Recent inflation reports show consumer prices climbing much faster than anticipated in 2026, meaning your upcoming Cost-of-Living Adjustment (COLA) could be significantly higher than expected. While this year brought a modest 2.8% boost, new economic data suggests you might see an increase approaching 4% or more in the new year. Understanding these shifting benefit projections empowers you to make smarter financial decisions right now. By tracking these broader economic trends, you can strategically adjust your household budget before prices rise any further. Let us explore exactly what this new data reveals about your retirement outlook and how you can position yourself to maximize your financial peace of mind.

Tip #1: Understand the Latest Inflation Report Trends

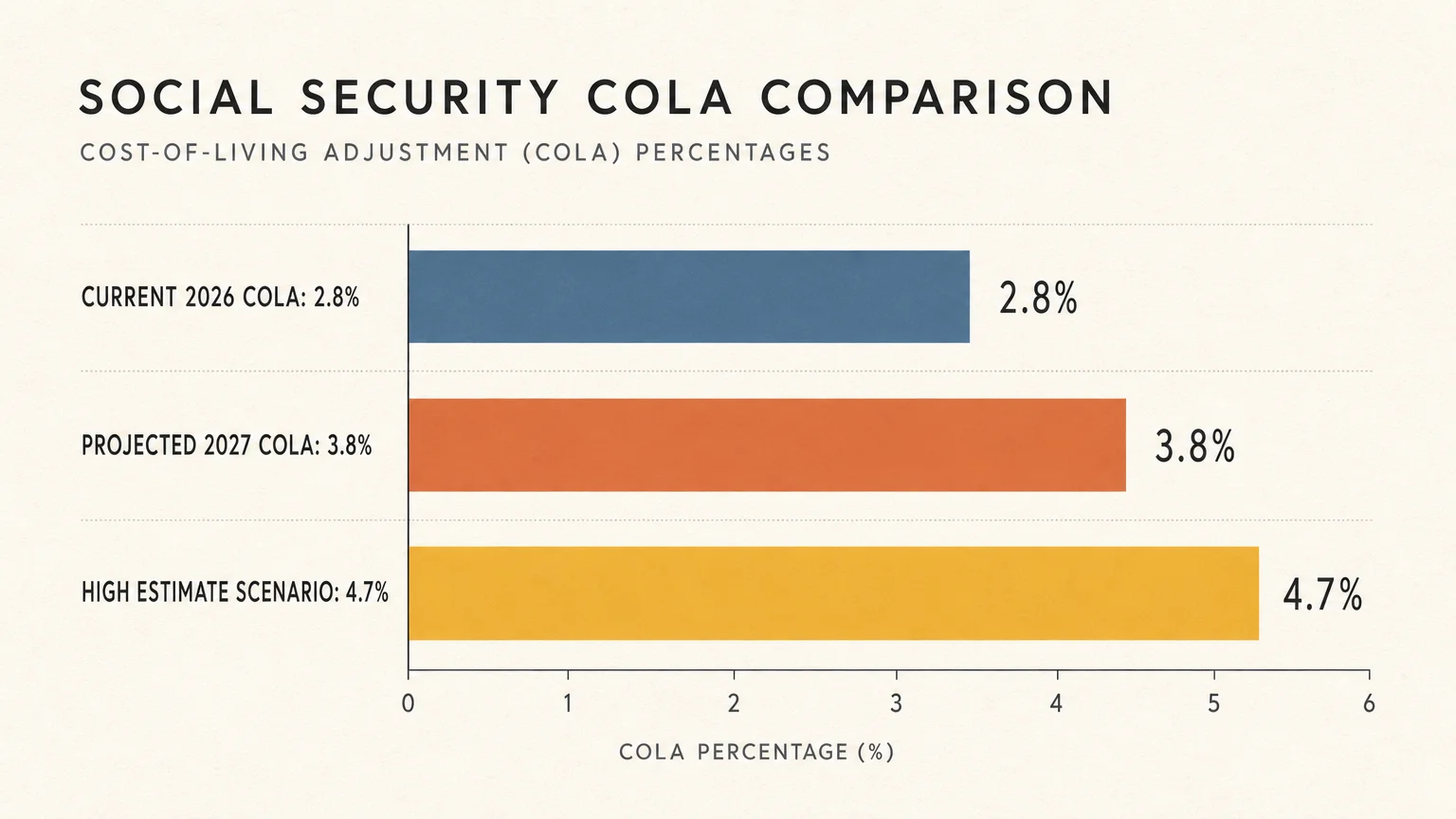

You started 2026 with a modest 2.8% increase to your monthly benefits. At the time, inflation seemed relatively stable, giving retirees hope that everyday prices would remain manageable. However, the economic landscape shifted rapidly by the spring. Recent consumer price indexes indicate that inflation surged past 4% in May, significantly outpacing the raise you received in January. This sudden jump changes the entire conversation around your next cost-of-living adjustment, requiring you to update your financial expectations.

Because the Social Security Administration adjusts benefits to match inflation, a hotter economy directly influences your future income. Advocacy groups like The Senior Citizens League now project a COLA of roughly 3.8% for 2027. Some independent Medicare and Social Security analysts estimate the increase could climb even higher, potentially reaching 4.7% if prices for essentials like fuel, housing, and groceries continue to rise throughout the year.

To put this into perspective, consider a retiree receiving a monthly benefit of $2,000. A 3.8% increase adds $76 to your monthly check, while a 4.7% increase adds $94. Over the course of a year, that translates to more than $1,100 in additional income to help you cover necessary expenses. Understanding this COLA data allows you to forecast your future income with greater accuracy. You no longer have to guess how much relief is on the horizon; you can look at the current inflation report and recognize that a more substantial adjustment is likely coming your way. Armed with this concrete knowledge, you can approach your daily spending with confidence, knowing financial reinforcements are building for the upcoming year.

Tip #2: Look at the Q3 Timeline for Official Benefit Projections

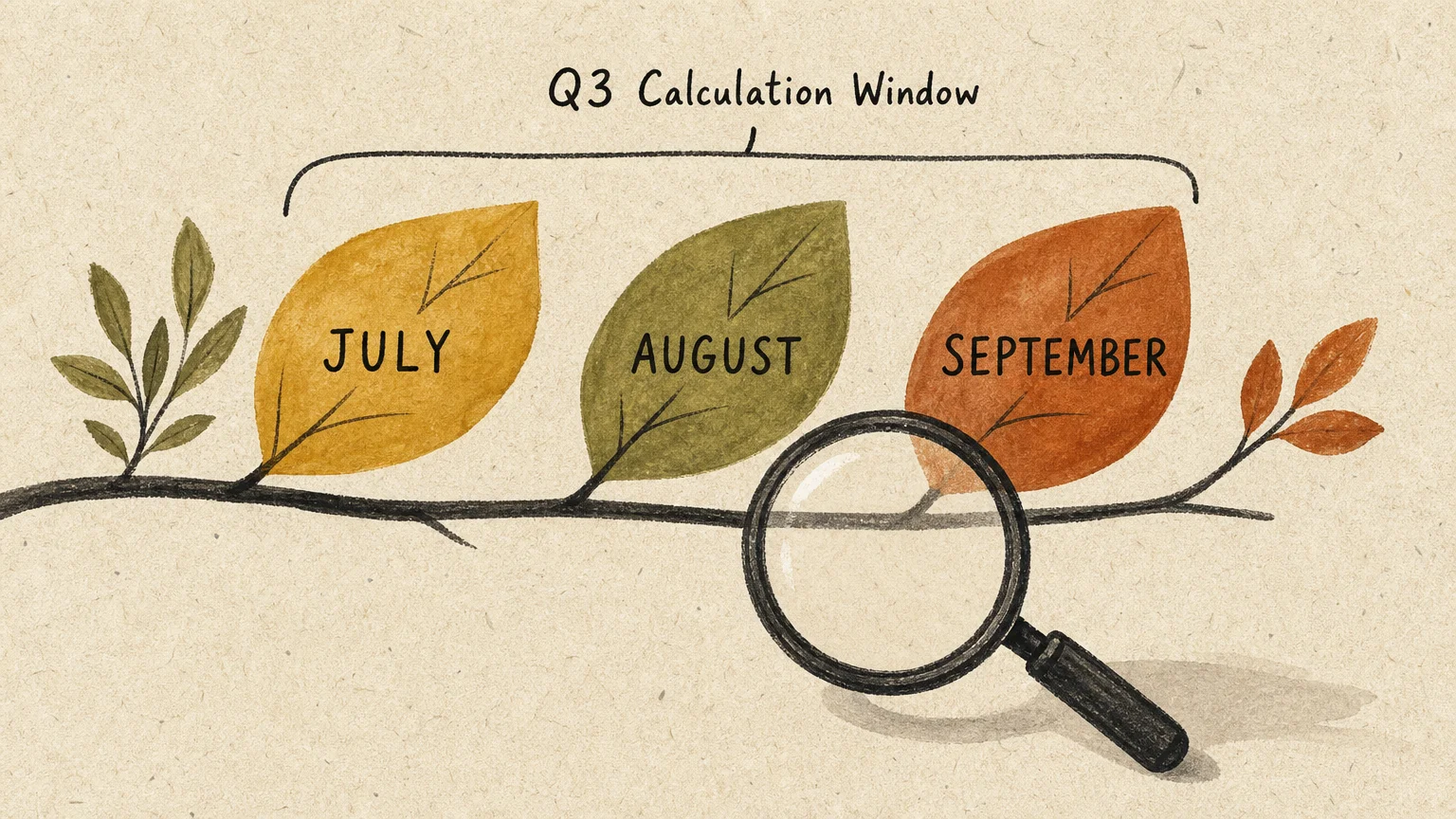

While reading about rising benefit projections in the spring provides a helpful preview, you must understand the specific timeline the government uses to calculate your actual raise. The Social Security Administration does not base your yearly adjustment on inflation from April, May, or June. Instead, they rely exclusively on economic data from the third quarter of the year to formulate their final calculations.

Specifically, the government tracks the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) during July, August, and September. They average the inflation data from these three specific months and compare it to the same three-month period from the previous year. The percentage difference mathematically becomes your official COLA for the new year. If there is no increase, your benefits simply remain exactly the same.

Knowing this timeline helps you manage your expectations and severely reduces daily financial anxiety. You do not need to stress over every single monthly inflation report broadcasted on the evening news. Spring inflation spikes often grab sensational headlines, but late-summer economic trends ultimately dictate your actual wallet.

Use this third-quarter window as your personal observation period. Notice what you pay at the grocery store or the pharmacy during July and August. These are the specific prices shaping your upcoming check. The government officially announces the finalized COLA in mid-October, giving you several months to plan before the new amount appears in your January direct deposit. By focusing only on the data that truly matters, you protect your peace of mind and keep your retirement outlook grounded in facts rather than speculation.

Tip #3: Evaluate Your Personal Inflation Rate

The official inflation report provides a broad overview of the national economy, but it rarely captures the exact financial reality of a senior household. The index used to calculate your annual raise measures the spending habits of urban wage earners and clerical workers. These individuals typically spend a large portion of their income on commuting, education, and apparel—categories that may no longer dominate your monthly spending.

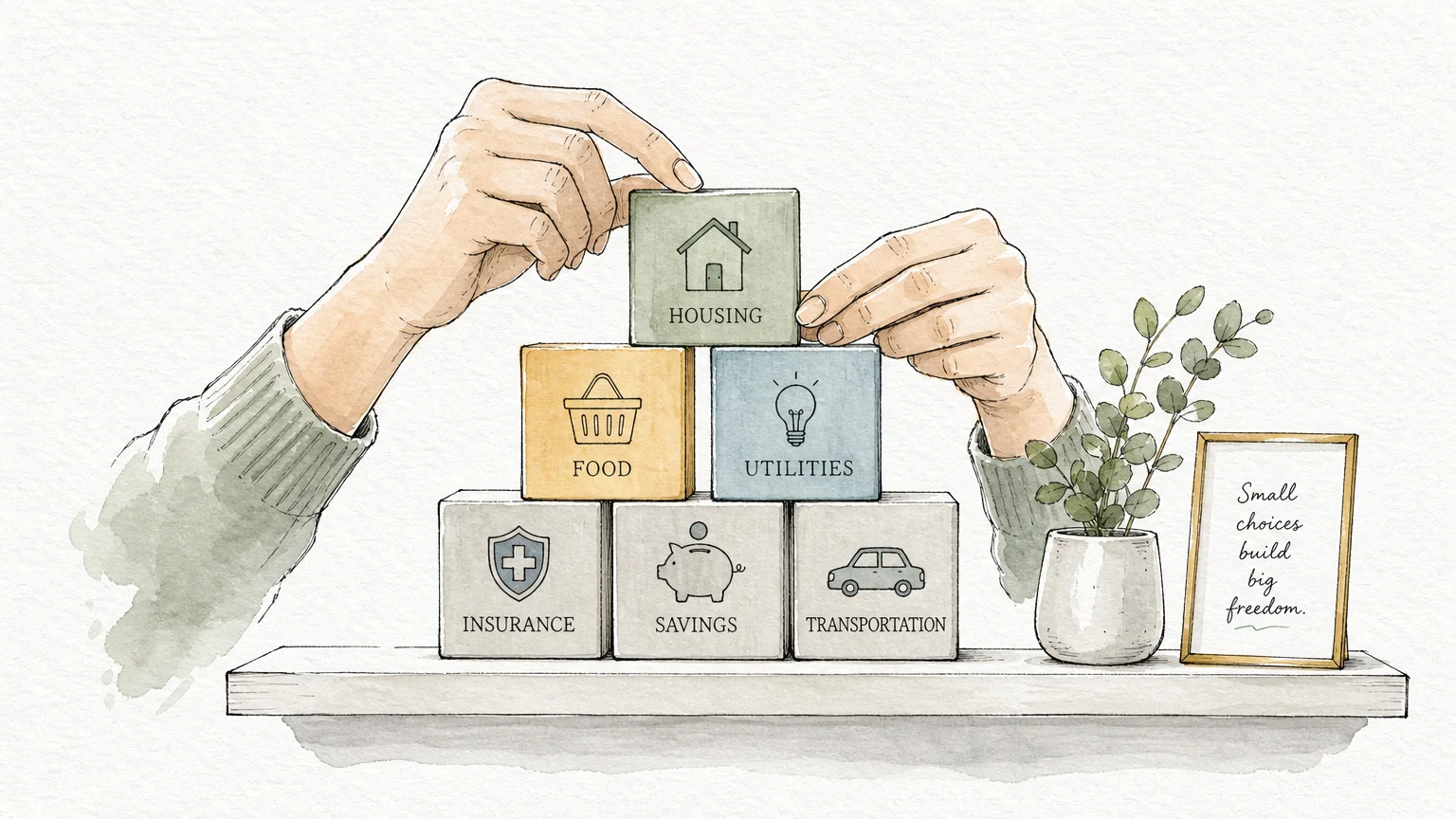

As a retiree, your financial patterns look completely different. You likely dedicate a much larger slice of your monthly budget to healthcare, prescription medications, housing, and utilities. Historically, medical costs and housing expenses rise at a much faster rate than general consumer goods. Because of this discrepancy, an official 3.8% or 4.7% adjustment might not fully cover the actual price hikes you experience at the pharmacy counter or the doctor’s office.

You can take control of this situation by calculating your personal inflation rate. Sit down with your bank statements from the past six months. Identify your top five necessary expenses; these usually include groceries, utilities, rent or property taxes, insurance, and medical out-of-pocket costs. Compare what you paid last month to what you paid six months ago to see the real difference.

If your personal living costs have increased by 6%, you immediately know that an anticipated 4% benefit increase will leave a small gap. Identifying this gap early prevents unpleasant surprises down the road. You can make targeted, intelligent adjustments right now, rather than waiting until January to realize your expenses have outgrown your income. Tracking your own financial data empowers you to build a resilient, deeply personalized retirement plan that honors your exact lifestyle.

Tip #4: Adjust Your Household Budget Proactively

One of the most frustrating aspects of managing a fixed income is the built-in delay between rising prices and your corresponding benefit increase. When an inflation report shows prices spiking in May, you feel the financial pinch immediately at the checkout counter. However, the cost-of-living adjustment designed to offset those higher prices will not reach your bank account until the following January. You must actively navigate this lag to protect your precious savings.

Do not wait for the government to increase your check; take immediate action to streamline your household budget today. Start by auditing your recurring monthly expenses. Many seniors pay for streaming services, magazine subscriptions, or premium cable channels they rarely use. Canceling just two unused digital services can easily put an extra $30 or $40 back into your pocket each month, creating immediate breathing room.

Next, pick up the phone and negotiate your essential bills. Call your auto insurance provider to ask about low-mileage discounts or senior defensive driving credits. Contact your cellular provider and ask to be switched to a senior-specific plan. Many utility companies also offer fixed-rate billing or discount programs specifically designed for older adults living on fixed incomes.

Look beyond your basic utilities and explore local community resources. Many municipalities offer substantial property tax exemptions or freezes for older adults, which can save you thousands of dollars annually. Additionally, review your prescription drug coverage. Switching to generic medications or utilizing preferred pharmacy networks can dramatically reduce your monthly out-of-pocket healthcare expenses. By trimming the fat from your budget now, you effectively give yourself a raise before the official COLA takes effect. This proactive approach ensures that when your larger Social Security check finally arrives, you have more discretionary income to spend on the things you truly enjoy.

Tip #5: Factor Medicare Premium Changes into Your Retirement Outlook

When projecting your future income, you must look beyond the gross increase in your Social Security check. Many retirees celebrate a high COLA announcement in October only to feel profoundly disappointed when their actual January deposit looks smaller than anticipated. This happens because Medicare Part B premiums are automatically deducted from your Social Security benefits before the money ever reaches your bank account.

Historically, years with significant inflation also see rising healthcare costs, which typically prompt the Centers for Medicare and Medicaid Services to increase Part B premiums. If you are expecting an $80 monthly boost from your cost-of-living adjustment, a $15 or $20 increase in your Medicare premium will noticeably reduce your net gain. You must account for this interplay to maintain a highly accurate financial picture.

Fortunately, a special federal rule known as the hold harmless provision protects most beneficiaries. This vital rule ensures that a Medicare premium increase cannot reduce your net Social Security check below what you received the previous year. While your benefit will never shrink from year to year, a steep premium hike can certainly absorb a large portion of your upcoming raise.

To maintain a realistic retirement outlook, always factor potential healthcare costs into your benefit projections. Keep a close eye on Medicare announcements, which usually occur in the fall right around the same time the official COLA data is released. By mentally subtracting a modest amount for premium increases, you ensure your 2027 household budget relies on accurate, realistic figures. Planning for these essential deductions transforms potential disappointment into prepared confidence.

Tip #6: Diversify Income Beyond Social Security

Relying solely on Social Security to fund your golden years leaves you highly vulnerable to unpredictable economic trends. While a higher COLA provides necessary relief, it is designed strictly to help you tread water and maintain your current purchasing power, not to build wealth over time. To enjoy a truly blissful and secure retirement, you should actively diversify your income streams.

Start by evaluating where you keep your emergency savings. Traditional bank accounts often pay less than a fraction of a percent in interest, meaning your cash loses value against inflation every single day. Consider moving a portion of your liquid savings into a high-yield savings account or a Certificate of Deposit (CD). Many of these secure, FDIC-insured accounts offer generous interest rates that match or exceed current inflation levels, allowing your money to grow passively without requiring you to take on risky investments.

If you feel comfortable navigating the financial markets, you might also speak with a financial advisor about dividend-paying stocks. Established companies with a long history of paying dividends often increase their payouts during inflationary periods, providing you with a growing stream of passive income that outpaces standard inflation.

Beyond optimizing your savings and investments, consider exploring light, flexible part-time work that aligns perfectly with your unique passions. The modern gig economy offers countless opportunities for seniors to monetize a lifetime of valuable skills. You could offer consulting services in your former career field, tutor students online, or sell handmade crafts. Even generating an additional $300 a month creates a remarkably powerful financial buffer. When you build alternative income sources, shifting benefit projections no longer dictate your lifestyle. You transform from a passive recipient of government adjustments into an active director of your financial destiny.

The Takeaway: Living a More Blissful Retirement

Navigating shifting economic trends and parsing through complex inflation reports can sometimes feel overwhelming, but it does not have to disrupt your hard-earned peace of mind. By staying thoroughly informed about the latest COLA data, you empower yourself to make smart, forward-thinking decisions. Remember that the upcoming benefit projections are simply tools to help you plan your budget, not reasons to panic about the future.

You have worked incredibly hard over the decades to earn your Social Security benefits, and you deserve to enjoy your golden years with robust confidence and radiant joy. Take the actionable steps outlined above—evaluate your personal spending, trim unnecessary monthly expenses, and boldly explore new ways to grow your savings. By taking a proactive approach to your finances today, you guarantee that your retirement outlook remains positive and entirely secure. Embrace this beautiful season of life knowing that with a bit of thoughtful preparation, you are fully equipped to handle whatever the broader economy brings your way.

Frequently Asked Questions

When exactly will the Social Security Administration announce the 2027 COLA?

The Social Security Administration officially announces the annual cost-of-living adjustment in mid-October. This highly anticipated announcement immediately follows the release of the September inflation report by the Bureau of Labor Statistics. Once the official percentage is declared to the public, you will receive a personalized notice in November or December detailing your exact new benefit amount for the upcoming year.

Does the annual benefit adjustment fully cover the rising cost of groceries and healthcare?

Unfortunately, the official adjustment does not always mirror the exact price increases you experience at the store or the pharmacy. The government calculates the adjustment using a spending index based on urban wage earners, who generally spend far less on healthcare and housing than older adults. Because seniors spend a larger percentage of their income on medical care and groceries—categories that often see the highest inflation—you may still need to proactively adjust your personal budget to make up the difference.

Can my Social Security check decrease if inflation goes down?

No, your gross Social Security benefit will never decrease due to a drop in inflation. If the economy experiences deflation and consumer prices actually fall during the third quarter, the cost-of-living adjustment simply drops to zero percent. The government designed the program to protect your baseline income, ensuring your gross monthly check remains steady even in negative economic conditions.

How do potential Medicare Part B increases affect my upcoming raise?

Because Medicare Part B premiums are deducted directly from your Social Security payments, an increase in your premium will immediately reduce the net amount of your raise. For example, if your benefit goes up by $80 but your Medicare premium simultaneously increases by $15, you will only see a $65 increase in your bank account. However, a federal rule ensures that a Medicare premium hike cannot lower your net payment below what you received the previous year.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply