Securing your financial comfort during retirement demands proactive inflation planning, especially when confronting a smaller COLA than you may have grown accustomed to in recent years. By making strategic adjustments to your fixed income management, you can confidently protect your purchasing power and maintain the lifestyle you worked so hard to build. Rather than viewing a modest cost-of-living adjustment as a setback, use it as an opportunity to optimize your retirement budgeting and discover new efficiencies in your daily spending. This guide provides actionable retiree strategies designed to help you stretch your dollars further, maximize your existing assets, and ensure your golden years remain genuinely blissful. Implementing these practical shifts today will keep your financial foundation strong tomorrow.

Tip #1: Conduct a Comprehensive Spending Audit

When adjusting to a smaller COLA, your first line of defense is a thorough, honest review of your outgoing cash flow. Many older adults operate on autopilot with their monthly expenses; paying for services or conveniences they no longer actively use. Print out your last three months of bank and credit card statements, and carefully highlight every single recurring charge. You might discover an unused television streaming service, an overpriced mobile phone plan, or a specialized gym membership you rarely visit.

Canceling just three redundant subscription services can instantly put hundreds of dollars back into your annual budget. This auditing process forms the absolute bedrock of effective retirement budgeting. Once you strip away the waste, you can confidently redirect those exact funds toward essential categories like high-quality groceries and ongoing healthcare. Group your spending into fixed necessities and discretionary lifestyle items. Knowing exactly where every dollar goes empowers you to make rapid adjustments when economic conditions naturally shift.

Consider calling your internet, cable, or cellular provider directly to negotiate a better monthly rate. Corporate loyalty departments often possess the authority to apply unadvertised senior discounts to your account simply because you took the time to ask. By taking firm command of your daily and monthly expenses, you effectively shield yourself from the subtle sting of inflation and build a highly durable financial foundation for the decades ahead.

Tip #2: Optimize Your Medicare and Healthcare Costs

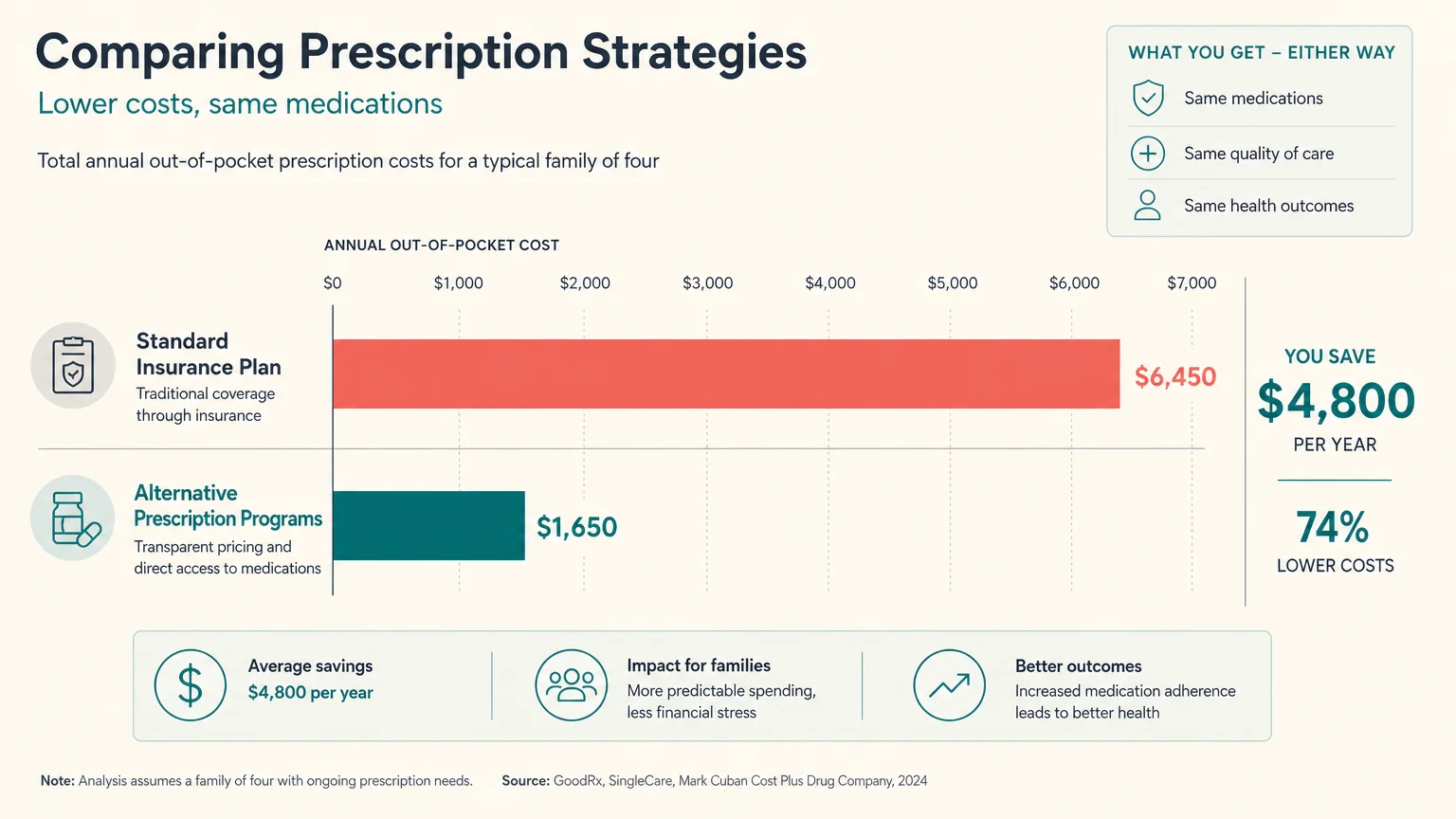

Healthcare costs consistently outpace general inflation, making medical expenses a highly critical target for optimization. If you rely on Medicare, treating the annual Open Enrollment period as a mandatory financial checkup is absolutely vital for long-term inflation planning. Part D prescription drug plans aggressively modify their formularies and pricing tiers every single year. The health plan that offered the best value last year might significantly increase its premiums or mysteriously shift your daily medication to a much more expensive tier this year.

Use the official plan finder tool on the Medicare website to vigorously compare your current coverage against all new local offerings. Simply inputting your exact prescription list can quickly reveal alternative insurance plans that save you hundreds, or even thousands, of dollars annually. Beyond traditional Medicare, take time to explore modern discount programs like GoodRx or Mark Cuban Cost Plus Drugs for your generic medications; occasionally, paying out-of-pocket through these direct services costs significantly less than your standard insurance copay.

Additionally, focus your energy on routine preventive care. Utilizing your free annual wellness visits and staying current on recommended vaccinations prevents incredibly costly hospitalizations down the road. Treating your routine health maintenance as a core financial strategy protects both your physical well-being and your wallet from sudden, unexpected economic shocks.

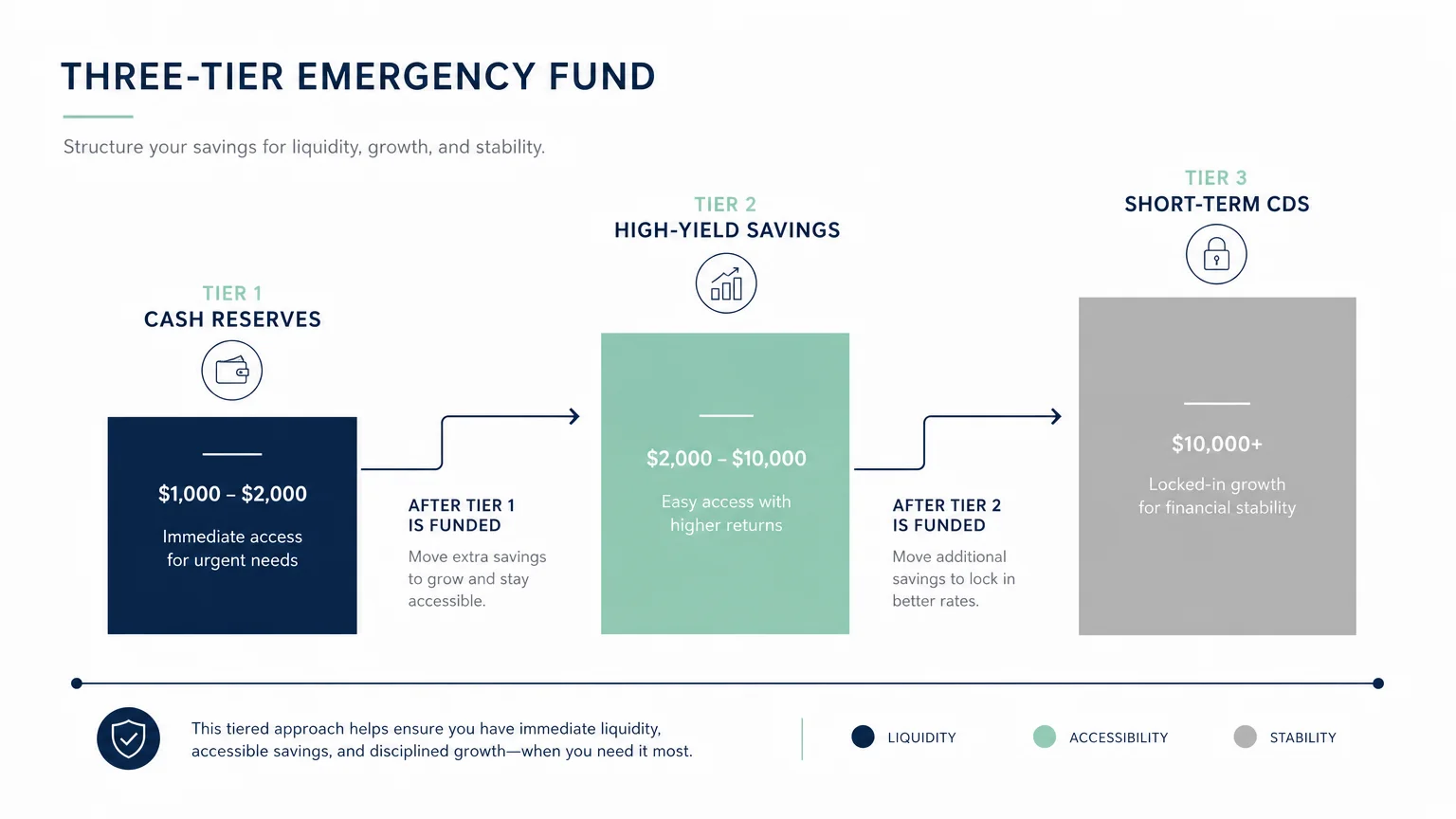

Tip #3: Implement a Tiered Emergency Fund Strategy

A robust and highly accessible emergency fund prevents you from liquidating your long-term investments during sudden market downturns. As a fundamental component of your fixed income management, structure your household cash reserves using a highly strategic tiered bucket approach. Keep three to six months of vital living expenses in an easily accessible checking or traditional savings account for immediate daily use.

Then, establish a secondary liquidity tier containing one to two full years of living expenses in slightly higher-yielding, exceptionally safe vehicles like short-term Certificates of Deposit (CDs) or government-backed Treasury bills. This specific approach guarantees you have reliable, stress-free cash flow regardless of broader market volatility or a surprisingly small Social Security adjustment from the federal government. When your primary income sources lag behind the actual rising cost of living, you can confidently draw from these specific reserves without selling your equities at a painful loss.

Earmarking specific funds for immediate lifestyle needs entirely removes the severe anxiety usually associated with daily stock market fluctuations. You built your retirement nest egg meticulously over several decades; organizing it into distinct, purpose-driven time horizons ensures your hard-earned money is precisely where you need it, exactly when you need it. This systematic cash management strategy provides profound and lasting peace of mind.

Tip #4: Leverage High-Yield Savings and CDs

Earning meaningful, compounded interest on your cash holdings requires moving decisively beyond traditional brick-and-mortar neighborhood banks. Conventional savings accounts frequently pay absolutely abysmal interest rates—often hovering around a negligible 0.01 percent. In stark contrast, modern online high-yield savings accounts typically offer extremely competitive rates exceeding 4 or 5 percent, depending on the current federal funds rate.

If you keep $40,000 in a conventional local checking account, you might earn a meager $4 a year. Moving that exact same amount to a high-yield account generating a 4.5 percent return yields an impressive $1,800 annually. That substantial additional income effortlessly offsets a smaller COLA without requiring you to lift a finger, take on any market risk, or sacrifice your precious free time. Seek out reputable online institutions that explicitly carry full FDIC insurance, ensuring your principal remains entirely safe from institutional failure.

Building a CD ladder represents another exceptionally smart tactic for generating highly predictable returns. By purchasing individual CDs that mature at staggered intervals—such as three, six, nine, and twelve months—you continuously capture strong interest rates while seamlessly maintaining periodic access to your cash. Maximizing the guaranteed yield on your safest assets is a completely risk-free method of actively giving yourself the annual raise that the government did not provide.

Tip #5: Embrace the Power of Senior Discounts and Memberships

Never underestimate the massive compound power of age-based consumer discounts. Many older adults feel inexplicably hesitant to ask for specific senior rates, yet consistently claiming these targeted benefits remains one of the most highly effective retiree strategies available today. Start your search directly with your local county government; numerous municipalities offer substantial property tax exemptions, rate freezes, or payment deferrals for residents over the age of 65 who meet specific income thresholds. A successfully approved application can permanently shave thousands of dollars off your absolute largest annual tax burden.

Next, audit your routine grocery shopping habits. Many regional supermarket chains designate specific days of the week where seniors automatically receive 5 to 10 percent off their entire checkout purchase. Aligning your weekly shopping trips exclusively with these discount days yields remarkably significant annual savings that compound beautifully over time.

Apply this exact same proactive mindset to your automotive and comprehensive home insurance policies. Completing a simple, locally certified defensive driving course often legally obligates your auto insurer to drastically reduce your monthly premiums for up to three full years. Your age and extensive life experience are highly valuable financial assets; leverage them relentlessly to negotiate much lower prices across every single sector of your personal economy.

Tip #6: Downsize Your Housing or Utility Expenses

Utility bills represent a major variable expense that directly threatens your monthly cash flow during stubborn inflationary periods. You can aggressively combat rising energy costs by initiating a comprehensive home efficiency audit. Most local utility companies offer entirely free in-home assessments where a trained professional identifies precisely where your residence loses costly heating or cooling.

Simple, highly inexpensive weekend projects—like applying thick weatherstripping to drafty exterior doors, adding blown-in insulation to your attic, or installing heavy thermal curtains over large windows—dramatically reduce your monthly energy consumption. Upgrading to an affordable smart thermostat allows you to automatically optimize your home’s temperature while you sleep or travel, trimming your overall utility bills by up to 15 percent annually.

If you currently maintain a much larger home filled with empty bedrooms, thoughtfully consider whether downsizing aligns with your current and future lifestyle goals. Selling a large property to purchase a smaller, vastly more energy-efficient residence not only cuts your utility and maintenance costs but often unlocks incredibly substantial home equity. Redirecting that previously trapped equity into safe, income-producing investments provides a robust financial cushion that easily compensates for underwhelming cost-of-living adjustments.

Tip #7: Create Joyful Secondary Income Streams

Creating a secondary, highly flexible income stream completely neutralizes the negative impact of a smaller COLA while actively keeping your mind sharp and deeply engaged. The modern gig economy offers unprecedented scheduling flexibility, allowing you to generate meaningful revenue strictly on your own terms. Consider creatively monetizing a lifelong hobby or strategically leveraging the specialized skills you acquired during your primary professional career.

If you spent several decades in management, human resources, or accounting, offer freelance consulting services strictly to small local businesses in your town. If you genuinely love animals, sign up for popular pet-sitting platforms like Rover; routinely walking neighborhood dogs provides both excellent cardiovascular exercise and a surprisingly lucrative supplemental income.

Earning just $400 or $500 extra a month provides a massive, impenetrable buffer against rising inflation. Furthermore, part-time work offers profound social and emotional benefits. Engaging regularly with your local community, actively mentoring younger professionals, and learning exciting new technologies powerfully combats the isolation that sometimes accompanies full retirement. You control your schedule entirely—working only when you genuinely want to, for exactly as long as you want to. This highly proactive approach transforms lingering financial anxiety into a deeply empowering opportunity for personal growth and community contribution.

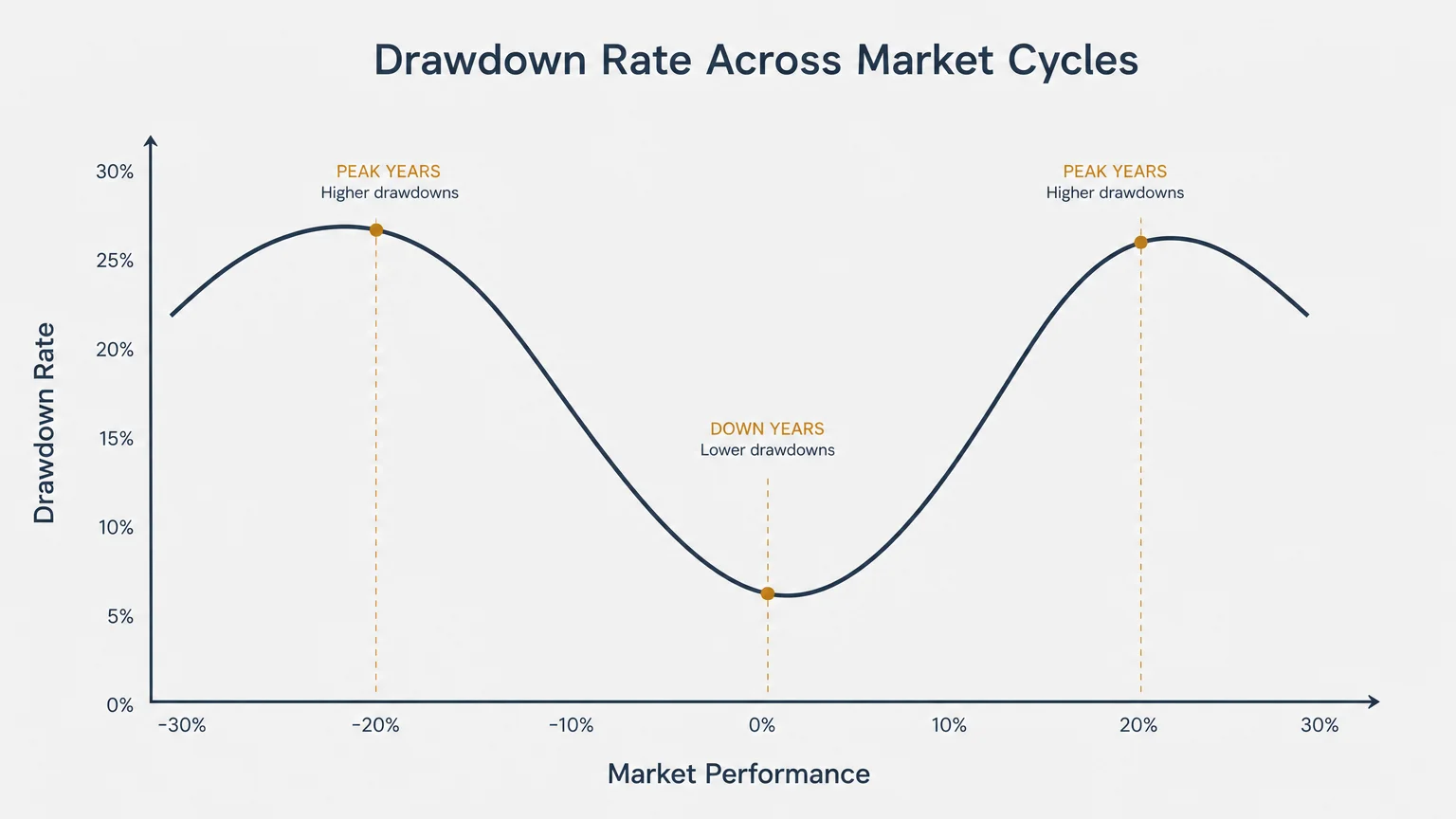

Tip #8: Adopt a Flexible Drawdown Approach for Investments

Your portfolio withdrawal strategy must remain highly adaptable to successfully survive shifting and unpredictable economic climates. Rigorously following the traditional, rigid “4 percent rule”—which strictly suggests increasing your withdrawal amount by the inflation rate every single year—can deplete your assets dangerously fast during turbulent bear markets.

Instead, adopt a highly dynamic drawdown approach commonly referred to by financial planners as the “guardrails” strategy. Under this specific system, you agree to skip your personal portfolio inflation adjustment entirely during calendar years when the broader stock market experiences significant negative returns. By tightening your belt temporarily and relying slightly more heavily on your safe cash reserves, you grant your equity investments the necessary time to fully recover their lost value.

Conversely, during years of truly exceptional market performance, you can safely grant yourself a much larger raise or distribute a special financial bonus to your various savings buckets. Flexibility is the ultimate, non-negotiable key to extreme longevity in modern retirement planning. By dynamically aligning your portfolio withdrawals with actual stock market conditions rather than strictly following arbitrary inflation targets, you carefully safeguard your principal and ensure your accumulated wealth comfortably outlives you.

The Takeaway: Living a More Blissful Retirement

Adapting smoothly to inevitable economic shifts is a completely natural, highly manageable phase of your ongoing financial journey. A modest or disappointing increase in your Social Security benefits absolutely does not have to spell disaster for your carefully planned lifestyle. By taking immediate, proactive steps to streamline your monthly budget, maximize your safe cash yields, and flexibly manage your investment withdrawals, you effectively build an impenetrable fortress around your retirement savings.

You already possess decades of hard-earned life experience and incredible personal resilience; applying that profound wisdom directly to your current finances guarantees you remain firmly and confidently in the driver’s seat. Embrace these minor financial adjustments not as painful sacrifices, but as incredibly smart, empowering optimizations that ultimately free up vital resources for the wonderful experiences and beloved people you value most.

Stay highly engaged with your community, stay intellectually curious about new financial tools, and continuously seek out entirely new avenues for personal efficiency. The golden years are truly meant to be thoroughly cherished. With the right dynamic strategies firmly in place, you can confidently navigate absolutely any economic environment while enjoying the deeply blissful, perfectly secure retirement you absolutely deserve.

Frequently Asked Questions

Why is the COLA sometimes smaller than expected?

The Social Security Administration carefully calculates the annual cost-of-living adjustment strictly based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) specifically from the third quarter of the year. If general consumer inflation cools down during those specific measurement months, the resulting adjustment will be definitively lower, even if prices for your personal healthcare or groceries still feel incredibly high to you.

Can I negotiate my fixed expenses to help offset inflation?

Absolutely. Many proactive retirees successfully negotiate substantially lower rates for internet service, cellular plans, and comprehensive home insurance. Companies almost always prefer to keep you as a paying customer rather than completely lose your business to a local competitor. Call your service providers annually, mention clearly that you are auditing your expenses for retirement budgeting, and ask directly if any new promotional rates or specialized senior discounts apply to your account.

How much of my portfolio should I keep in cash?

While individual financial needs always vary, professional financial planners generally recommend that retirees maintain one to two full years’ worth of living expenses in highly liquid, exceptionally safe accounts. This critical cash buffer absolutely prevents you from having to sell off your stocks during a sudden market downturn just to cover your daily bills, providing immense stability when broader economic conditions change unexpectedly.

Do I need to hire a financial advisor to manage these changes?

While you can successfully implement many of these budgeting and targeted savings strategies entirely independently, consulting a licensed, fiduciary financial advisor provides deeply personalized guidance. An expert helps you mathematically stress-test your existing portfolio and meticulously design a dynamic withdrawal strategy flawlessly tailored to your specific life goals, ensuring you remain completely confident during heavily fluctuating economic cycles.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply