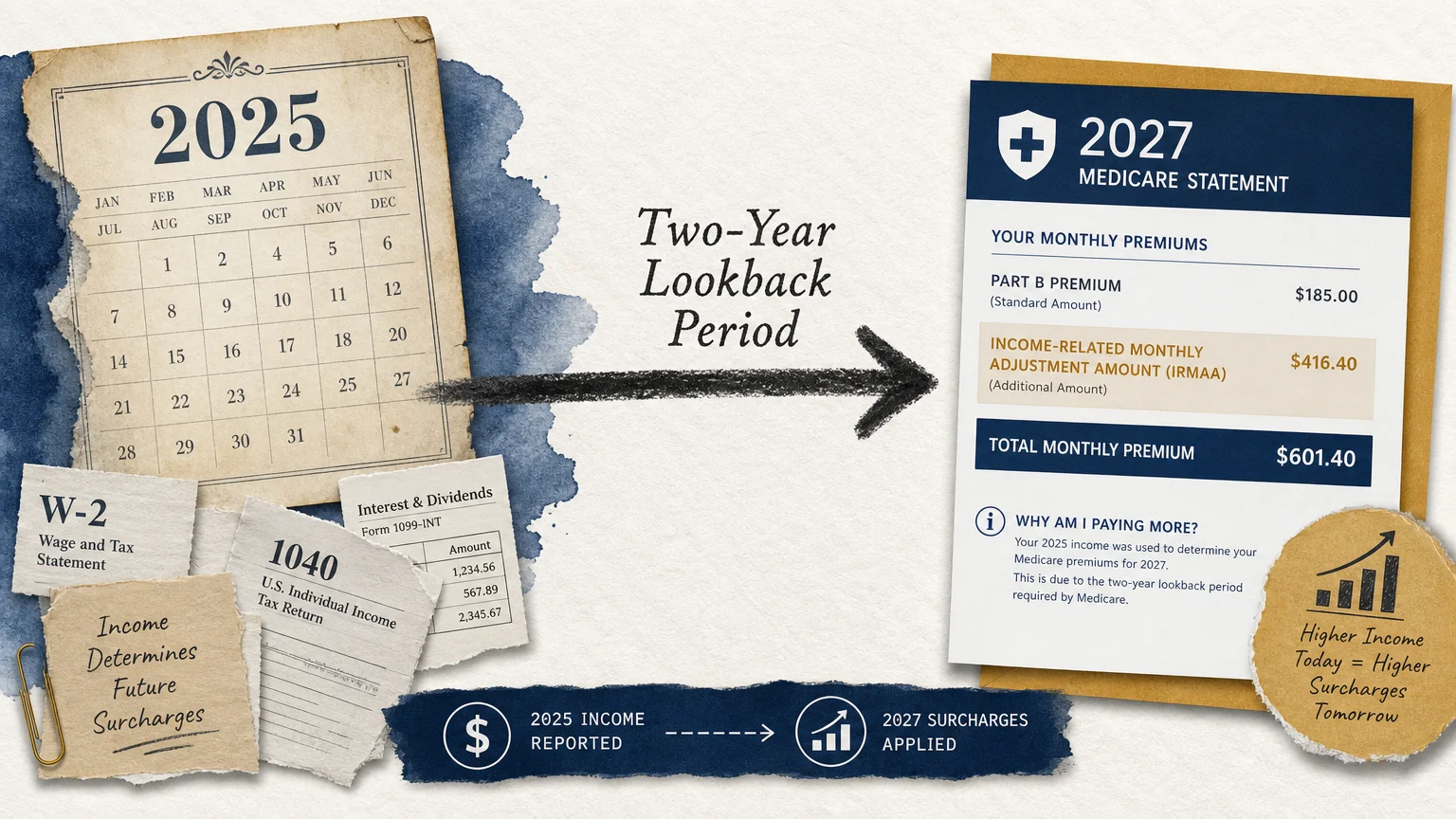

Planning your retirement finances requires looking ahead so you can maximize your lifestyle and minimize unexpected expenses like the 2027 Medicare IRMAA. Because the Social Security Administration uses a two-year lookback period, your 2025 income directly determines the Medicare Part B and Part D surcharges you will face in 2027. By understanding these anticipated brackets now, you gain the power to make strategic tax moves that protect your hard-earned savings. Grasping the estimated 2027 Medicare premiums empowers you to navigate your healthcare costs with absolute confidence; this foresight gives you the peace of mind to focus on enjoying your golden years. Let us explore actionable strategies to help you anticipate and manage your future Medicare expenses seamlessly.

Tip #1: Understand the Mechanics of the Two-Year Lookback Period

Your Medicare costs do not rely on your current year’s income; the government determines your surcharges using a strict two-year lookback period. When you pay your monthly premiums in 2027, the Social Security Administration evaluates the income you reported on your 2025 tax return. This mechanism means the financial decisions you execute today carry direct consequences for your future healthcare expenses. Understanding this delayed timeline gives you a tremendous strategic advantage. You possess the opportunity right now to structure your 2025 income in clever ways that minimize or entirely eliminate your future surcharges.

The calculation relies specifically on your Modified Adjusted Gross Income, commonly referred to as MAGI. For Medicare purposes, your MAGI includes your standard adjusted gross income plus any tax-exempt interest you earn from investments like municipal bonds. Many retirees accidentally trigger massive surcharges by executing large financial transactions without considering this specific calculation. Selling a highly appreciated piece of real estate, executing a massive Roth IRA conversion, or cashing out an inherited stock portfolio will dramatically spike your 2025 MAGI.

This temporary income bump inevitably forces you into higher 2027 IRMAA brackets. You can maintain complete control over your healthcare costs by simply collaborating with your financial planner before finalizing any substantial withdrawals this year. Keeping your income safely below the government’s designated thresholds ensures you keep more of your hard-earned money in your own pocket rather than sending it back to the Medicare system. Mastering this timeline represents the fundamental first step in protecting your retirement budget.

Tip #2: Anticipate the Estimated 2027 IRMAA Brackets

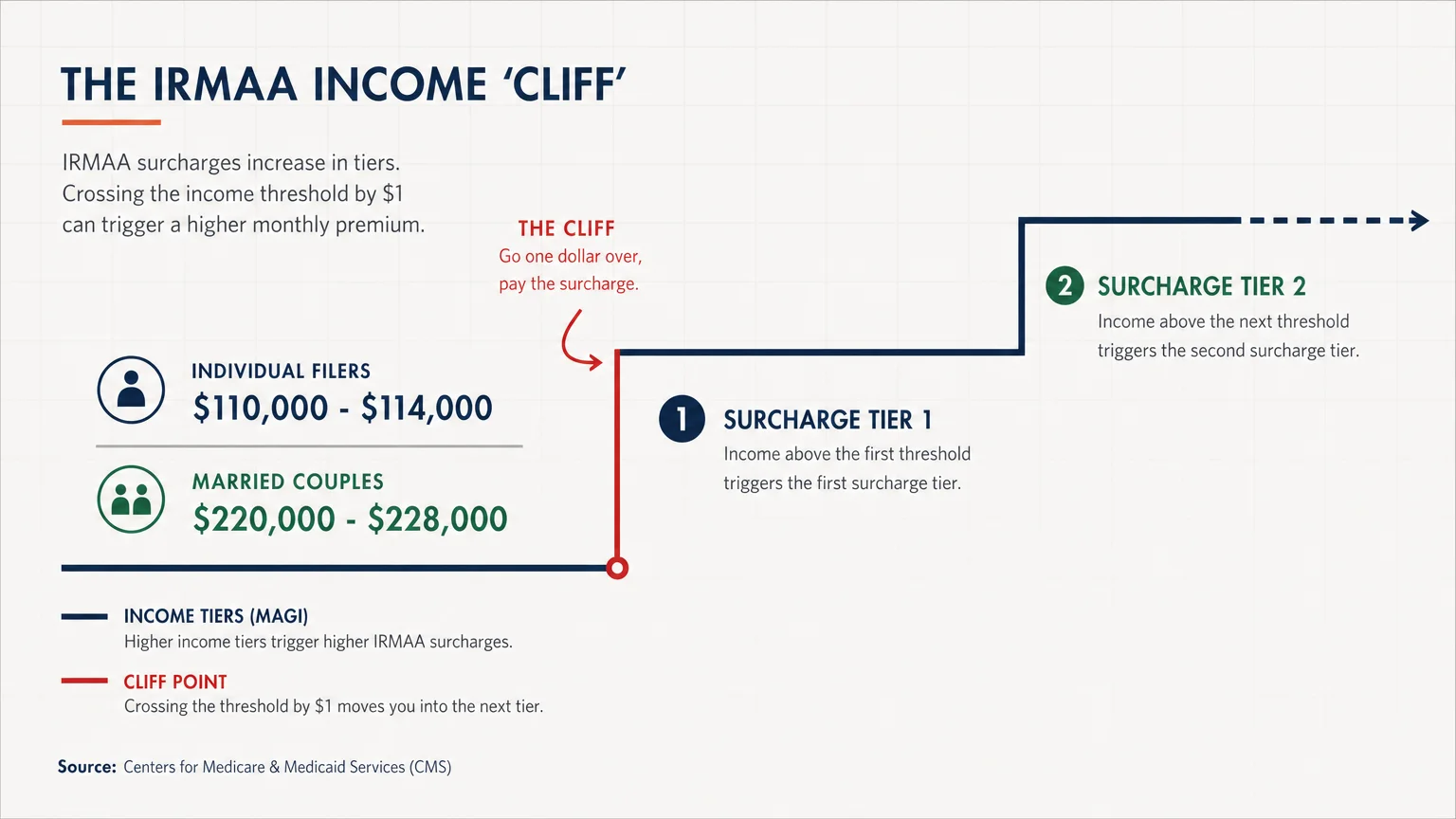

The official government agencies release the exact income brackets late in the preceding year, but you can forecast the 2027 Medicare IRMAA today by analyzing current inflation trends. Medicare adjusts these income thresholds annually using the Consumer Price Index; this vital adjustment protects retirees from being penalized purely by standard economic inflation. For your 2025 financial planning, you must proactively project where these dividing lines will fall. Financial experts anticipate that the lowest threshold for single filers will likely sit around $110,000 to $114,000, while married couples filing jointly could see their baseline shift to approximately $220,000 to $228,000.

Earning even one single dollar over these specific boundaries pushes you instantly into the first surcharge tier. The system does not phase in gently; it operates on a rigid cliff mechanism. Each subsequent tier utilizes a stair-step model, meaning that as your income climbs higher, your monthly surcharge increases significantly. For instance, experts project the second tier might begin around $140,000 for individual filers and $280,000 for married couples. The highest tier typically impacts single filers earning over $500,000 and couples earning over $750,000.

You must aim to land your 2025 MAGI securely within the lower boundaries to avoid these escalating penalties. Forecasting these 2027 IRMAA brackets empowers you to optimize your asset withdrawals throughout the current year. You can safely pull funds from traditional taxable accounts up to the predicted limits, then strategically switch to tax-free sources like a Roth IRA or a cash reserve to cover the remainder of your living expenses. Planning with these estimated numbers ensures you never face sudden, unexpected financial penalties when your official determination letter arrives two years down the road.

Tip #3: Calculate Your Projected Medicare Part B IRMAA

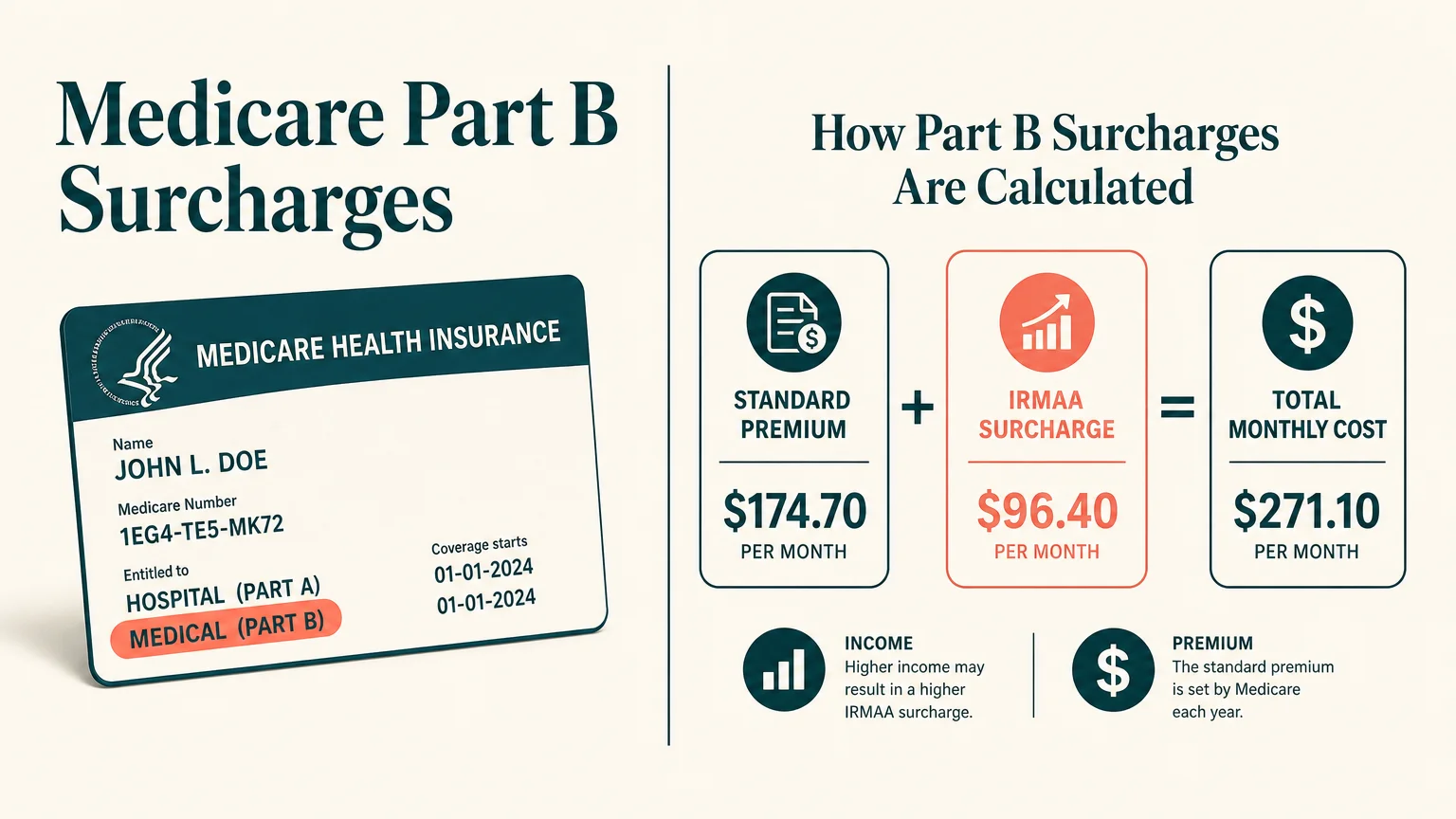

Medicare Part B covers your crucial outpatient services, physician visits, lab tests, and durable medical equipment. Every enrolled retiree pays a standard monthly premium, which actuaries project will climb steadily to keep pace with modern healthcare costs; however, high earners pay the standard premium plus the Medicare Part B IRMAA. This surcharge acts as an extra layer of cost added directly to your monthly bill. The Social Security Administration typically deducts this total combined amount straight from your monthly Social Security check before the funds ever hit your personal bank account.

If your 2025 income pushes you into the first surcharge tier, you might expect an additional monthly fee ranging from $70 to $90 per person. For a married couple, this translates to hundreds of dollars in extra yearly expenses stripped directly from your benefits. In the highest income brackets, retirees sometimes face monthly surcharges exceeding $400 per person, pushing their total Part B premium well past the $600 mark. Anticipating your 2027 Medicare premiums requires multiplying these monthly fees over the entire twelve-month calendar year to understand the full annual impact.

By realizing the true annual cost of these surcharges, you quickly see how a small, seemingly harmless bump in your taxable income creates an outsized financial penalty. A $500 capital gain could trigger a $2,000 annual surcharge for a married couple. You can protect your retirement budget by staying incredibly vigilant about your capital gains, dividends, and taxable distributions. Structuring your income correctly ensures your Social Security check remains as large and beneficial as possible, providing you with the maximum amount of cash flow for your daily lifestyle.

Tip #4: Navigate Your Anticipated Medicare Part D IRMAA

Your prescription drug coverage carries its own entirely separate surcharge structure. Just like Part B, your Medicare Part D IRMAA is directly tied to your 2025 MAGI. Private insurance companies administer Part D plans, meaning your base premium varies wildly depending on the specific policy and coverage level you select during open enrollment; however, the government mandates the surcharge itself. You pay this extra surcharge amount directly to Medicare, not to your private insurance provider.

Recent legislative changes, most notably the Inflation Reduction Act, introduced wonderful benefits like the $2,000 annual cap on out-of-pocket prescription drug costs. This landmark legislation provides immense relief for retirees requiring expensive maintenance medications. However, you must understand that this $2,000 cap applies strictly to your medication purchases at the pharmacy counter. It does not limit, offset, or prevent the Part D premium surcharge in any way. If you fall into a higher income tier, you could see an extra $15 to $85 added to your monthly costs, regardless of whether you ever actually fill a prescription during the year.

Analyzing your estimated 2027 Medicare premiums means adding your Part B standard premium, your Part B surcharge, your Part D private plan premium, and your Part D surcharge together. You can accurately map out your holistic healthcare budget only when you view these four distinct components as a single, interconnected ecosystem. Grasping this complete picture gives you the absolute clarity to make confident, proactive financial choices regarding your drug coverage and overall health spending.

Tip #5: Implement Tax-Efficient Income Strategies Today

Because your 2025 income dictates your future premiums, implementing tax-efficient strategies right now serves as your absolute best defense. One of the most powerful and accessible tools at your disposal is the Qualified Charitable Distribution. If you are aged 70 and a half or older, the IRS allows you to transfer funds directly from your Traditional IRA to an eligible charity. This direct distribution counts toward fulfilling your Required Minimum Distribution, yet it completely bypasses your taxable income. Utilizing this generous strategy keeps your MAGI substantially lower, simultaneously supporting a cause you love and fiercely protecting your 2027 IRMAA brackets.

You should also practice strategic capital gains management throughout the year. When you rebalance your investment portfolio to maintain your desired risk level, you inevitably trigger taxable events. You can neutralize these newly realized gains through a process known as tax-loss harvesting; this sophisticated maneuver involves actively selling underperforming assets at a loss to cleanly offset the profits generated by your winners. This effectively reduces your overall MAGI without diminishing your actual spending power. You essentially clean up your investment portfolio while actively defending against future Medicare surcharges.

Furthermore, you must carefully time any anticipated Roth IRA conversions. While converting traditional retirement funds into a Roth account provides tremendous long-term tax-free growth advantages, the entire conversion amount gets added directly to your taxable income for the current year. Executing a massive, single-year conversion in 2025 will certainly inflate your MAGI and trigger steep penalties two years later. You can achieve far better results by systematically dividing your conversions into smaller, manageable chunks over several consecutive years. This measured approach allows you to fill up your current tax bracket without spilling over into the next punitive surcharge tier. Controlling your taxable footprint today guarantees a significantly more affordable healthcare experience tomorrow.

Tip #6: Prepare to Appeal with Form SSA-44

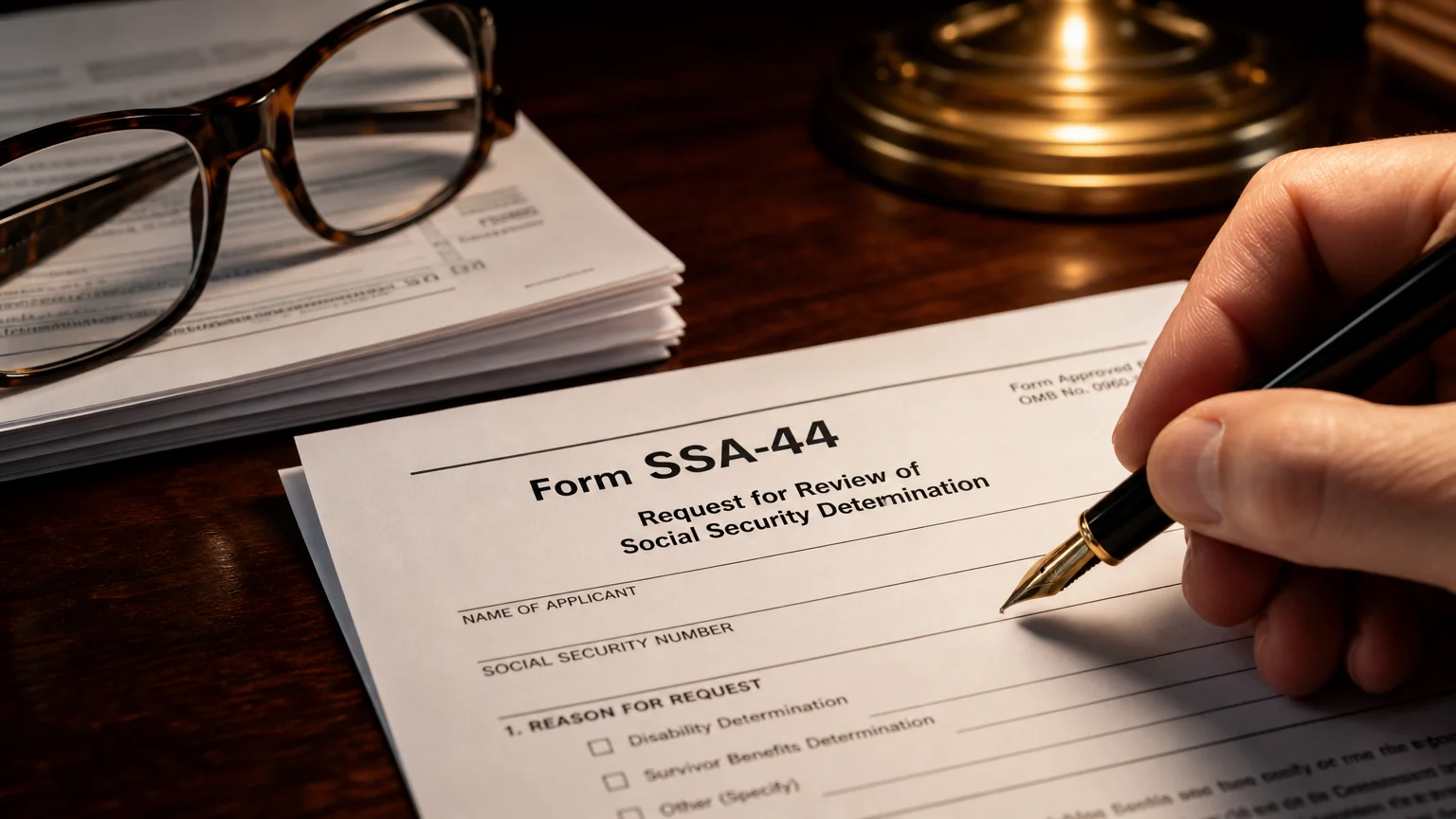

Life rarely follows a perfectly predictable path; you might experience a significant personal transition that drastically reduces your actual income between the 2025 lookback year and the 2027 coverage year. The Social Security Administration provides a clear, highly documented pathway to contest your assigned surcharges if you encounter specific, life-altering events. You do not have to passively accept a massive premium increase if your financial reality has genuinely shifted downward. You can officially request a complete recalculation of your Medicare Part B IRMAA and Part D surcharges by filing Form SSA-44.

The government officially recognizes eight distinct life-changing events that instantly qualify you for a premium reduction. The most common and widely utilized event is retirement itself. If you earned a high executive salary in 2025 but plan to retire completely in 2026, your actual 2027 income will be significantly lower than your lookback year suggests. Other eligible, recognized events include marriage, divorce, the sudden death of a spouse, an involuntary reduction in work hours, the loss of income-producing property due to a natural disaster, or the unexpected loss of a pension.

When you receive your initial premium determination letter late in 2026, you simply submit Form SSA-44 to the administration along with concrete proof of your life-changing event and a realistic estimate of your newly reduced income. Acceptable proof often includes a signed letter from your former employer or a certified marriage certificate. The administration will quickly review your submitted case and update your premium to accurately reflect your current financial truth. Knowing you possess this powerful safety net eliminates the anxiety of facing unjustified fees during major, stressful life transitions.

The Takeaway: Living a More Blissful Retirement

Managing your healthcare expenses requires foresight, diligence, and a deeply positive mindset. You hold the incredible power to shape your financial future simply by understanding how your daily actions today directly influence your fixed costs down the road. By projecting your 2025 MAGI and utilizing tax-smart, proactive strategies, you actively shield your lifelong savings from unnecessary government penalties. Navigating the 2027 Medicare IRMAA does not have to feel confusing or overwhelming; it simply serves as another fantastic opportunity to optimize your wealth and streamline your budget.

Your hard-earned retirement years are meant for grand exploration, abundant joy, and total peace of mind. Keeping your baseline healthcare costs manageable predictably leaves significantly more room in your monthly budget for international travel, engaging hobbies, and beautiful family experiences. You can approach your upcoming financial decisions with absolute clarity and soaring confidence. Embrace the wonderful journey ahead, deeply knowing you are fully equipped and expertly prepared to handle whatever the future brings your way.

Frequently Asked Questions

Will I have to pay the IRMAA surcharge forever once I cross the threshold?

Absolutely not; the Social Security Administration completely recalculates your Medicare premium every single year based on a rolling two-year lookback. If you experience a sudden, isolated spike in your income during 2025 that temporarily pushes you into a surcharge tier, you will only pay the higher premium for the 2027 calendar year. Assuming your income naturally drops back down to normal levels in 2026, your 2028 premiums will automatically return to the standard baseline level. This annual recalculation mechanism ensures your healthcare costs always remain closely aligned with your most recent financial reality.

Do withdrawals from a Roth IRA count toward the MAGI calculation for my Medicare surcharges?

You will be thrilled to know that qualified distributions from a Roth IRA completely bypass your taxable income. Because these withdrawals are entirely tax-free at the federal level, they do not affect your Modified Adjusted Gross Income whatsoever. This unique characteristic makes Roth accounts incredibly valuable tools for managing your daily living expenses without inadvertently triggering future Medicare surcharges. Pulling cash from a Roth account allows you to maintain a luxurious lifestyle while appearing invisible to the IRMAA formula.

When will the government officially notify me about my exact 2027 surcharges?

The government actively sends out initial determination letters toward the very end of 2026, typically arriving in your mailbox in late November or early December. This comprehensive letter clearly outlines your new standard premium, details your specific surcharges based precisely on your 2025 tax return, and outlines the exact process you must follow if you need to file an appeal. Keeping a close eye out for this vital correspondence ensures you remain perfectly prepared for the new financial year.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply