Taking control of your retirement income means creating a personalized cost-of-living adjustment rather than waiting for annual federal announcements. Rising prices impact your daily expenses, making it vital to find reliable ways to boost your purchasing power. By adopting proactive income growth strategies and smart financial habits, you can protect your lifestyle against inflation. You will learn practical methods for generating extra income, optimizing your investments, and managing your everyday spending without sacrificing the joy of your golden years. These approaches offer concrete ways to strengthen your financial foundation and give you lasting peace of mind.

Tip #1: Maximize Yields on Your Cash Savings

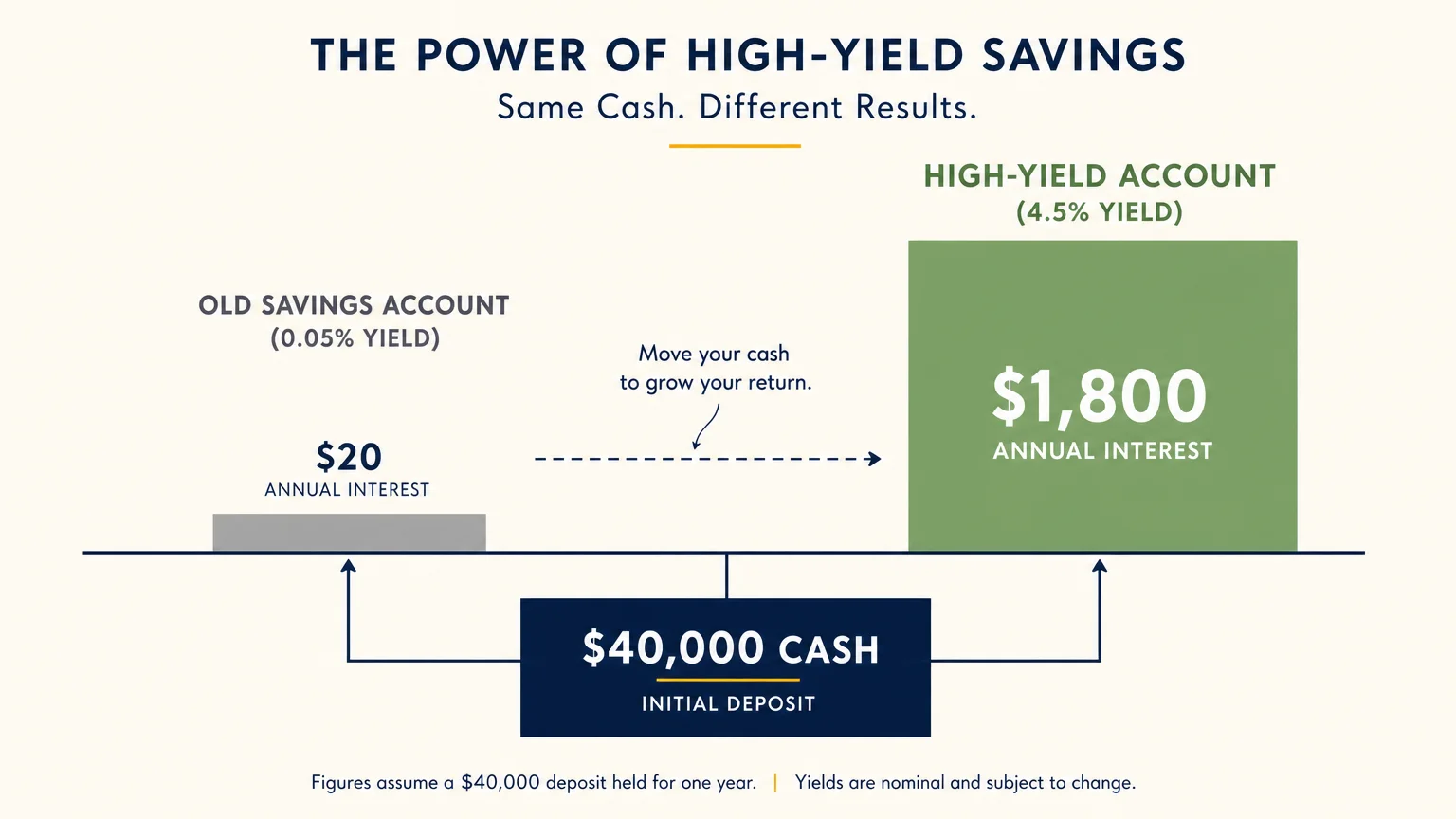

Many retirees keep a significant portion of their emergency funds in traditional bank accounts earning almost zero interest. You can easily change this dynamic by shifting your funds into high-yield savings accounts or certificates of deposit. When inflation drives up the cost of everyday goods, it usually pushes interest rates higher as well. You can take advantage of this economic shift by moving your money to institutions that offer competitive returns. This simple adjustment protects your purchasing power without requiring you to take on any stock market risk; it acts as a reliable foundation for your retirement finances.

To maximize your returns while maintaining access to your money, consider building a CD ladder. This strategy involves dividing your investment into multiple certificates of deposit with different maturity dates—such as three, six, nine, and twelve months. As each certificate matures, you can either spend the cash or reinvest it into a new one-year CD at the highest available rate. This approach provides a steady stream of accessible cash while capturing better yields than a standard savings account. It is a straightforward method for beating inflation with minimal daily effort.

Let us look at the numbers to see the real financial impact. If you move $40,000 from an old savings account paying 0.05 percent to a high-yield account paying 4.5 percent, your annual interest jumps from a meager $20 to $1,800. That additional money easily covers several months of utility bills or groceries. Generating this reliable yield creates a powerful, personalized cost-of-living adjustment that you control entirely.

Tip #2: Turn Your Professional Expertise Into Consulting Income

Leaving your primary career does not mean your professional expertise loses its value. You can turn decades of industry experience into a lucrative consulting or freelance business. Generating extra income in retirement does not require returning to a grueling forty-hour workweek. You hold the power to set your own hours, choose the projects that interest you, and decline the ones that do not. A retired marketing director might consult for small local businesses, while a former accountant could offer seasonal tax preparation services.

The beauty of independent consulting lies in its unparalleled flexibility. You can work heavily during the winter months and take the entire summer off to travel and spend time with family. Reaching out to your former employer or networking with local business owners often yields your first few clients. Because you already possess the necessary skills, your startup costs remain incredibly low. You only need a computer, an internet connection, and a willingness to share your knowledge.

Earning just a modest amount through consulting provides a massive boost to your budget. If you bill $50 an hour and work just five hours a week, you add $1,000 a month to your household budget. This steady stream of extra income acts as an enormous buffer against economic shifts, ensuring you never have to stress over rising property taxes or medical costs. Staying engaged in your field also keeps your mind sharp and provides a deep sense of ongoing purpose.

Tip #3: Build a Reliable Dividend Income Stream

One of the most historically proven income growth strategies involves investing in companies that consistently share their profits with shareholders. Dividend growth investing focuses on purchasing shares in established businesses that have a long track record of raising their payouts year after year. Financial professionals often refer to these elite companies as dividend aristocrats. When you hold these assets, your income stream grows automatically over time, creating a natural and powerful hedge against rising consumer prices.

You do not need to spend hours researching individual stocks to implement this strategy. Many exchange-traded funds bundle dozens of these high-quality dividend-paying companies into a single, easily managed investment. By purchasing shares of a dividend-focused fund, you instantly diversify your holdings across multiple sectors—such as consumer goods, healthcare, and utilities. During your early retirement years, you can automatically reinvest these dividends to compound your wealth. When you need the money, you simply redirect the cash payouts straight into your checking account.

Consider a practical example of how this works. If you hold a $100,000 portfolio yielding 3.5 percent, you generate $3,500 annually in passive cash flow. If those companies increase their dividends by an average of 6 percent each year, your cash payout grows steadily without you ever having to sell a single share of your principal. This reliable, increasing stream of funds represents the ultimate self-made cost-of-living adjustment.

Tip #4: Optimize Your Monthly Outgoings

Creating your own cost-of-living adjustment is not solely about increasing your revenue; it also requires keeping more of the money you already have. Applying smart retirement budgeting tips allows you to dramatically lower your monthly overhead. Start by conducting a thorough audit of your recent bank and credit card statements. Identify automatic subscriptions you no longer use, such as premium streaming services, unused gym memberships, or old software licenses. Canceling these recurring charges instantly frees up cash.

You can also negotiate better rates on your essential bills. Call your internet provider, cell phone carrier, and auto insurance company to ask for their current promotional rates or senior discounts. Companies frequently offer loyalty discounts to retain long-term customers, but they rarely advertise them unless you ask directly. Furthermore, adjusting your thermostat by a few degrees or switching to energy-efficient appliances lowers your monthly utility costs, directly combating the effects of beating inflation.

Reducing your monthly outgoings by $250 is the exact mathematical equivalent of earning an extra $250, yet it requires no ongoing labor or tax obligations. By saving $3,000 a year through careful expense management, you create a massive financial cushion. Staying mindful of your spending habits ensures your money stretches further, cementing a cornerstone of strong retirement finances.

Tip #5: Capitalize on Your Unused Space

If you have downsized your life but still own a home with unused areas, you possess a highly valuable income-producing asset. The modern sharing economy makes it incredibly easy to turn an empty bedroom, a vacant garage, or an underutilized driveway into a steady stream of extra income. Renting out a furnished room to a traveling nurse or a visiting graduate student can comfortably yield hundreds of dollars a month. These short-term arrangements offer great flexibility compared to traditional year-long leases.

If you prefer not to share your immediate living quarters, you still have excellent options. Many people desperately need safe spaces to store their belongings, park their recreational vehicles, or keep their boats during the off-season. Specialized neighborhood apps connect you with locals willing to pay for your unused garage or driveway space. This strategy generates passive revenue with almost zero daily effort required on your part.

Earning an extra $150 to $300 a month simply by letting someone park their camper in your side yard provides a fantastic inflation buffer. This straightforward method requires no special skills or heavy lifting. Always take a moment to review your local zoning laws and homeowner association rules, and ensure you have proper insurance coverage before listing your available space.

Tip #6: Leverage Cash-Back and Loyalty Programs

Every time you purchase groceries, pump gas, or dine at a local restaurant, you hold an opportunity to claw back a percentage of your expenses. Strategic use of cash-back credit cards serves as an incredibly simple tool for enhancing your retirement finances. Many cards offer between two and five percent cash back on specific everyday spending categories. By aligning your purchases with the right payment method, you effectively create a permanent discount on the items you need to survive.

To maximize this benefit, you must commit to paying your statement balance in full every single month. Carrying a balance incurs interest charges that completely wipe out the value of any rewards you earn. If you use your cards responsibly, the cash back represents pure profit. You can amplify these savings by combining your credit card rewards with digital coupons and grocery store loyalty apps, allowing you to double dip on discounts.

The numbers add up surprisingly fast over a calendar year. If your household spends $800 a month on groceries and gas using a card that offers three percent cash back, you pocket nearly $300 in free money annually. While this sum will not fund a luxury vacation on its own, it easily covers a utility bill or pays for a special night out. Small, consistent savings mechanisms perfectly complement your broader income growth strategies.

Tip #7: Navigate the Gig Economy on Your Own Terms

Many retirees discover immense joy in transitioning their lifelong hobbies into modest, low-stress business ventures. The gig economy provides countless avenues to monetize your passions while maintaining complete control over your schedule. If you love spending time in your workshop or sewing room, selling your handmade crafts at local farmer’s markets or through online marketplaces brings in reliable extra income. This creative outlet keeps you active while simultaneously fattening your wallet.

Animal lovers can find incredible success offering pet-sitting or dog-walking services in their immediate neighborhoods. Platforms designed for pet care allow you to set your own rates, choose the size of dogs you prefer to handle, and block off dates when you want to take a personal vacation. Walking dogs provides fantastic cardiovascular exercise, wonderful social interaction, and a steady paycheck.

Creating your own personal COLA becomes a highly enjoyable process when the work involves activities you already love doing. Earning $300 a month walking a neighbor’s golden retriever a few days a week removes the financial pressure of rising grocery prices. The secret to gig economy success in retirement is to start small, keep your overhead expenses low, and only scale up the business if it continues to feel fun and manageable.

The Takeaway: Living a More Blissful Retirement

You do not need to sit back and watch inflation slowly erode your hard-earned savings. By taking proactive steps to maximize your cash yields, optimize your expenses, and generate alternative revenue streams, you effectively build your own cost-of-living adjustment. Embracing these actionable strategies shifts you from a passive recipient of economic changes to an empowered creator of your own financial stability.

Moving forward with confidence requires a willingness to adapt and a commitment to managing your retirement finances actively. Whether you choose to invest in dividend-paying companies, rent out your spare garage, or consult in your former industry, every small step makes a profound difference. Implementing just a few of these methods protects your purchasing power, reduces financial anxiety, and allows you to fully enjoy the peace and freedom of your golden years.

Frequently Asked Questions

What exactly does COLA mean in the context of my personal finances?

COLA stands for Cost of Living Adjustment. Traditionally, this term refers to the annual percentage increase applied to Social Security benefits to help offset inflation. In the context of your personal finances, creating your own COLA means proactively generating extra money or reducing expenses to ensure your purchasing power keeps pace with rising prices.

Will earning extra money affect my Social Security benefits?

If you have already reached your full retirement age, you can earn an unlimited amount of extra income without any reduction in your Social Security benefits. However, if you claim benefits before reaching your full retirement age, earning above a certain annual limit may temporarily reduce your monthly payout. Always review the current Social Security Administration guidelines regarding the retirement earnings test.

Do these income growth strategies require taking on high financial risks?

Not at all. Many of the most effective strategies involve zero market risk. Opening a high-yield savings account, building a CD ladder, auditing your monthly budget, and selling your consulting services carry virtually no financial risk. Investing in dividend-paying stocks does involve market fluctuations, but focusing on established, high-quality companies significantly mitigates potential downsides.

How can I easily start implementing these retirement budgeting tips today?

The easiest way to begin is by printing out your bank and credit card statements from the last three months. Grab a highlighter and mark every recurring subscription or discretionary expense. Identify two or three services you can cancel immediately. Then, call your primary insurance or internet provider to negotiate a better rate. These small actions take less than an hour and provide immediate financial relief.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply