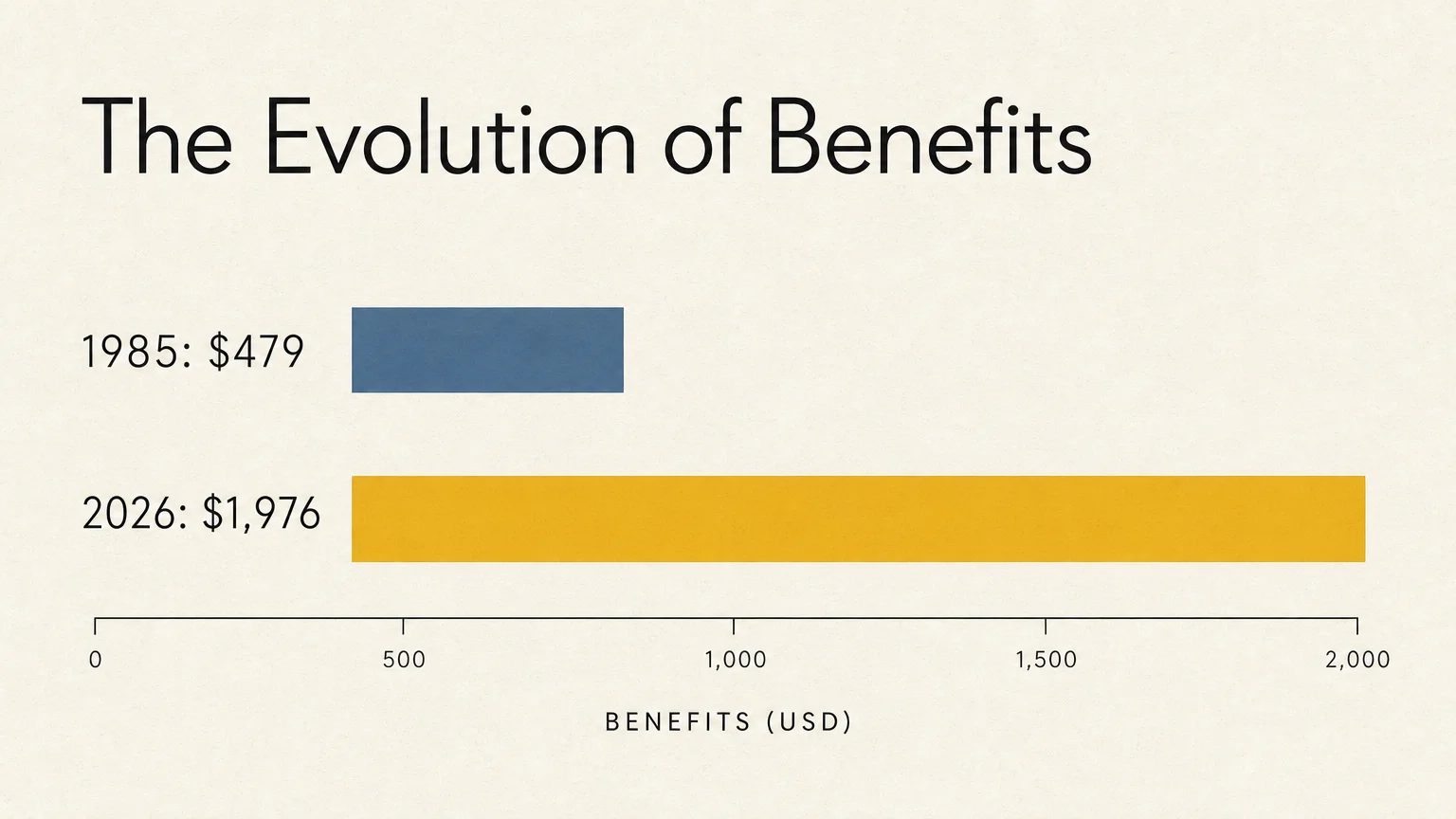

The gap between the $479 average Social Security check of 1985 and the robust $1,976 payment in 2026 illustrates how benefits adapt to protect your purchasing power. Understanding these historical leaps empowers you to make smarter choices about your retirement timeline. You hold the keys to unlocking a higher monthly benefit by mastering the system’s modern rules. While the world has changed dramatically since the mid-eighties, the core promise of financial security remains intact. By leveraging today’s expanded earnings limits, annual cost-of-living adjustments, and strategic claiming ages, you can actively maximize your lifetime income. Let us explore these striking differences and discover practical ways to optimize your financial future.

Tip #1: Embrace the Power of the Cost-of-Living Adjustment (COLA)

Look closely at the numbers, and you quickly realize the sheer impact of inflation over forty years. In 1985, the Social Security Administration distributed an average monthly benefit of just $479 to retired workers. Back then, a gallon of gas cost around a dollar, and rent took a much smaller bite out of the household budget. Today, the economic landscape looks entirely different; thankfully, your benefits have evolved alongside it. Looking at Social Security 2026 data, following a 2.8% Cost-of-Living Adjustment (COLA), that average Social Security payment surged to approximately $1,976 per month.

You can thank the annual COLA for this essential growth. Introduced automatically in 1975, the COLA ensures your buying power does not erode as the cost of groceries, utilities, and healthcare climbs. The government recalculates this adjustment every October using the Consumer Price Index for Urban Wage Earners and Clerical Workers. When inflation rises, your monthly check increases to help bridge the gap. Without this vital feature, a fixed $479 payment would leave modern retirees struggling to pay even a fraction of their monthly bills.

To make the most of this system, actively factor the annual COLA into your financial planning. Instead of guessing your future income, wait for the official October announcement to adjust your household budget for the upcoming year. Use this yearly bump as an opportunity to review your spending habits. Allocate the extra funds toward essential needs like prescriptions or utility bills, ensuring your most critical expenses remain fully funded.

Keep in mind that rising Medicare Part B premiums often absorb a portion of your COLA increase. Because the government automatically deducts Medicare premiums from your Social Security check, a premium hike can take a bite out of your net gain. Review your year-end benefit statements carefully to understand exactly how much extra cash will actually hit your bank account in January. By tracking these numbers, you maintain total control over your monthly cash flow and prevent unexpected budget shortfalls.

Tip #2: Maximize Your Lifetime Earnings for a Bigger Check

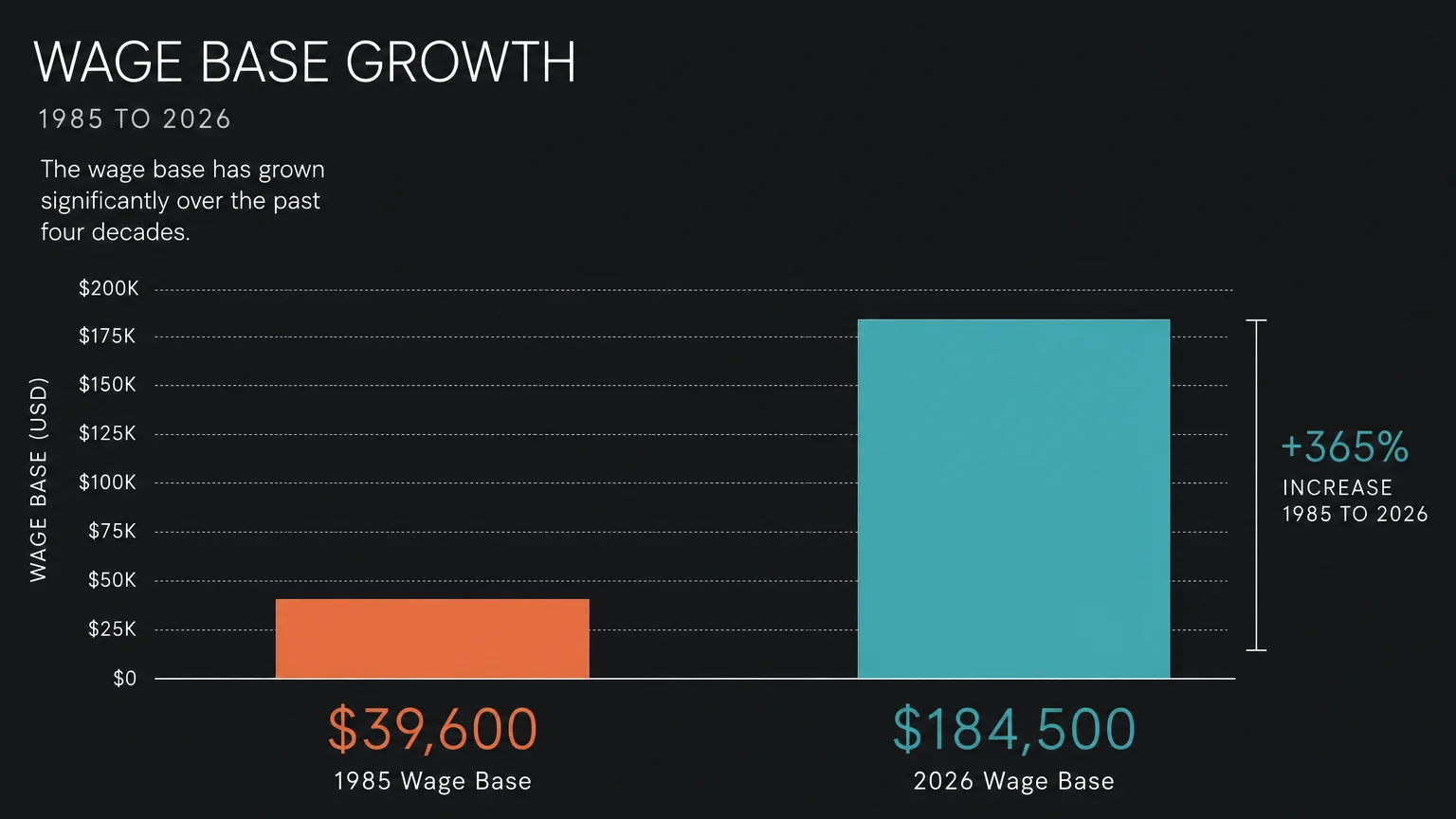

Decades ago, achieving the maximum Social Security benefit required a very different salary trajectory. In 1985, the Social Security taxable wage base—the maximum amount of your income subject to Social Security taxes—sat at $39,600. If you earned above that threshold, you stopped paying into the system for the remainder of the year. Fast forward to 2026, and that wage base has skyrocketed to $184,500. This dramatic shift highlights how wages have grown, but it also reveals a powerful strategy for boosting your own monthly check.

The Social Security Administration calculates your primary insurance amount using your highest 35 years of indexed earnings. If you do not have a full 35-year work history, the government inserts zeros for the missing years. Those zeros drag down your average and permanently shrink your benefit. Conversely, replacing low-earning years with high-earning years actively increases your future payments.

You hold the power to shape this calculation. If you took time away from the workforce to raise children or care for aging parents, consider working a few extra years in your sixties. Even a fun, part-time job or a lucrative side hustle can replace a zero-income year on your permanent record. Every dollar counts toward pushing your average higher.

Furthermore, routinely check your earnings record on the official Social Security website. Mistakes happen; an employer might misreport your income, or a clerical error could cheat you out of valuable credits. Correcting a missing year of income guarantees you receive every penny you deserve. Treat your earnings record like a vital financial document, because it directly dictates the outcome of any future Social Security payment comparison you might run.

Take a proactive approach to your career’s twilight years. Many older adults discover that transitioning into consulting or freelance work offers both mental stimulation and a solid financial payoff. When you continue working, you continue paying into the system, steadily raising your lifetime average. Over time, pushing out those low-earning years from your twenties or thirties yields a surprisingly robust increase in your baseline benefit. Your earning power remains a valuable tool, so use it strategically to maximize your golden years.

Tip #3: Timing Your Claim Matters More Than Ever

When you file for benefits heavily influences the size of your monthly reward. In 1985, the Full Retirement Age (FRA) stood firmly at 65. Most workers confidently claimed their benefits on their 65th birthday without facing any permanent reductions. Today, demographic shifts and longer life expectancies have reshaped the timeline. For anyone born in 1960 or later, the Full Retirement Age is now 67. Claiming earlier than your FRA results in a permanently reduced check, while delaying your claim yields significant financial growth.

You have a distinct advantage if you understand how delayed retirement credits work. If you claim at age 62—the earliest possible age—you might receive roughly 30% less than your full benefit amount. In 2026, an early claim could easily shrink a potential $1,976 check down to around $1,383. However, if you possess the flexibility to wait, the system rewards you handsomely. For every year you delay claiming past your FRA up to age 70, your benefit grows by a guaranteed 8%.

This 8% annual boost stands as one of the most reliable financial returns available. By age 70, you can increase your baseline check by 24%. In fact, the maximum possible Social Security benefit for someone claiming at age 70 in 2026 reaches an astonishing $5,108 per month.

To capitalize on this rule, evaluate your current health, life expectancy, and savings. If you enjoy good health and possess enough retirement savings to cover your early sixties, strongly consider delaying your application. Use withdrawals from your investment accounts to bridge the income gap until you reach age 70. This calculated patience locks in a much larger, inflation-adjusted income stream for the rest of your life.

Even if waiting until 70 feels out of reach, delaying by just one or two years makes a tangible difference. Every month you wait adds a fraction of a percent to your permanent payout. Partner with a trusted financial planner to run a customized breakeven analysis. This reveals the exact age at which your delayed, higher benefits surpass the total amount you would have collected by claiming early. Arm yourself with the math to make the most lucrative choice.

Tip #4: Leverage Spousal and Survivor Benefits

The Social Security system offers incredible protections for married couples, widows, and widowers. When examining Social Security 1985 figures, the average benefit for spouses hovered around $246 per month. While that provided a helpful supplement, modern spousal and survivor benefits deliver a much more substantial lifeline. Today, a non-working spouse can claim up to 50% of the higher-earning spouse’s full benefit amount. If your partner earned a high salary, your spousal benefit alone could easily eclipse the average worker’s check from the 1980s.

To fully optimize your household income, you must coordinate your claiming strategies. If you and your spouse both worked, the Social Security Administration automatically pays out the higher of the two available amounts: your own earned benefit or your spousal benefit. You cannot receive both simultaneously, but the system ensures you receive the maximum single payout you qualify for.

Survivor benefits require even more careful planning. When a spouse passes away, the surviving partner inherits the larger of the two Social Security checks. Because of this rule, the higher earner in a marriage holds a profound responsibility. When the higher earner delays claiming until age 70, they permanently maximize the survivor benefit. If you outlive your spouse, that bolstered check provides immense comfort and stability during a difficult transition.

Open a dialogue with your partner about your long-term goals. Map out your respective ages, earnings histories, and health outlooks. Consider having the lower-earning spouse claim benefits early to provide immediate household liquidity, while the higher earner waits until age 70. This dual approach gives you cash flow today and maximized survivor protection for tomorrow. Navigating the rules together fortifies your marriage against financial uncertainty.

If you are divorced, do not overlook your potential eligibility for ex-spousal benefits. Provided your marriage lasted at least ten years and you remain currently unmarried, you can claim benefits based on your ex-spouse’s earnings record. Doing so does not reduce their payout or the payout of their current spouse. Explore every avenue available to ensure you leave no money on the table.

Tip #5: Supplement Your Check to Build True Golden Years Bliss

While the growth of the average Social Security benefit since 1985 is undeniably striking, you must view this check as just one piece of your financial puzzle. The Social Security Administration explicitly designs benefits to replace roughly 40% of an average worker’s pre-retirement income. In the 1980s, many retirees relied on guaranteed corporate pensions to fill the remaining gap. Today, traditional pensions have largely vanished, placing the responsibility of income generation squarely on your shoulders.

Embrace this shift as an opportunity to build a diversified, resilient retirement portfolio. To achieve true golden years bliss, you need multiple streams of income working in harmony. Start by maximizing contributions to your 401(k), IRA, or Roth IRA. If you are over age 50, take full advantage of catch-up contributions to rapidly accelerate your wealth accumulation.

Once you transition into retirement, structure your withdrawals strategically. Use your guaranteed Social Security check to cover your absolute baseline expenses, such as housing, utilities, and groceries. Then, rely on your personal investment accounts to fund your lifestyle goals—whether that involves traveling the globe, spoiling your grandchildren, or taking up expensive new hobbies.

Do not shy away from alternative income sources. Many modern seniors invest in dividend-paying stocks, real estate, or fixed annuities to create reliable monthly cash flow. Others launch passion-based small businesses or monetize lifelong skills through consulting. By actively cultivating secondary income streams, you reduce your dependence on government programs and insulate yourself against market volatility. You have the freedom to design a rich, vibrant retirement that extends far beyond the limitations of a single monthly check.

Remember, retirement no longer means a hard stop to productivity. The concept of a phased retirement continues to gain popularity, allowing you to transition slowly by working part-time. This approach not only provides extra income but also offers profound social and mental benefits. Staying engaged with your community and maintaining a sense of purpose directly contributes to your overall happiness. When you combine a healthy Social Security payment with robust personal savings and an active lifestyle, you truly capture the essence of a blissful retirement.

The Takeaway: Living a More Blissful Retirement

Reflecting on the evolution of your Social Security check from 1985 to 2026 reveals a system that continuously adapts to support older adults. The striking difference between a $479 payment and a nearly $2,000 monthly benefit demonstrates the powerful, protective nature of the cost-of-living adjustment. However, these adjustments only tell part of the story. Your ultimate financial success depends entirely on how actively you engage with the rules today.

You possess the knowledge and the tools to take charge of your future. By maximizing your earning years, strategically timing your claim, and coordinating with your spouse, you actively shape a more prosperous reality. Couple these tactics with a solid foundation of personal savings, and you build an unbreakable safety net.

Retirement marks a beautiful, expansive new chapter in your life. It offers the freedom to pursue your passions, nurture your relationships, and savor the quiet moments of joy you have rightfully earned. Approach this transition with confidence and optimism. With careful planning and a proactive mindset, you will navigate the complexities of modern retirement seamlessly, unlocking the financial peace of mind necessary to truly enjoy your golden years.

Frequently Asked Questions

What is the maximum possible Social Security benefit in 2026?

For a worker who retires at full retirement age in 2026, the maximum monthly benefit exceeds $3,800. However, if you consistently earn at or above the maximum taxable wage base for 35 years and delay claiming your benefits until age 70, your maximum payment can soar to an impressive $5,108 per month. Achieving this requires decades of high earnings and strategic patience.

How does the 2026 COLA compare to previous years?

The 2.8% Cost-of-Living Adjustment for 2026 represents a moderate, stabilizing increase following the higher, inflation-driven spikes of the early 2020s. While it may seem smaller than the historic 8.7% bump seen in 2023, a 2.8% increase effectively keeps pace with current economic conditions. It adds a meaningful boost to your average Social Security benefit, helping you manage everyday expenses securely.

Can I work while collecting Social Security in 2026?

Yes, you can absolutely work while receiving benefits! If you have reached your Full Retirement Age, you can earn an unlimited amount of money without facing any reductions to your Social Security check. If you claim benefits before your FRA and continue working, the Social Security Administration will temporarily withhold a portion of your benefits if your earnings exceed a specific annual limit. Fortunately, they return those withheld funds to you in the form of a higher check once you reach your FRA.

Are Social Security benefits taxable?

Yes, a portion of your benefits may be subject to federal income taxes, depending on your combined income. If you file a joint return and your combined income falls between $32,000 and $44,000, you may have to pay income tax on up to 50% of your benefits. If your combined income exceeds $44,000, up to 85% of your benefits may be taxable. Proactive tax planning—such as utilizing Roth IRAs or managing your withdrawal rates—can help you minimize this tax burden. Always consult with a certified tax professional to map out a tax-efficient retirement strategy.

What happens if I change my mind after claiming benefits early?

The Social Security Administration offers a one-time opportunity to undo your claiming decision. If you file for benefits but realize within 12 months that you made a mistake, you can withdraw your application. To do so, you must repay all the money you and your family received based on your application. Once you repay those funds, your record resets entirely. You can then delay your claim to a later date, allowing your future checks to grow and locking in a much higher permanent benefit amount.

Will Social Security run out of money before I retire?

You do not need to panic about the system going bankrupt. While the Social Security trust funds face projected shortfalls in the mid-2030s, the program operates on a pay-as-you-go basis. Current workers continually fund the system through payroll taxes. Even if Congress takes no legislative action, the ongoing tax revenue would still cover approximately 80% of promised benefits. Rest assured, lawmakers have numerous tools—such as adjusting the retirement age or raising the taxable wage cap—to shore up the program long before any cuts occur.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply