Retirement travel planning unlocks the world, but protecting your health requires understanding the critical gap between senior travel insurance and standard Medicare. You can explore the globe with absolute peace of mind once you secure the right coverage for medical emergencies and trip cancellations. Original Medicare generally stops providing coverage the moment you step outside the United States; relying on it for an overseas vacation leaves you exposed to massive medical bills. By mastering the differences between Medicare supplements and dedicated travel medical insurance, you ensure your adventures remain joyful and stress-free. Let us explore exactly what your domestic policies cover and how to select the perfect protection for your upcoming journeys.

Tip #1: Understand the Limits of Original Medicare Travel Coverage

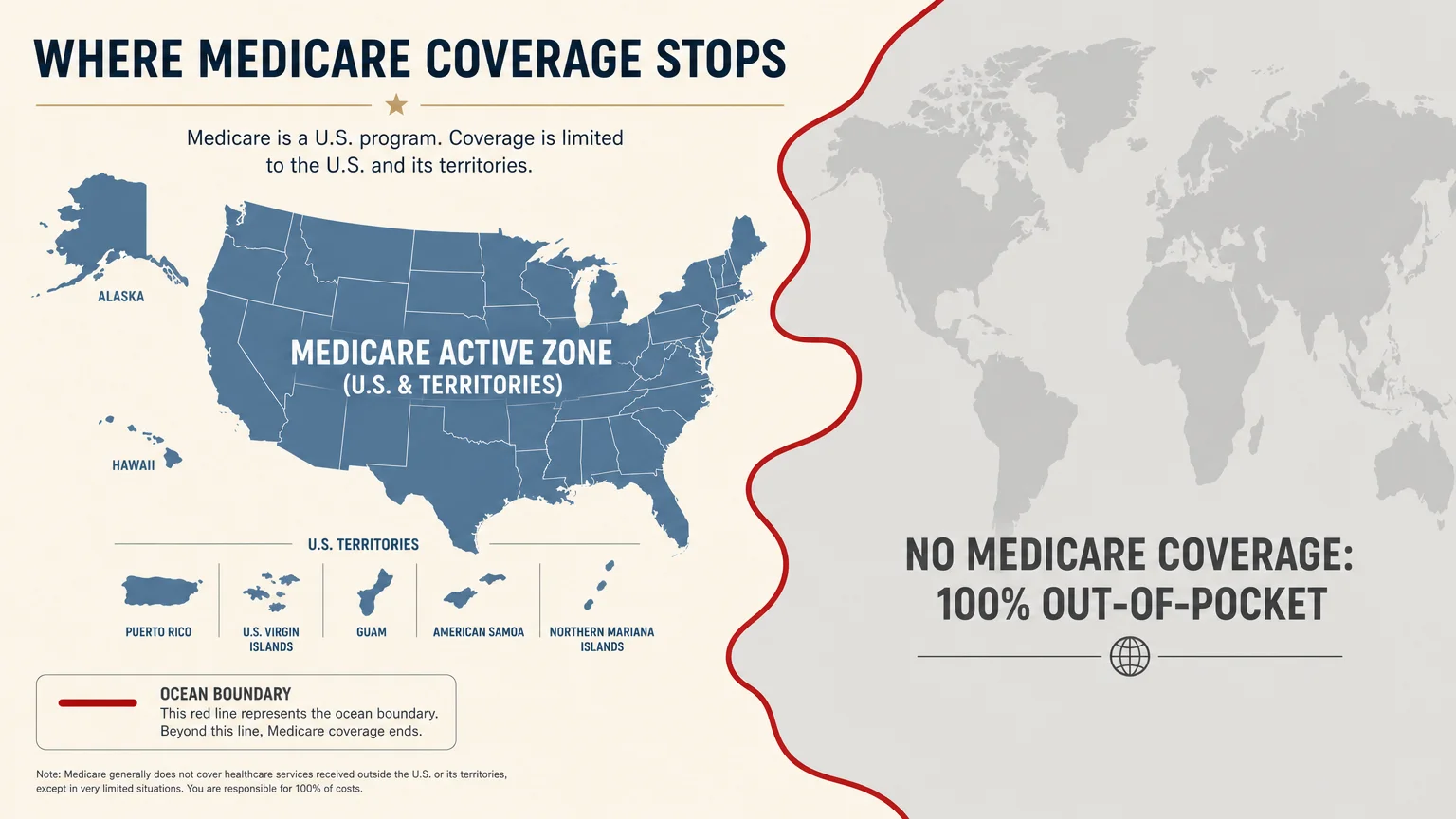

Original Medicare provides phenomenal health coverage within the borders of the United States and its territories, including Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa, and the Northern Mariana Islands. However, once you travel outside these specific areas, Medicare travel coverage drops significantly. You must understand that standard Medicare Parts A and B simply do not pay for healthcare services or supplies received outside the country; this leaves you fully responsible for 100 percent of any international medical bills.

There are three extremely rare exceptions where Original Medicare might step in. First, if you experience a medical emergency while physically in the United States, but a foreign hospital happens to be closer than the nearest domestic facility, Medicare may cover your care. Second, if you travel through Canada via the most direct route between Alaska and another state and a medical emergency occurs, coverage might apply. Finally, if you live in the United States and a foreign hospital is closer to your home than a U.S. hospital—regardless of an emergency—Medicare might approve treatment there.

Beyond these highly specific, incredibly rare scenarios, you are entirely on your own. Prescription drugs purchased overseas are never covered by Medicare Part D. Routine medical care, sudden debilitating illnesses, or traumatic injuries sustained on a European river cruise or a tropical beach will require immediate, out-of-pocket payments. This startling reality highlights exactly why senior travel insurance becomes a non-negotiable addition to your vacation budget. Recognizing these rigid domestic boundaries allows you to plan effectively and secure the supplemental protection required for a carefree journey.

Tip #2: Explore Medigap Plan Foreign Travel Perks

If you carry a Medicare Supplement Insurance policy—commonly known as Medigap—you might already possess a foundational layer of protection for international adventures. Specific Medigap plans offer a foreign travel emergency benefit that standard Medicare lacks. Plans C, D, F, G, M, and N provide coverage for emergency medical care received outside the United States; however, this coverage comes with strict parameters and financial limits that you must carefully review before boarding a plane.

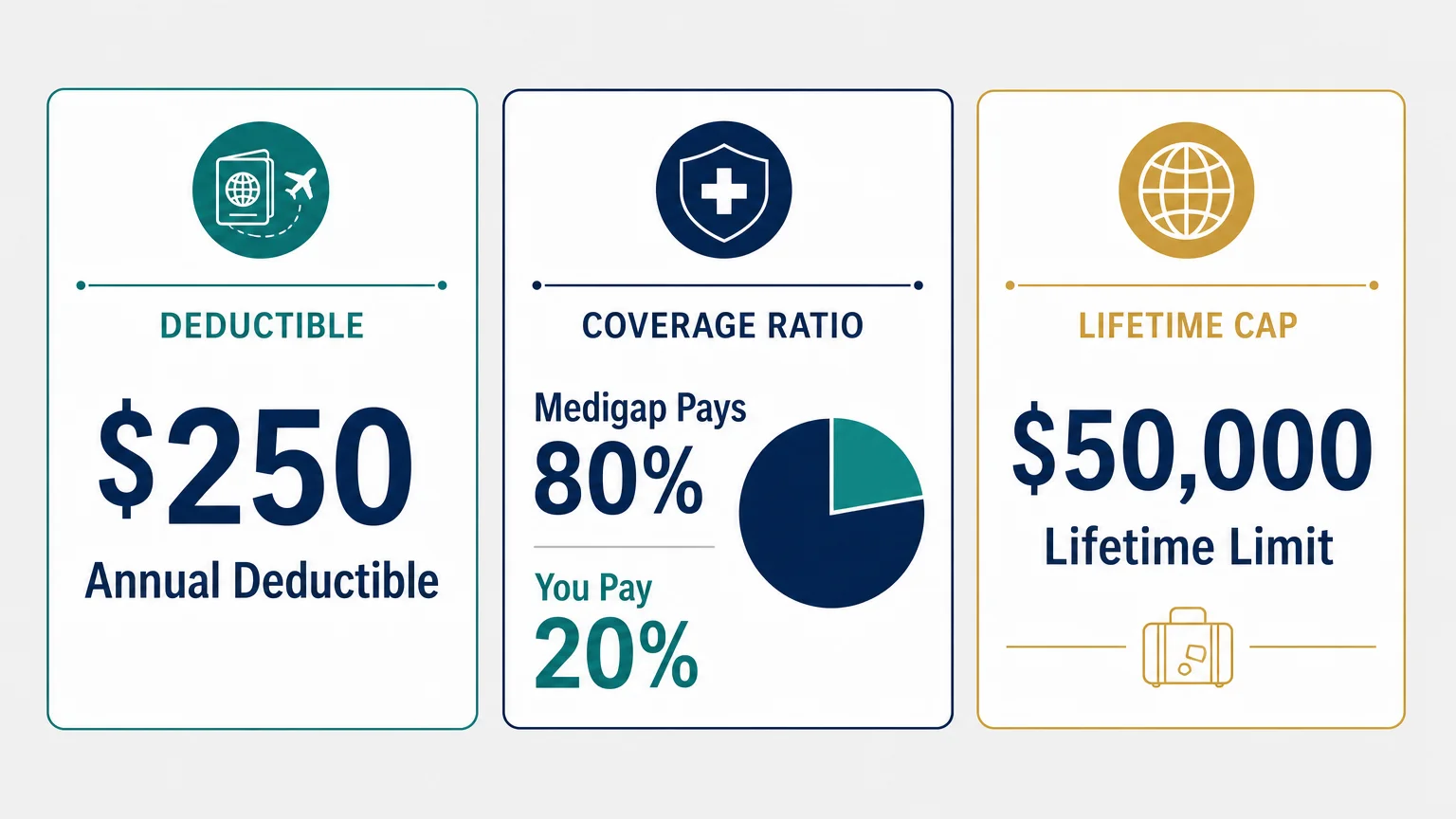

Your Medigap policy will typically pay 80 percent of billed charges for medically necessary emergency care outside the U.S., provided the care begins during the first 60 days of your trip. Before the policy kicks in, you must pay a $250 annual deductible entirely out of pocket. You also remain personally responsible for the remaining 20 percent coinsurance on every single medical bill. Most importantly, these specific Medigap policies enforce a strict $50,000 lifetime limit for foreign travel emergency care. While fifty thousand dollars sounds substantial, it depletes rapidly if you require complex surgery, extended hospitalization, or specialized medical procedures abroad.

Consider a concrete example to illustrate this critical benefit. Imagine you suffer a severe fall while exploring historic ruins in Italy, resulting in a sudden $20,000 hospital bill. You would first pay your $250 deductible, leaving $19,750. Your Medigap plan would then cover 80 percent of that remaining balance—which equals $15,800—leaving you to pay the final $3,950. This supplemental coverage certainly softens the immediate financial blow, but it also highlights the remaining gaps. A $50,000 lifetime cap offers minimal protection against truly catastrophic emergencies; therefore, relying solely on Medigap for extensive retirement travel planning leaves significant financial risk on the table.

Tip #3: Choose Comprehensive Travel Medical Insurance for Global Trips

To completely close the gaps left by standard domestic policies, you need dedicated travel medical insurance designed specifically for international explorers. While standard trip cancellation policies protect your prepaid expenses, travel medical insurance focuses entirely on your physical well-being. This specialized coverage steps in precisely where Medicare and limited Medigap plans fall short—offering robust financial safety nets for unexpected doctor visits, emergency hospitalizations, surgical procedures, and even urgent dental care while you are miles away from home.

When shopping for travel medical insurance, experts strongly recommend securing a policy that provides at least $50,000 to $100,000 in emergency medical coverage. Medical costs vary drastically around the globe; a minor procedure in Southeast Asia might cost a fraction of what it does in the United States, but specialized trauma care in Switzerland, Canada, or Japan could easily rival American hospital bills. By selecting a high coverage limit, you ensure that unexpected illnesses or severe accidents do not drain your hard-earned retirement savings.

Additionally, excellent travel medical insurance provides invaluable logistical support through 24/7 global assistance hotlines. Navigating a foreign healthcare system presents terrifying challenges when you face steep language barriers and unfamiliar medical protocols. These assistance services connect you immediately with multilingual coordinators who can locate the nearest acceptable medical facility, arrange necessary ground transportation, and communicate directly with local doctors to ensure you receive appropriate care. This level of support transforms a potential international crisis into a highly manageable situation, giving you the confidence to embrace your golden years with enthusiasm and absolute peace of mind.

Tip #4: Prioritize Medical Evacuation and Repatriation Benefits

Medical evacuation represents one of the most critical—and significantly most expensive—components of senior travel insurance. If you suffer a severe medical emergency in a remote location or a region lacking adequate healthcare facilities, you require immediate, specialized transport to a capable hospital. Medical evacuation coverage pays for specialized transportation, such as a helicopter airlift from a rugged mountain town or a medically equipped private jet from a remote island, ensuring you reach a facility equipped to save your life.

Without this indispensable coverage, arranging an emergency medical flight falls entirely on your shoulders, and the costs are absolutely staggering. A simple domestic air ambulance can easily cost $20,000, while an international medical evacuation can skyrocket well beyond $100,000 depending on your exact location and the required medical staff on board. Standard domestic health plans, including Original Medicare, explicitly exclude these exorbitant transportation costs; leaving you heavily exposed to immense financial devastation during a life-threatening crisis.

In addition to emergency evacuation, you must look closely for repatriation of remains coverage. This delicate but deeply necessary benefit ensures that, in the tragic event of a fatality abroad, the insurance company coordinates and finances the dignified return of your remains to your home country. By prioritizing travel policies that offer at least $250,000 to $500,000 in combined medical evacuation and repatriation benefits, you completely shield your family from the overwhelming logistical burdens and catastrophic expenses associated with international medical transport.

Tip #5: Look for Pre-Existing Condition Waivers

When navigating the complex landscape of travel insurance for seniors, understanding exactly how policies handle your existing health issues remains absolutely paramount. A pre-existing condition generally refers to any medical issue, chronic illness, or recent injury that required treatment, medication changes, or professional medical advice during a specific timeframe before you purchased the policy. This specific timeframe—commonly known as the look-back period—typically stretches from 60 to 180 days prior to your official insurance purchase date.

If you file a claim for a medical emergency abroad and the insurance company determines the event stemmed directly from a condition active during the look-back period, they will deny your claim entirely. Fortunately, you can easily bypass this massive hurdle by securing a pre-existing condition waiver. This crucial waiver forces the insurance provider to cover medical emergencies related to your established health issues, ensuring chronic conditions like hypertension, diabetes, or mild heart disease do not void your hard-earned travel coverage.

To obtain this indispensable waiver, you must follow strict timing rules set out by the insurance provider. The vast majority of companies require you to purchase your comprehensive travel insurance policy within 14 to 21 days of making your very first initial trip deposit—whether that deposit went toward a luxury cruise, an airline ticket, or a hotel reservation. Additionally, you must be medically fit to travel on the exact day you buy the policy. Meeting these two simple criteria secures the waiver, granting you robust protection and total peace of mind regardless of your complex medical history.

Tip #6: Secure Trip Cancellation and Interruption Protection

Retirement travel planning usually involves significant upfront financial investments, from booking luxury European river cruises to securing extended stays in tropical villas. Trip cancellation and interruption insurance safeguard these substantial non-refundable deposits against unpredictable life events. While comprehensive travel medical insurance protects your physical health, cancellation coverage acts as an impenetrable shield for your wallet, fully reimbursing you if you must suddenly abandon your travel plans before your scheduled departure.

Covered reasons for standard trip cancellation typically include severe unexpected illness, the sudden death of an immediate family member, unexpected jury duty, or a destructive weather event rendering your final destination completely uninhabitable. If a covered catastrophe strikes just two days before your flight to Paris, your policy reimburses the prepaid, non-refundable costs of your airfare, luxury hotels, and guided tours. This immense financial rescue allows you to seamlessly reschedule your dream vacation for a later date without suffering thousands of dollars in absolute loss.

Furthermore, trip interruption coverage brilliantly rescues your finances if a terrible emergency forces you to return home prematurely. Imagine you are halfway through a spectacular Alaskan cruise when a severe medical issue requires immediate evacuation. Interruption coverage reimburses the unused portion of your trip and often helps cover the exorbitant last-minute, one-way flight back home. For ultimate travel flexibility, you might consider upgrading to a Cancel for Any Reason policy; this premium add-on reimburses a significant percentage of your costs even if you simply change your mind about traveling.

Tip #7: Compare Primary vs. Secondary Coverage Options

As you meticulously finalize your senior travel insurance purchase, you will consistently encounter policies categorized as offering either primary or secondary coverage. This major distinction dictates exactly how the insurance company processes your future claims and dramatically impacts the amount of tedious paperwork you must navigate during a stressful medical recovery. Understanding this subtle but highly critical difference ensures you choose a robust policy that aligns perfectly with your desire for a completely hassle-free administrative experience.

Primary travel medical insurance securely assumes the first position in the complex claims process. If you visit a busy emergency room in London, you submit your medical bills directly to your primary travel insurance provider. They immediately process the claim and pay the eligible expenses upfront, completely bypassing your domestic health insurance network. This beautifully streamlined approach eliminates endless bureaucratic hurdles, providing rapid financial reimbursement and significantly reducing the anxiety associated with international medical billing.

Conversely, secondary travel insurance explicitly requires you to file a detailed claim with your domestic health insurance provider first. Because you already know Original Medicare generally provides absolutely zero international coverage, you must patiently wait for Medicare to officially deny your claim in writing. Only after receiving this formal denial letter can you finally submit the remaining bills to your secondary travel insurance company for reimbursement. While secondary policies often cost slightly less upfront, the exhausting paperwork and lengthy delays make primary coverage the vastly superior choice for seniors seeking a smooth experience.

The Takeaway: Living a More Blissful Retirement

Retirement offers the perfect opportunity to explore new cultures, savor exotic cuisines, and create unforgettable memories across the globe. By acknowledging the strict boundaries of Medicare travel coverage, you take the first empowering step toward responsible and secure exploration. You possess the knowledge necessary to evaluate Medigap limits, prioritize crucial medical evacuation benefits, and secure vital pre-existing condition waivers. Investing in comprehensive travel medical insurance provides more than just financial reimbursement; it delivers profound peace of mind. You can step onto a plane knowing that, should the unexpected occur, you have a robust safety net ready to catch you. Embrace your upcoming adventures with absolute confidence, secure in the knowledge that your health, your finances, and your family remain thoroughly protected every step of the way.

Frequently Asked Questions

Does Medicare Advantage (Part C) offer better international travel coverage?

Medicare Advantage plans replace Original Medicare and are sold by private insurance companies, meaning their rules vary significantly from standard Medicare. Some Advantage plans do offer limited coverage for international medical emergencies; however, you must carefully read your specific policy documents. Even if your plan includes foreign travel perks, the coverage often functions strictly as secondary insurance, requires high co-pays, and rarely covers expensive medical evacuation flights. You should still purchase dedicated travel medical insurance to fill these precarious gaps securely.

How does age affect the cost and availability of senior travel insurance?

Insurance premiums naturally increase as you age, reflecting the statistically higher risk of medical emergencies and trip cancellations. Once you reach the ages of 70, 80, or 85, you will notice noticeable price jumps in comprehensive policies. Despite the increased costs, the protection remains absolutely essential. While some companies restrict coverage limits or eliminate certain benefits for travelers over a specific age, many reputable providers specialize in senior travel insurance and offer robust, restriction-free policies tailored specifically for older adults.

Are routine prescription medications covered by travel medical policies?

Travel medical insurance specifically covers new, unforeseen medical emergencies rather than routine care or standard maintenance medications. If you simply run out of your daily blood pressure pills or lose them in transit, your travel policy will generally not reimburse the cost of a routine refill. You should always travel with an ample supply of your necessary prescriptions securely packed in your carry-on luggage. However, if a foreign doctor prescribes a completely new medication abroad to treat an unexpected illness or injury, the insurance policy will cover that specific pharmacy expense.

What happens if I forget to buy travel insurance within the waiver window?

If you miss the crucial 14-to-21-day window following your initial trip deposit, you lose the ability to secure a pre-existing condition waiver from most standard providers. You can still purchase travel insurance up until the day before you depart, and it will comprehensively cover new injuries, lost luggage, and entirely unrelated illnesses. However, any medical claim resulting from a pre-existing health condition will face immediate denial. If you missed the window, you might need to seek out specialized, often more expensive policies that specifically cater to pre-existing conditions outside the standard timeline.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply