.

Do I have to take an RMD if I am still working at age 73?

The rules depend on where your retirement funds are held. If you are still employed at age 73 and do not own 5 percent or more of the company you work for, you can generally delay taking RMDs from that specific employer’s 401(k) or 403(b) plan until you actually retire. However, this “still working” exception does not apply to traditional IRAs, SEP IRAs, or SIMPLE IRAs. You must begin taking mandatory distributions from your individual retirement accounts at age 73, regardless of your employment status.

What happens if I make a mistake and miss my RMD deadline?

Failing to take your full mandatory distribution by the deadline results in an IRS excise tax. Previously, this penalty was a steep 50 percent of the amount you failed to withdraw. The SECURE 2.0 Act reduced this penalty to 25 percent. Furthermore, if you realize your mistake, take the missing distribution, and file the necessary tax forms within a timely correction window, the IRS will reduce the penalty further to 10 percent. If you miss a deadline due to a reasonable error, you can file IRS Form 5329 to request a penalty waiver, outlining the steps you took to correct the shortfall.

Does my Roth IRA require minimum distributions at age 73?

No, Roth IRAs provide significant flexibility during retirement. As the original owner of a Roth IRA, you are never required to take minimum distributions during your lifetime; your funds can continue growing tax-free indefinitely. Additionally, starting in 2024, the SECURE 2.0 Act eliminated RMDs for employer-sponsored Roth accounts, such as Roth 401(k)s. This makes Roth accounts an incredibly powerful tool for legacy planning and managing your taxable income during your golden years.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply