The annual Cost-of-Living Adjustment (COLA) is your financial shield against rising prices, ensuring your Social Security benefits maintain their purchasing power year after year. With everyday expenses fluctuating, you are likely eager to know exactly how much extra you can expect in your monthly check. While the official number is not announced until October, recent data offers a clear glimpse into what your next benefit increase might look like. By understanding the key factors driving these forecasts, you can take proactive steps to protect your retirement income. We have broken down the most crucial insights you need to confidently navigate the upcoming changes, prepare your household budget, and keep your golden years financially secure.

Tip #1: Understand How the Government Calculates Your Raise

The cost of living adjustment was enacted to prevent inflation from eroding the value of your hard-earned benefits. Prior to this automatic system, Congress had to pass special legislation to authorize any benefit increase. Today, the adjustment happens automatically based on concrete economic data. This systematic approach gives you a highly predictable timeline for your retirement income planning; allowing you to focus on enjoying your golden years.

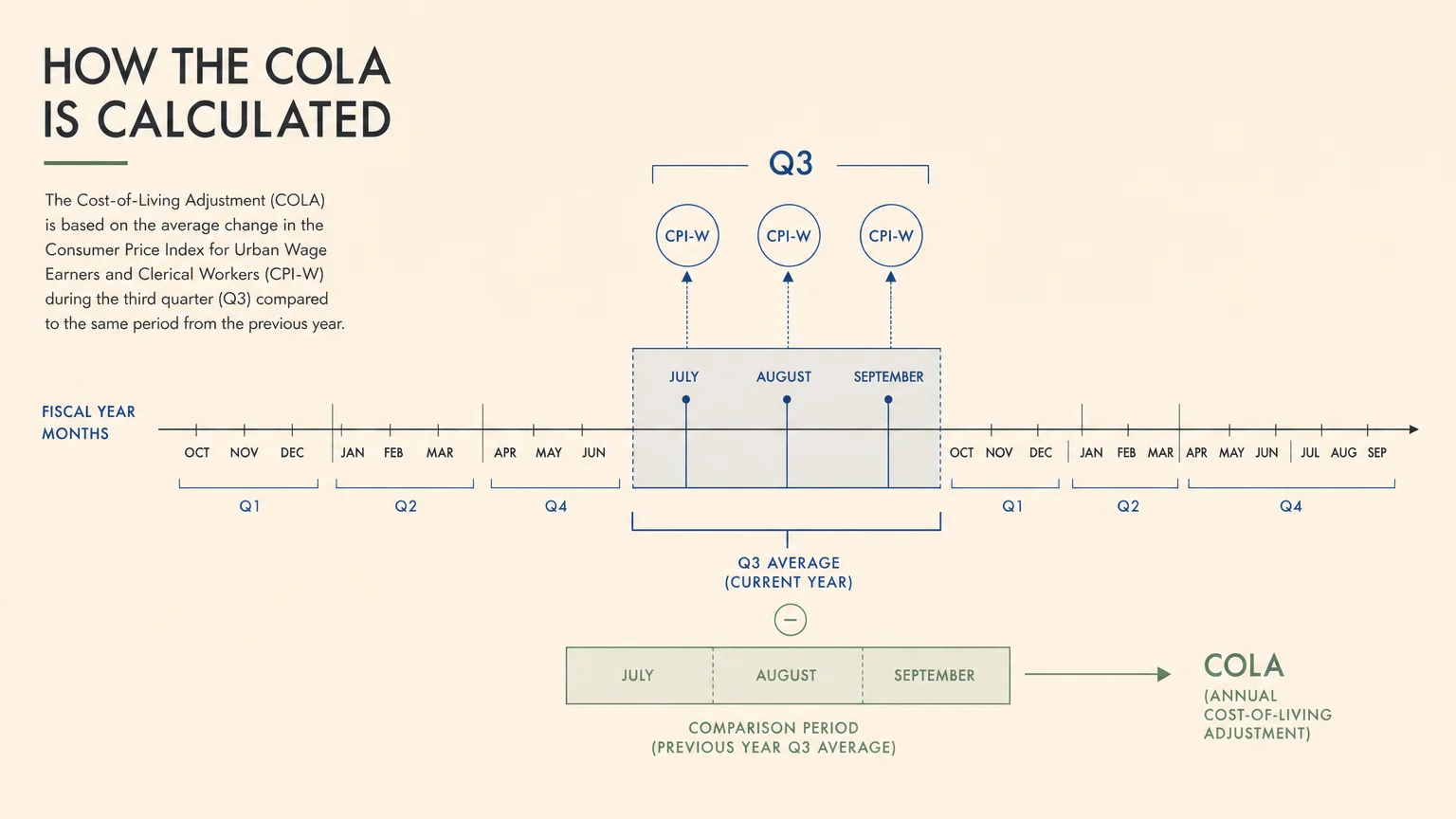

The Social Security Administration relies on a specific metric called the Consumer Price Index for Urban Wage Earners and Clerical Workers—commonly known as the CPI-W. The government tracks this index meticulously to measure how the cost of basic goods and services changes over time. Your future COLA depends heavily on the shifting prices of everyday essentials like groceries, gasoline, apparel, and transportation.

The government tracks several different inflation metrics. You might often hear news anchors discuss the Consumer Price Index for All Urban Consumers; known as the CPI-U. However, the Social Security Administration relies strictly on the CPI-W. Understanding this distinction is crucial because the two indexes weigh spending categories differently. The CPI-W places a heavier emphasis on transportation and food costs compared to the broader CPI-U. Knowing exactly which ruler the government uses helps clarify why official adjustments sometimes differ from headline news reports.

The official calculation is not based on an entire year of inflation. Instead, the Social Security Administration specifically looks at the economic data from the third quarter of the current year. They compare the average CPI-W from July, August, and September to the average from the exact same period in the previous year. If there is a measurable increase in those specific months, that percentage becomes your official raise for the following calendar year.

Tip #2: Keep an Eye on the Latest Cost-of-Living Forecasts

While you will not know the official number until autumn, economic analysts track inflation continuously to provide early estimates. For context, retirees received a 2.8 percent adjustment in 2026. However, persistent inflation driven by recent energy and grocery costs has shifted the outlook for the upcoming 2027 adjustment. Keeping an eye on these projections helps you gauge what to expect and manage your retiree expectations.

Recent inflation adjustment forecasts suggest a more substantial increase is on the horizon. By mid-2026, the nonpartisan advocacy group The Senior Citizens League projected a potential benefit increase of around 3.8 percent. Meanwhile, independent Social Security analysts have forecasted an even higher jump; with some estimates reaching up to 4.7 percent due to unexpected spikes in the consumer price index. These forecasts give you a realistic baseline for your proactive retirement planning.

Before the 2026 adjustment, retirees experienced several volatile years of shifting payouts. We saw massive, historically high bumps followed by more moderate corrections. This rollercoaster environment makes predicting exact figures challenging but incredibly important for anyone living on a fixed income. As you plan your financial future, remember that these forecasts are educated estimates based on current trends. Global events and shifts in energy production can all impact the final calculation announced in the fall.

How does this translate to your actual monthly check? If you currently receive an average monthly benefit of two thousand dollars, a 3.8 percent increase would add about seventy-six dollars to your payment each month. A 4.7 percent jump would add nearly ninety-four dollars. While these numbers remain subject to change based on late-summer inflation data, they provide a highly valuable framework for balancing your household budget.

Tip #3: Factor in Medicare Part B Premium Deductions

One of the most common surprises for seniors involves the complex relationship between their Social Security checks and their Medicare costs. Most retirees choose to have their Medicare Part B premiums deducted automatically from their monthly benefits. When your gross benefit goes up due to a cost of living adjustment, your net payment might not increase by the exact same percentage if Medicare premiums also rise at the same time.

The Centers for Medicare and Medicaid Services typically announce their premium changes around the same time the new COLA is finalized. Historically, healthcare costs have increased at a much faster pace than general inflation. This means a portion of your new raise will likely go directly toward covering higher Medicare Part B expenses. You must factor this deduction into your personal financial planning to avoid overestimating your future monthly cash flow.

Fortunately, a federal rule known as the hold harmless provision offers a reliable safety net for many beneficiaries. This rule ensures that your standard Medicare Part B premium increase cannot exceed the dollar amount of your Social Security raise. In other words, your net monthly check will never decrease from one year to the next. However, this protection does not prevent a scenario where your entire raise is absorbed by rising healthcare costs.

For higher-income retirees, the impact of Medicare premiums can be even more pronounced due to the Income-Related Monthly Adjustment Amount. If your modified adjusted gross income from two years prior exceeded a certain threshold, you will pay a surcharge on top of the standard premium. A significant future COLA can sometimes push you over an income threshold; resulting in an unexpected spike in your medical costs. Staying informed about these brackets allows you to make strategic tax moves.

Tip #4: Calculate Your Personal Rate of Inflation

The official government formula provides a standardized raise for millions of Americans, but it rarely matches your individual spending habits perfectly. The CPI-W measures the out-of-pocket expenses of younger, working-age individuals. Working adults naturally spend significantly more on commuting, professional clothing, and dining out. Conversely, retirees tend to allocate a much larger portion of their fixed income to healthcare, housing, and prescription medications.

Because medical care and housing costs often outpace the general inflation rate, your personal cost of living may be rising much faster than the official metric suggests. This specific discrepancy explains why many seniors feel like their annual adjustments fall short of their actual day-to-day needs. To bridge this gap, you need to understand exactly where your money goes each month. Tracking your specific expenses allows you to create a highly personalized financial benchmark.

Senior advocacy groups have long lobbied Congress to change the official calculation method to the Consumer Price Index for the Elderly—commonly referred to as the CPI-E. This proposed index specifically tracks the spending patterns of Americans aged sixty-two and older. If adopted, it would give greater weight to the soaring costs of medical care, potentially resulting in more generous annual raises. Until such legislative changes occur, calculating your own personalized inflation rate remains your best defense.

Take a quiet afternoon to review your bank statements and credit card bills from the past six months. Compare your current grocery bills, utility costs, and pharmacy out-of-pocket expenses to what you paid last year. Calculating this personal inflation rate empowers you to make highly informed decisions about your budget. When you know precisely how much more you are spending, you can rely less on generic forecasts and more on your own absolute financial reality.

Tip #5: Make Strategic Adjustments to Your Retirement Budget

Armed with a solid understanding of your personal inflation rate, you can take active steps to stretch your retirement income further. Do not simply wait for the government to announce your next raise. Take absolute control of your finances today by conducting a thorough audit of your monthly household budget. Small, intentional changes can add up to incredibly significant savings over the course of a single year.

Start by identifying recurring expenses that you no longer need or actively use. Cancel unused streaming subscriptions, gym memberships, or expensive magazine deliveries. Next, take time to call your daily service providers. You can frequently negotiate lower rates for your internet, cable, and cellular phone plans simply by asking a representative for current retention offers. Reallocating these saved dollars toward essential expenses helps you effortlessly offset the rising cost of groceries.

Food and energy costs consistently rank as the two most volatile expenses in any retiree budget. To combat rising utility bills, consider requesting a free energy audit from your local power provider. Simple fixes like weatherstripping doors, upgrading to LED lighting, and installing a programmable thermostat can drastically reduce your monthly heating and cooling costs. At the grocery store, focus on purchasing seasonal produce and buying non-perishable staples in bulk to lock in lower prices.

You should also warmly embrace the power of targeted senior discounts. Many local grocery stores, retail chains, and restaurants offer dedicated discount days specifically for older adults. Signing up for free loyalty programs can yield substantial savings on your weekly shopping trips. By actively managing your outflows, you effectively give yourself a raise before the new adjustment even takes effect. Every dollar you save strengthens your robust financial foundation for the beautiful years ahead.

Tip #6: Protect Your Buying Power with Smart Savings Strategies

Relying solely on your Social Security benefit leaves you vulnerable to unpredictable economic shifts. To maintain a truly blissful retirement, you must ensure that your personal savings are working just as hard as you did during your career. Inflation quietly erodes the purchasing power of cash sitting in traditional, low-interest bank accounts. You need to position your emergency funds and liquid assets where they can generate a meaningful, steady return.

Explore high-yield savings accounts provided by reputable online banks. These modern accounts often offer interest rates significantly higher than traditional brick-and-mortar institutions; providing a highly reliable way to outpace modest inflation. Alternatively, consider building a Certificate of Deposit ladder. By purchasing multiple certificates with staggered maturity dates, you lock in guaranteed interest rates while maintaining periodic, penalty-free access to your cash when you need it most.

Another excellent vehicle for robust inflation protection is the Series I Savings Bond. Backed by the federal government, these unique bonds offer a guaranteed fixed interest rate combined with a variable inflation rate that adjusts twice a year. Because their yield is directly tied to the consumer price index, these bonds provide a virtually risk-free way to ensure your savings keep pace with the rising cost of living. They serve as a powerful addition to a well-rounded retirement portfolio.

Always consult with a trusted financial advisor before moving your money, but do not let economic fear keep your savings stagnant. Earning a competitive yield on your cash reserves provides an essential, comforting buffer against rising daily expenses. When your personal savings grow alongside your Social Security benefits, you build a resilient financial portfolio. This strategy allows you to easily weather whatever the broader economy brings while maintaining your wonderful standard of living.

Tip #7: Manage the Tax Implications of a Higher Benefit

Receiving a larger monthly check sounds absolutely fantastic, but it can introduce unexpected complexities during tax season. The Internal Revenue Service taxes Social Security benefits based on your combined income. This specific figure includes your adjusted gross income, nontaxable interest, and half of your annual Social Security benefits. When a generous future COLA pushes your total income higher, you might suddenly cross the threshold into an entirely new tax bracket.

Currently, single filers with a combined income over twenty-five thousand dollars and joint filers over thirty-two thousand dollars may have to pay income taxes on a portion of their benefits. A substantial cost of living adjustment could make up to eighty-five percent of your Social Security income taxable. Without proper upfront planning, the delightful raise you celebrate in January could lead to a frustrating, unexpected tax bill the following April.

Beyond federal taxes, you must also consider exactly how your home state handles Social Security benefits. While a majority of states do not tax these benefits at all, a handful still impose their own levies based on specific income thresholds. A higher cost of living adjustment could unexpectedly trigger state-level taxation depending on where you reside. If you are contemplating a move in retirement, researching the tax friendliness of potential destination states is a brilliant, money-saving strategy.

Take proactive measures today to mitigate these potential tax burdens. Work alongside a qualified tax professional or financial planner to continually optimize your retirement withdrawal strategy. They might suggest adjusting the distributions from your traditional retirement accounts to keep your combined income safely below the taxable thresholds. Staying ahead of the tax curve ensures that you get to keep the maximum possible amount of your hard-earned benefits.

The Takeaway: Living a More Blissful Retirement

Navigating the complexities of Social Security adjustments does not have to be a source of stress. While you cannot personally dictate the trajectory of national inflation or force the government to grant a larger future COLA, you possess absolute control over how you prepare for it. By staying informed about inflation adjustment forecasts and proactively managing your household budget, you build a fortress of financial security around your golden years.

Your retirement is meant to be a time of joy, exploration, and peace of mind. Implementing the actionable strategies outlined above empowers you to face the future with unwavering confidence. Whether you are adjusting your tax strategy, maximizing the yield on your savings, or simply auditing your monthly expenses, every positive step you take today secures a brighter tomorrow. Embrace the journey ahead, knowing that you have the knowledge and tools required to thrive in any economic environment.

Frequently Asked Questions

When will the exact COLA amount be officially announced?

The Social Security Administration typically announces the official cost of living adjustment in mid-October of each year. This timeline allows the government to collect and process the necessary consumer price index data from July, August, and September. Once the official percentage is released, you will receive a personalized notice detailing your exact new benefit amount before the end of the year.

Can my Social Security benefits ever decrease if inflation drops?

No, your core Social Security benefits will never go down due to a drop in inflation. The automatic adjustment formula is designed exclusively to increase benefits when the cost of living rises. If the inflation data shows zero growth or a decline in consumer prices—a scenario known as deflation—your benefit amount will simply remain exactly the same for the following year.

Why does my benefit increase often feel insufficient?

Many seniors feel their annual raise falls short because the government uses an inflation metric based on the spending habits of younger, working-age individuals. Working adults spend differently than retirees. Because older adults typically allocate a much larger percentage of their fixed income to healthcare and housing—sectors where costs tend to rise rapidly—the official adjustment frequently lags behind the true cost of living experienced by seniors.

Do I need to apply or fill out forms to receive my COLA?

No action is required on your part to receive the annual increase. The Social Security Administration automatically calculates and applies the cost of living adjustment to your monthly checks. You will see the new, higher amount reflected in your standard January payment. Just ensure that your mailing address and direct deposit information are up to date on your online Social Security portal.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply