Understanding how the government determines your annual Social Security increase allows you to better project your income and safeguard your financial security. While many retirees simply wait for the official announcement each fall, learning the mechanics behind this critical percentage gives you a clear advantage when planning your monthly budget. Your cost-of-living adjustment relies on a specific set of economic data gathered during a tight three-month window; everyday price fluctuations throughout the rest of the year do not directly influence your final raise. By breaking down the specific rules, indexes, and deductions that shape this process, you can build a more resilient financial strategy and enjoy your hard-earned retirement with greater peace of mind.

Tip #1: The Consumer Price Index for Urban Wage Earners

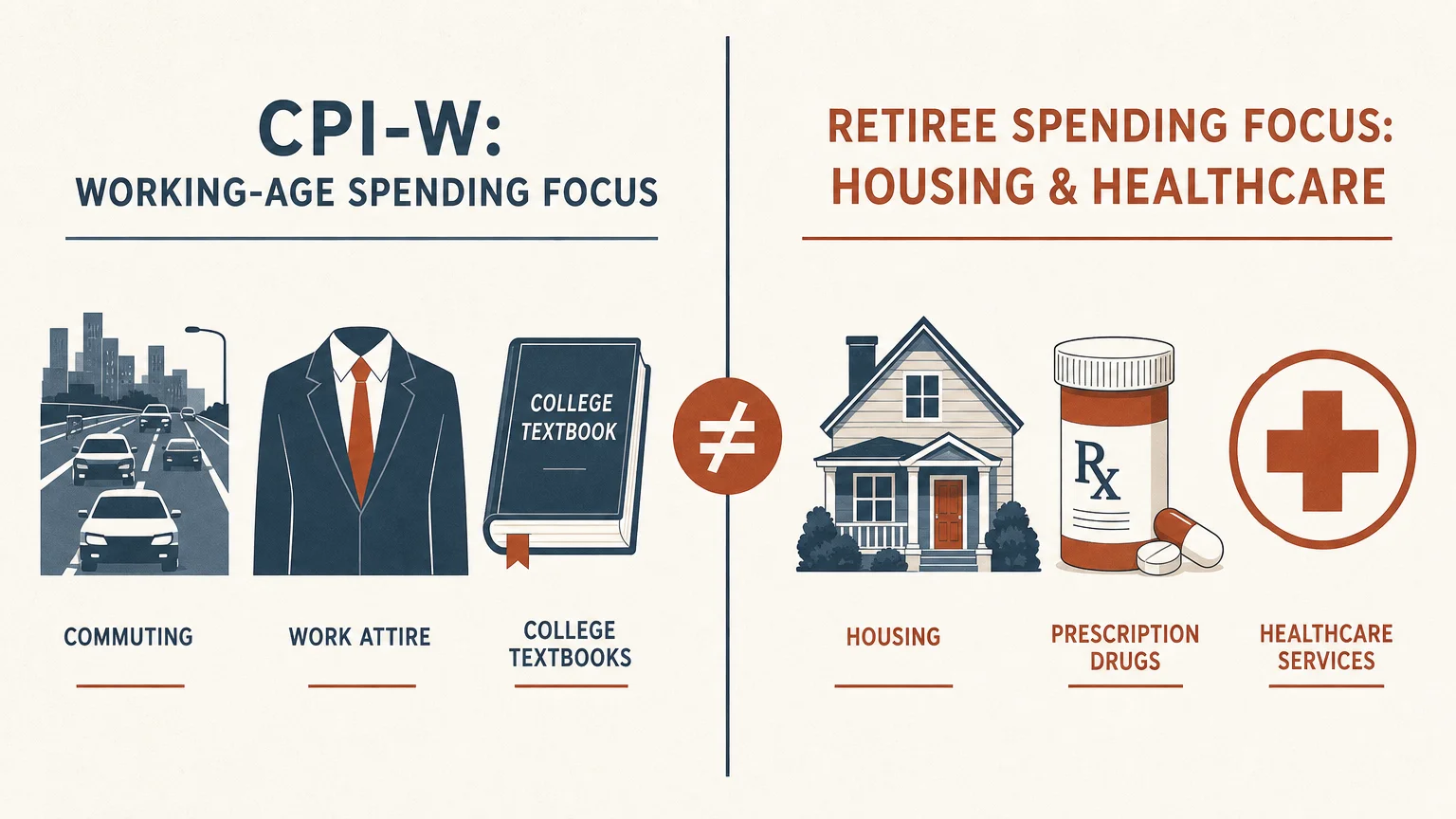

You might assume the government measures your specific cost of living to determine your annual raise. However, the Social Security Administration uses the Consumer Price Index for Urban Wage Earners and Clerical Workers—commonly known as the CPI-W. This specific index tracks the spending habits of younger, working-age Americans rather than retirees. These younger workers spend a significant portion of their income on commuting costs, professional clothing, and education. You likely allocate your money quite differently. Older adults typically dedicate a much higher percentage of their fixed budgets to healthcare, prescription medications, and housing.

Because the CPI-W heavily weighs transportation and apparel over medical care, the resulting COLA calculation rarely reflects your actual day-to-day expenses. For instance, if gasoline prices drop dramatically during the year, the CPI-W decreases significantly. This drop drives down the overall percentage of your raise, even if your prescription medication costs rise by ten percent during that exact same period. Advocates frequently push lawmakers to adopt the CPI-E, an index tailored specifically to the elderly, but current federal law still mandates the use of the CPI-W.

You must recognize this fundamental disconnect so you can plan your budget realistically. Knowing that your official raise relies on the spending patterns of younger workers helps you understand why your personal expenses sometimes outpace your annual increase. Adjust your expectations accordingly and build extra flexibility into your monthly spending plan to accommodate costs the CPI-W simply ignores.

Tip #2: The Crucial Third-Quarter Timeframe

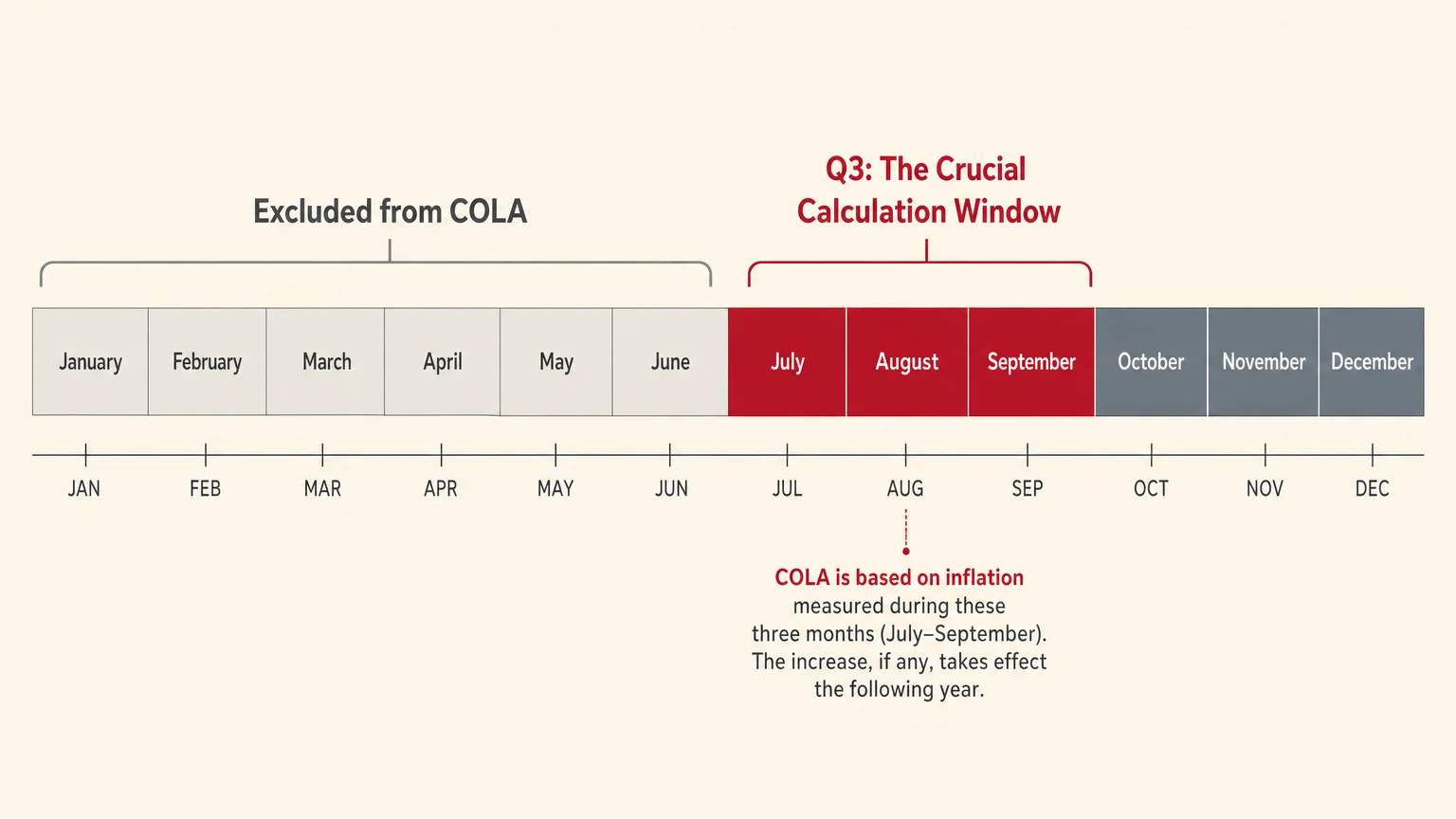

Your annual increase does not capture a full twelve months of inflation factors. The government strictly calculates your raise using data from a very specific window: the third quarter of the year. This means only the economic data from July, August, and September matter for your upcoming adjustment. The Social Security Administration compares the average CPI-W from these three specific months to the average from the exact same three months of the previous year. If the index rises, you receive a percentage increase matching that growth. If the index remains flat or drops, your benefit amount stays exactly the same.

This rigid timeframe explains why mid-winter heating spikes or springtime grocery price surges do not guarantee a higher raise. When heavy inflation cools off right before the summer, your official adjustment might appear surprisingly low, even if you spent the previous six months paying sky-high prices at the supermarket. The system essentially ignores any financial pain you experience from January through June.

You can track these specific economic indicators yourself. Watch the monthly consumer price reports released by the Bureau of Labor Statistics during the late summer. Monitoring these specific data releases gives you a highly accurate preview of your upcoming raise long before the official October announcement. Use this valuable knowledge to adjust your holiday savings plan early; if the third-quarter numbers look weak, you can proactively trim your discretionary spending before the new year even begins.

Tip #3: The Impact of Rising Medicare Part B Premiums

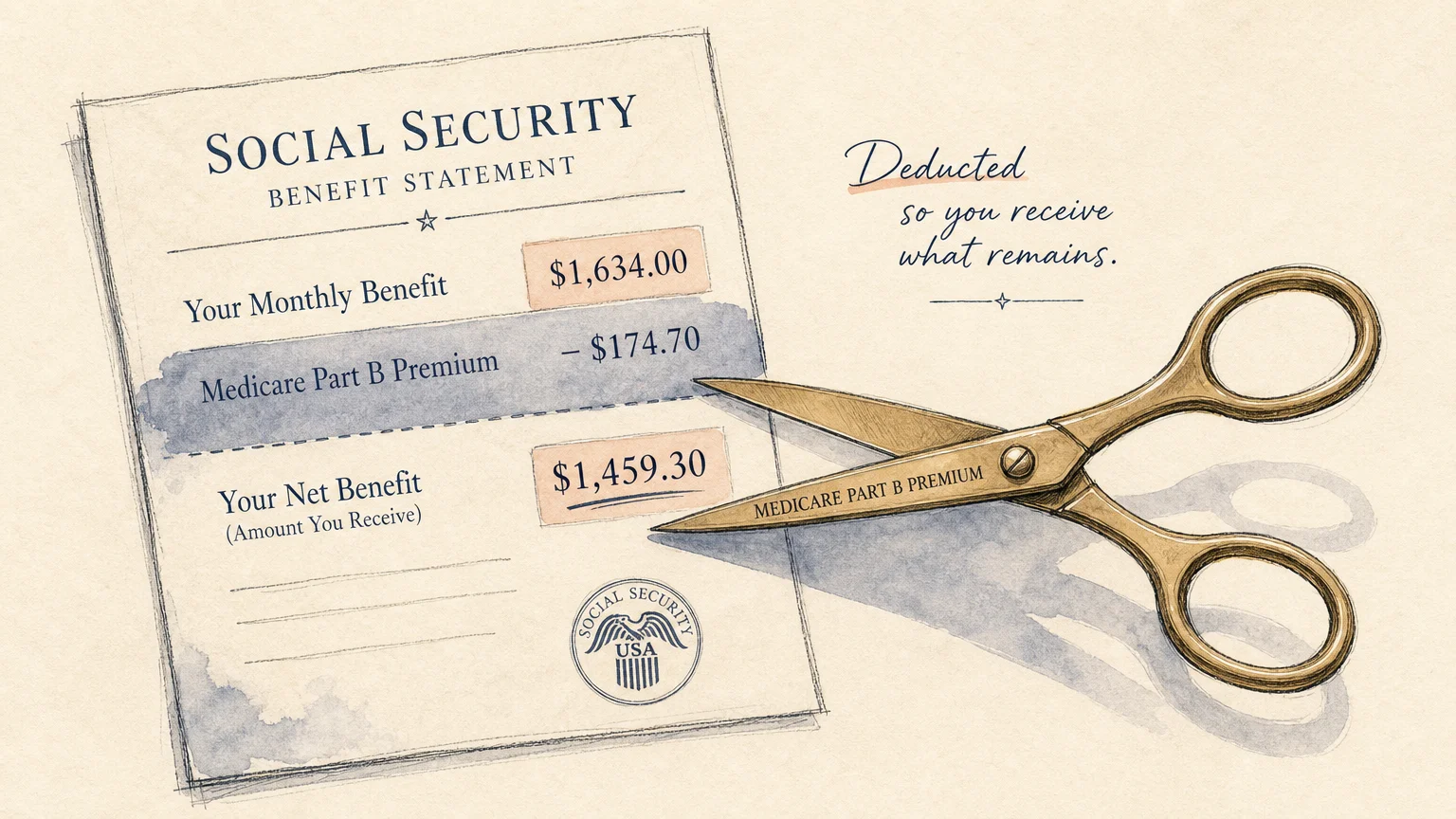

Many retirees forget to account for their healthcare premiums when estimating their new monthly income. The government automatically deducts your standard Medicare Part B premium directly from your Social Security checks. When your COLA increases, Medicare premiums frequently rise right alongside it. This concurrent increase directly impacts your net Social Security adjustments.

If the government announces a three percent benefit increase, you might immediately calculate a generous bump to your bank account. However, if Medicare Part B premiums jump significantly that same year, the higher premium consumes a large portion of your raise before you ever see the money. For example, if your raise equals fifty dollars a month, but your Medicare premium increases by twenty dollars, your actual take-home increase is only thirty dollars.

Fortunately, a federal rule called the hold harmless provision protects most retirees from actual benefit reductions. This law ensures your standard Medicare premium increase cannot reduce your net Social Security benefit below what you received the previous year. If your premium rises faster than your adjustment, the government caps the premium increase so your overall check does not shrink. However, you must remember that the hold harmless rule does not apply to higher-income retirees subject to the Income-Related Monthly Adjustment Amount. Always subtract projected Medicare premium increases when forecasting your available spending money for the upcoming year.

Tip #4: Local Versus National Economic Indicators

The annual cost-of-living adjustment represents a nationwide average. The government applies this single percentage uniformly to every recipient across the country, regardless of where they live. Unfortunately, inflation does not distribute itself evenly across all fifty states or even across different counties within the same state. Regional economic indicators play a massive role in your personal financial reality.

If you live in a fast-growing sunbelt state, local housing prices, utility costs, and property taxes might surge at double the national average. Meanwhile, retirees residing in rural Midwestern towns might experience a much slower, more manageable rise in local living costs. When you evaluate your annual raise, you must compare it directly against your localized reality. A four percent national adjustment feels incredibly generous in a town with steady prices; that exact same percentage feels woefully inadequate in a booming metropolitan area facing skyrocketing rent and insurance rates.

You cannot control the federal percentage, but you maintain absolute control over your location and your localized spending. Evaluating your community’s actual cost of living helps you determine whether your retirement benefits truly cover your needs. If local expenses consistently outpace your federal adjustments year after year, you might consider relocating. Moving to an area with lower property taxes, affordable utilities, and stable grocery prices can instantly stretch your fixed income and provide significant financial relief.

Tip #5: The Disproportionate Weight of Healthcare and Housing

Even though the official CPI-W tracks general inflation effectively for the broader workforce, it severely underestimates the two largest expenses you face in retirement: healthcare and housing. Medical costs historically rise much faster than the general inflation rate. As you age, you pay for supplementary insurance policies, specialized prescription co-pays, extensive dental work, and vision care completely out of your own pocket. The CPI-W assigns a relatively low weight to these specific medical expenses because younger, healthier workers generally consume far less healthcare.

Housing creates an equally frustrating challenge. While you might own your home outright, you still face climbing property taxes, soaring homeowners insurance premiums, and relentless maintenance costs. The federal index often relies on a theoretical metric called owners equivalent rent to measure housing costs. This abstract metric does not accurately capture the sudden, devastating financial shock of a doubled insurance premium or an unavoidable roof replacement.

Because the official COLA calculation fails to weigh these senior-specific expenses accurately, you must build a robust buffer into your financial plan. Dedicate a specific, untouchable portion of your savings strictly to a healthcare emergency fund. Shop aggressively for better home and auto insurance rates every single year to combat regional rate hikes. You simply cannot rely on your annual government adjustment to absorb the full impact of these specific, fast-growing categories.

Tip #6: Tax Thresholds on Your Retirement Benefits

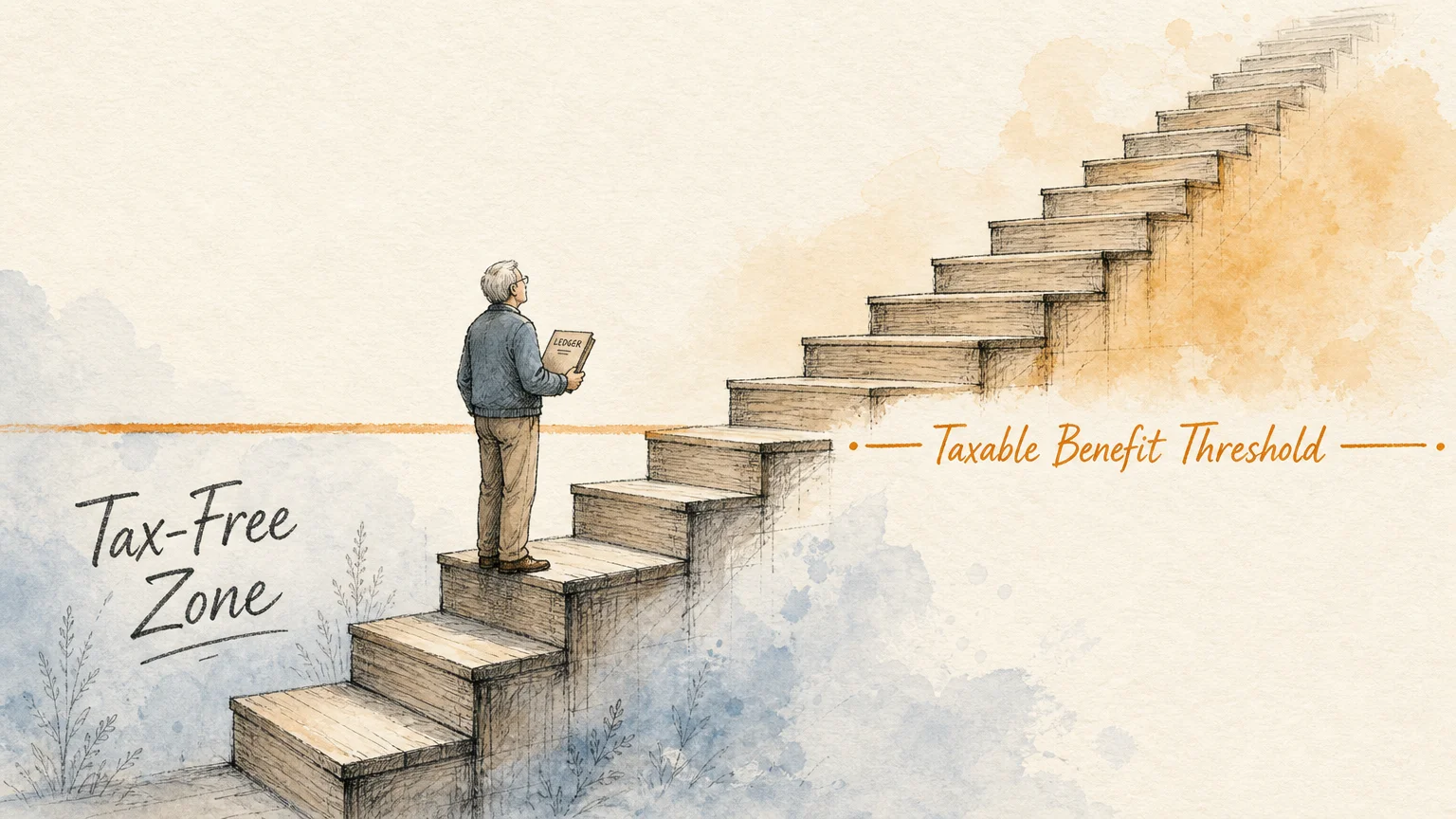

A generous cost-of-living increase looks wonderful on paper, but it sometimes creates an unexpected and frustrating tax burden. The Internal Revenue Service taxes your retirement benefits based on specific combined income thresholds. You must understand that Congress established these rigid thresholds decades ago, and unlike your benefits, these figures do not automatically adjust for inflation.

To determine your combined income, you add your adjusted gross income, your nontaxable interest, and half of your yearly Social Security benefits. If you file as a single individual and your combined income exceeds $25,000, up to fifty percent of your Social Security benefits become taxable. If your combined income surpasses $34,000, up to eighty-five percent becomes taxable. When a high inflation year produces a massive adjustment, that extra money can easily push your total income right past these stagnant thresholds.

You might suddenly find yourself owing federal taxes on your benefits for the very first time, or owing a significantly higher percentage than you did the previous year. This hidden factor essentially penalizes you for receiving a larger raise. You must proactively manage your taxable income to minimize this impact. Work closely with a qualified tax professional to carefully time your withdrawals from traditional retirement accounts. Strategic tax planning keeps your overall income below these critical lines.

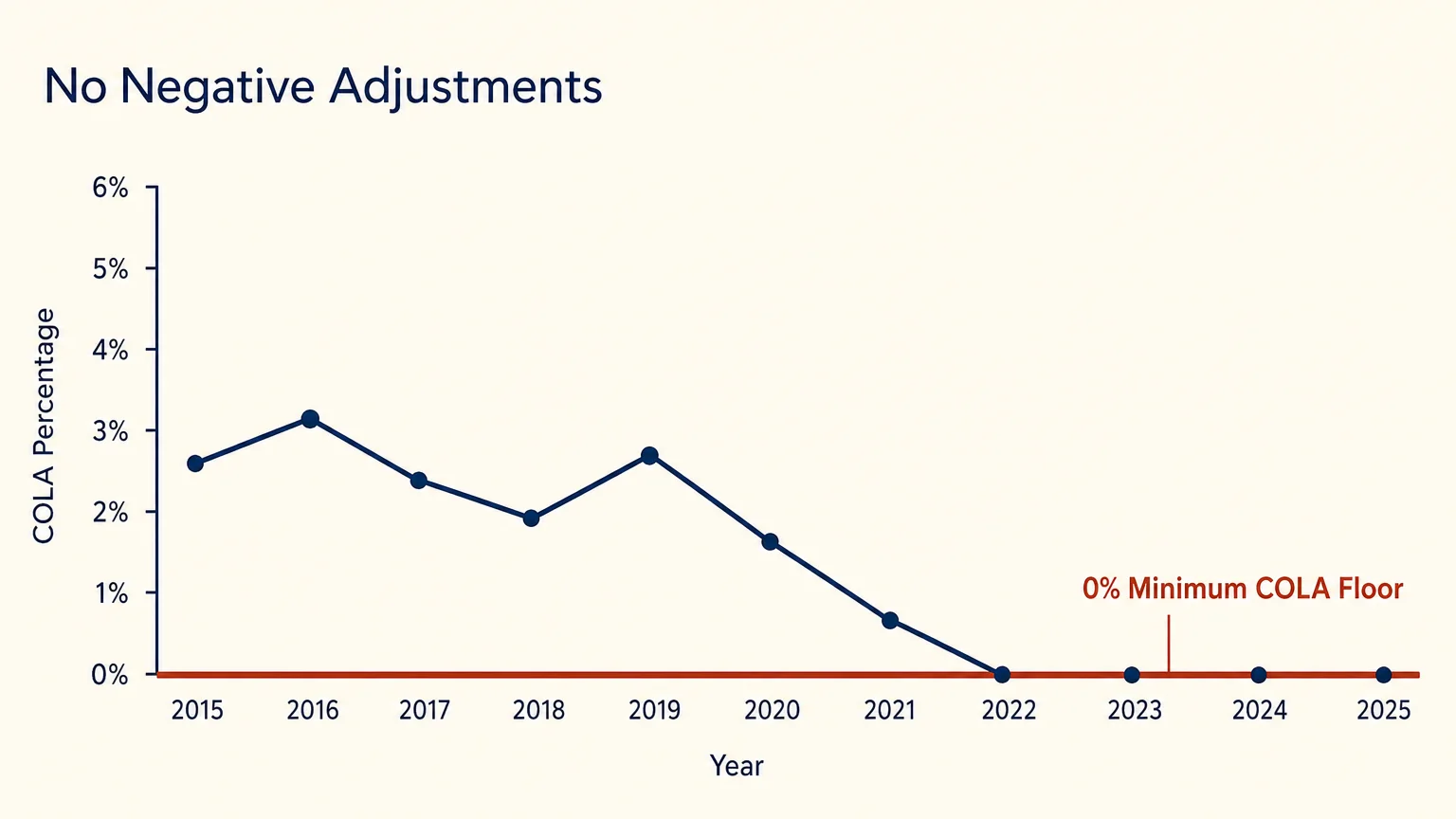

Tip #7: The Absence of a Minimum Guaranteed Increase

You might comfortably assume your monthly benefits will grow every single year to keep pace with modern life. The reality is quite different. Federal law absolutely does not guarantee a minimum annual increase. When the specific economic indicators show zero inflation, or when the overall economy actually experiences deflation, your cost-of-living adjustment drops to exactly zero percent. You will not receive a pay cut, but you will not receive a single extra penny, either.

This exact, frustrating scenario played out in 2010, 2011, and 2016. In those years, millions of retirees received absolutely no increase to their monthly checks. This harsh reality makes long-term financial planning incredibly challenging for anyone entirely dependent on federal benefits. You cannot safely assume an automatic three or four percent bump year after year. When national inflation vanishes, your income flatlines.

During these stagnant years, your unique personal expenses—like local utility rates, property taxes, or specialized dietary groceries—might still creep upward, aggressively squeezing your budget from all sides. You must protect yourself by diversifying your income streams well before you actually need the money. Build a resilient portfolio of dividend-paying stocks, utilize high-yield savings accounts, or invest in short-term certificates of deposit. Creating multiple sources of reliable income ensures you never have to depend entirely on a government calculation to pay your everyday bills.

The Takeaway: Living a More Blissful Retirement

Navigating the complexities of your retirement benefits requires vigilance, continuous education, and a proactive mindset. The hidden factors that dictate your annual increase—from the spending habits of younger workers to the rigid third-quarter measurement window—prove that your official raise rarely aligns perfectly with your personal reality. When you understand the profound impact of rising Medicare premiums, localized economic shifts, and static tax thresholds, you take control of your financial destiny.

You no longer have to wait passively for an October announcement to plan your life. By building separate emergency funds for healthcare and housing, diversifying your secondary income streams, and aggressively managing your taxable withdrawals, you insulate yourself from the unpredictable nature of federal adjustments. Use these practical insights to craft a resilient, flexible budget that works for your unique lifestyle. When you stop relying solely on a government calculation to maintain your standard of living, you open the door to a much happier, more secure future. Embrace these strategies today, and step confidently into the joyful, deeply fulfilling retirement you truly deserve.

Frequently Asked Questions

How does the government measure inflation for seniors?

The government officially measures inflation using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index monitors the costs of everyday goods and services purchased by younger, working-age people. Although advocates frequently campaign for the use of an elderly-specific index (CPI-E) that weighs medical care and housing more heavily, current law requires the Social Security Administration to use the standard CPI-W.

Can my net Social Security check actually go down?

Generally, a protective rule called the hold harmless provision prevents your net Social Security check from decreasing due to standard Medicare Part B premium hikes. If the Medicare premium increase exceeds your annual cost-of-living adjustment, the government caps your premium cost to ensure your take-home benefit remains at least the same as the previous year. However, high-income earners who pay IRMAA surcharges do not qualify for this protection and might see a reduction.

Why is my personal cost of living higher than the official COLA?

The official percentage reflects a national average based on a specific basket of goods. Your personal cost of living depends entirely on your regional economic indicators and individual spending habits. If you live in an area with soaring property taxes, or if you spend a large portion of your income on out-of-pocket healthcare, your personal expenses will inevitably outpace the generalized federal adjustment.

Do I have to pay taxes on my cost-of-living increase?

Your adjustment increases your overall gross income, which can push you into a higher tax bracket. Because the Internal Revenue Service does not automatically adjust the taxation thresholds for Social Security benefits to match inflation, a larger monthly check might cause up to eighty-five percent of your total benefits to become taxable depending on your combined annual income.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply