Taking proactive steps today ensures a potential 22% cut to Social Security in 2032 will not derail your peaceful retirement. As the federal trust funds face a projected shortfall in just six years, relying solely on government benefits leaves your financial future vulnerable to automatic legislative reductions. You hold the power to build a resilient financial plan by diversifying your income, reducing fixed expenses, and maximizing the assets you already own. Understanding the current Social Security outlook gives you a distinct strategic advantage, allowing you to implement smart portfolio adjustments well before any changes take effect. Secure your peace of mind and protect your lifestyle by taking actionable, empowering steps toward lasting financial independence right now.

Tip #1: Understand the Real Social Security Outlook

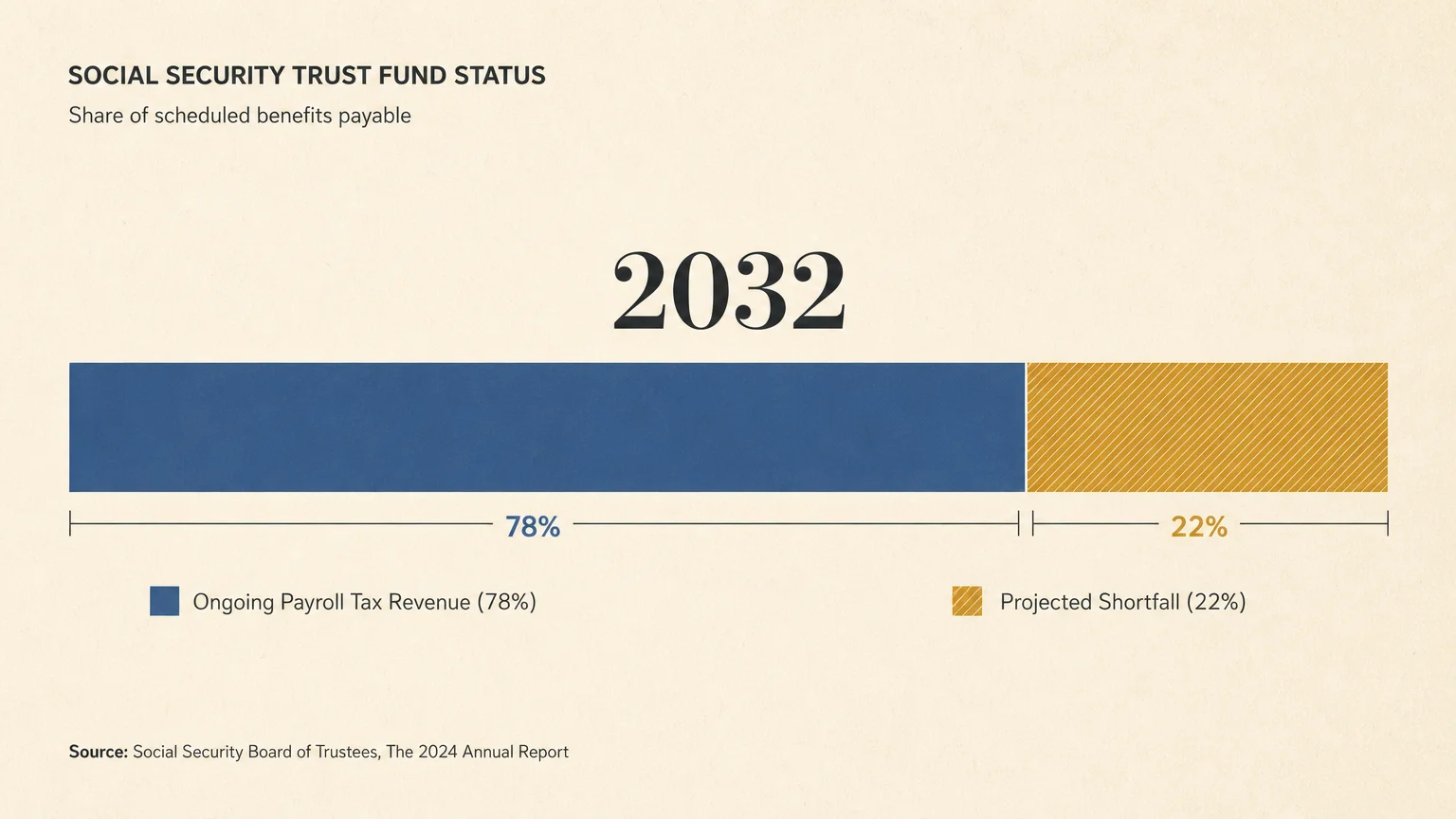

Sensational headlines often paint a catastrophic picture of the future, but understanding the actual math behind the Social Security 2032 projections provides immense relief. The Old-Age and Survivors Insurance Trust Fund is indeed facing a shortfall; however, this certainly does not mean the entire system is going bankrupt. If Congress takes absolutely no legislative action by the 2032 deadline, ongoing payroll tax revenues will still cover approximately 78% of your scheduled benefits.

You can turn this statistical knowledge into a tangible planning tool right now. Navigate to the official Social Security Administration website and download your most recent earnings statement. Look at your projected monthly benefit at your full retirement age, and multiply that figure by 0.78. This simple calculation reveals your baseline worst-case scenario. When you know the exact numbers, the paralyzing fear of the unknown immediately dissipates. You can clearly identify the precise monthly income gap you need to fill over the next six years, making your financial strategy much more targeted, effective, and completely under your control.

Tip #2: Optimize Your Claiming Strategy to Offset Social Security Benefit Cuts

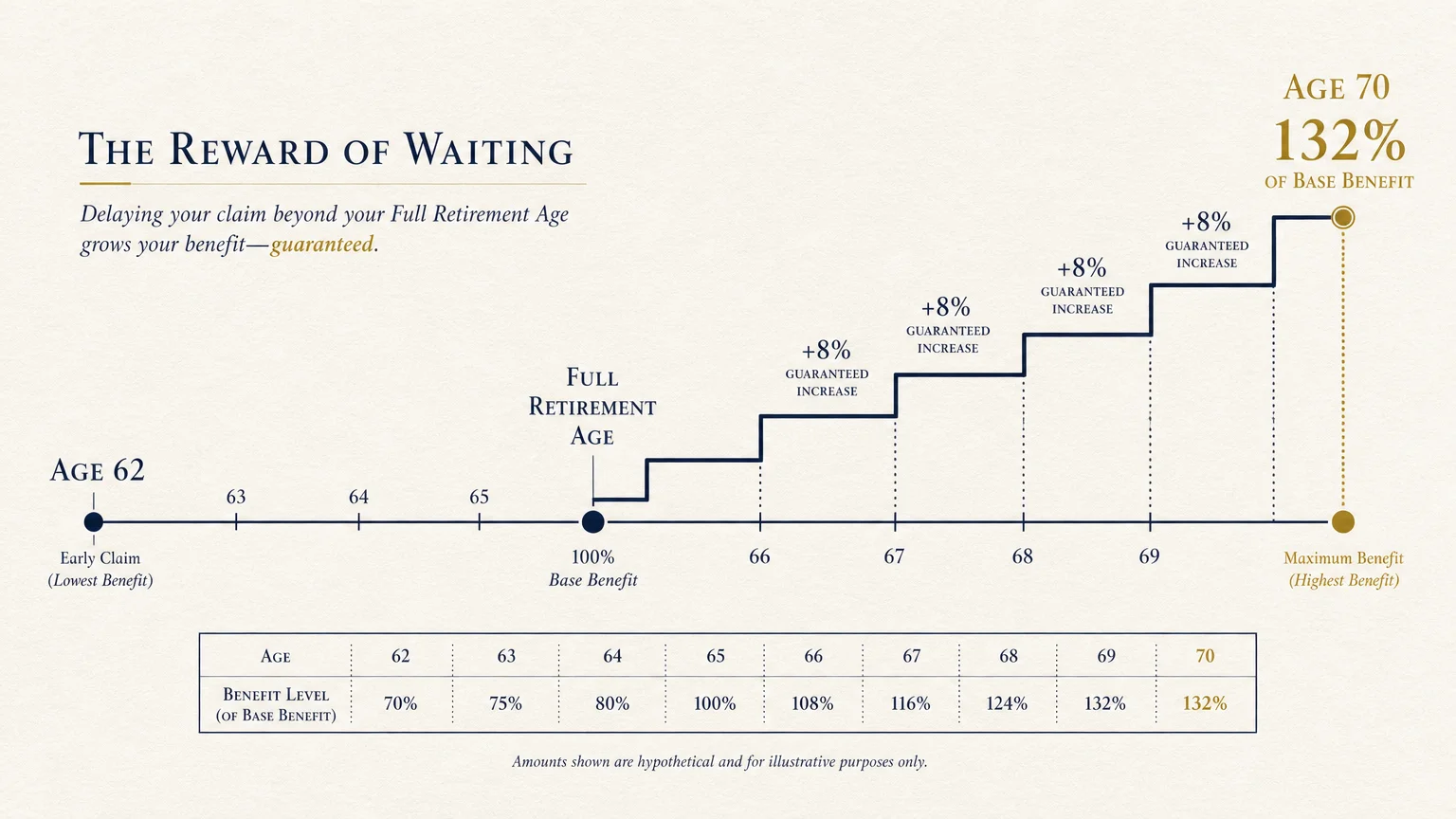

Your claiming age remains one of the most powerful and accessible financial levers you control in retirement. While you hold the right to claim benefits as early as age 62, doing so permanently locks in a severely reduced monthly payout. Conversely, delaying your claim beyond your full retirement age yields a guaranteed 8% annual increase in your benefit amount until you reach age 70.

By intentionally delaying your claim, you artificially inflate your baseline benefit. If an automatic 22% reduction occurs in six years, taking a cut on a much larger initial sum leaves you with a significantly higher net payout. For example, a benefit that has grown by 24% due to a three-year delayed claiming strategy will weather a 22% reduction far better than a benefit permanently reduced by early filing. Evaluate your personal health, your family longevity history, and your current savings to determine if you can realistically afford to wait. Using your existing investment portfolio to bridge the income gap between age 62 and 70 often proves to be an exceptionally wise investment in your long-term security.

Tip #3: Maximize Your Catch-Up Contributions Now

Because the 2032 deadline is still several years away, you possess a vital window of opportunity to drastically increase your personal savings. The IRS provides highly generous catch-up contribution limits specifically designed for individuals aged 50 and older. Leveraging these elevated limits allows you to pump additional tax-advantaged money into your retirement accounts during what are typically your highest-earning years.

Recent legislative updates from the SECURE 2.0 Act offer even more aggressive savings options tailored for near-retirees. For instance, individuals aged 60 to 63 can now make significantly higher special catch-up contributions to their workplace retirement plans. Directing your surplus income into a 401(k), a 403(b), or an Individual Retirement Account creates a massive private financial fortress. Even if government benefits shrink, a robust personal portfolio guarantees you retain complete authority over your lifestyle. Automate these elevated contributions through your employer’s payroll system so your money grows quietly and consistently in the background without requiring daily management.

Tip #4: Build Sizable Cash Reserves to Protect Retirement Income

Unpredictable market volatility combined with sudden Social Security changes creates a perfect storm for retirees who lack highly liquid assets. Sequence of returns risk—the very real danger of experiencing poor investment returns just as you begin withdrawing funds—can quickly deplete your hard-earned nest egg. You can entirely neutralize this threat by maintaining a robust, highly liquid cash reserve.

Leading financial experts typically recommend keeping one to two years’ worth of baseline living expenses in cash or cash equivalents. Consider utilizing high-yield savings accounts, short-term certificates of deposit, or stable Treasury bills to safely house this money. When you hold adequate cash reserves, you never have to sell your stocks or mutual funds at a loss during a sudden market downturn just to pay for your groceries or medical bills. This intentional liquidity acts as a powerful financial shock absorber; it ensures that even if your government check arrives 22% lighter, your daily life remains completely uninterrupted and perfectly stress-free.

Tip #5: Diversify Your Revenue Streams Away from the Government

Relying heavily on a single source of income violates one of the most fundamental rules of wealth management. Protecting retirement income requires you to actively build multiple, distinct revenue silos. When you successfully diversify your cash flow, shifting political winds in Washington lose their ability to threaten your standard of living.

Take a close look at your current asset allocation and seek out investments that consistently generate reliable passive income. Dividend-paying blue-chip stocks, real estate investment trusts, and strategically laddered bonds offer dependable payouts that operate entirely independently of the Social Security administration. You might also explore fixed annuities to establish a private, guaranteed income floor that securely covers your essential baseline expenses, like housing and utilities. Cultivating three or four separate streams of revenue creates an unshakable financial foundation. If one income stream temporarily dries up or faces reductions, the others continue flowing and keep your golden years beautifully funded.

Tip #6: Strategically Reduce Your Fixed Household Expenses

A dollar saved is often significantly more valuable than a dollar earned, especially when you factor in the erosive impact of income taxes. One of the most highly effective ways to prepare for potential Social Security benefit cuts is to systematically and permanently lower your required monthly overhead. When your baseline living expenses are exceptionally lean, a 22% reduction in benefits feels like a minor inconvenience rather than a full-blown financial crisis.

Evaluate your largest monthly outflow: your housing. Downsizing to a smaller, more manageable home or relocating to a more tax-friendly state frees up massive amounts of locked home equity while simultaneously slashing your property taxes, utility bills, and maintenance costs. If moving is not on the table, focus relentlessly on eliminating all high-interest consumer debt and auto loans before you officially retire. Entering your golden years completely debt-free ensures that every single dollar of your reduced Social Security check goes straight toward your happiness, your health, and your leisure, rather than servicing past obligations.

Tip #7: Optimize Tax-Efficient Withdrawal Strategies

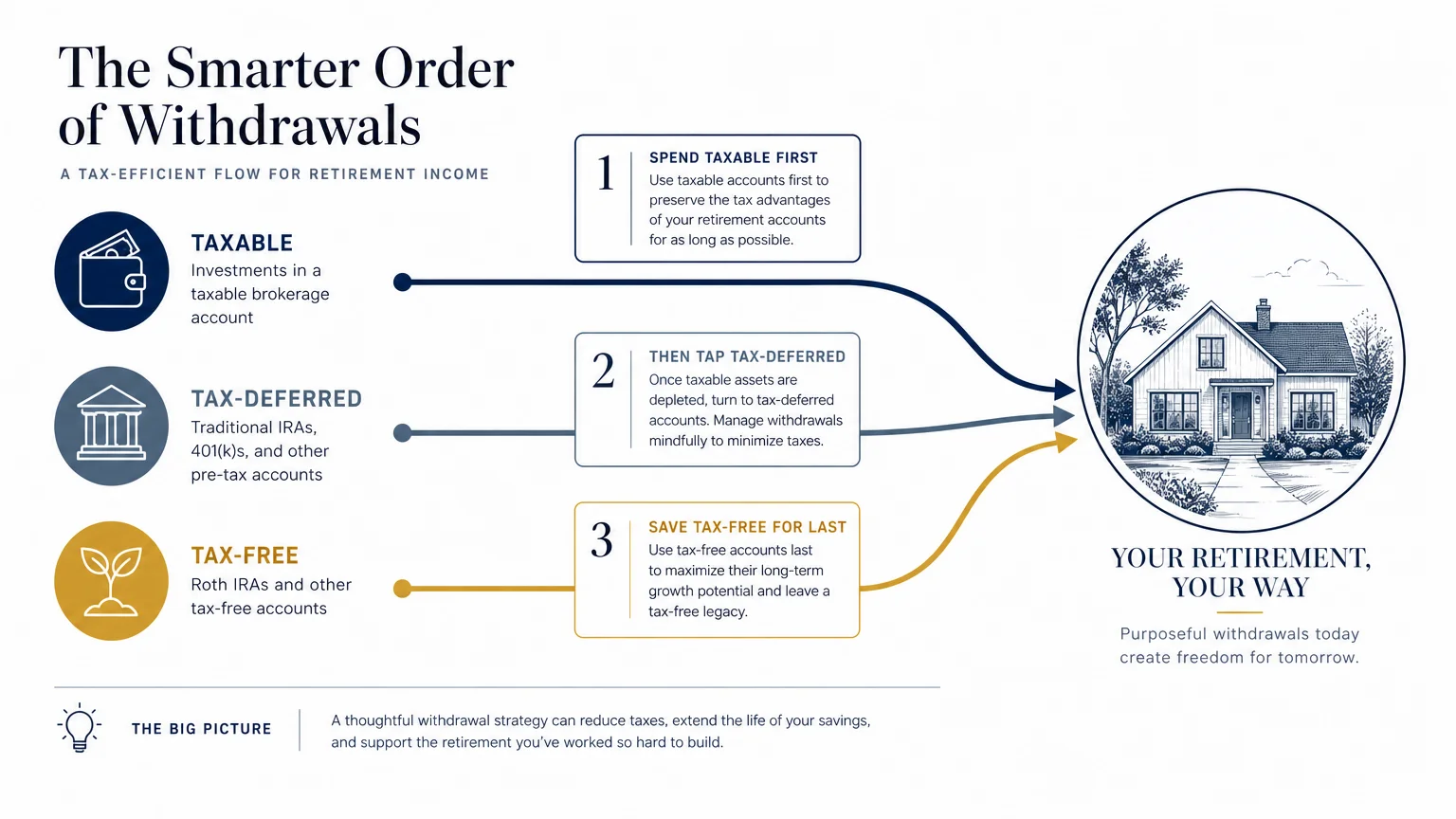

Retirees often lose a significant portion of their wealth to invisible leaks, and taxes represent the absolute largest leak of all. Proper Social Security retirement planning goes far beyond simply saving a pile of money; it involves engineering exactly how and when you pull that money out. The specific way you structure your account withdrawals directly determines how much of your wealth you actually get to keep in your pocket.

Work diligently on balancing your taxable, your tax-deferred, and your tax-free accounts. Executing strategic Roth IRA conversions during calendar years when your income temporarily falls into a lower tax bracket can easily save you thousands in future tax liabilities. Because Social Security benefits are subject to taxation based on your combined provisional income, carefully drawing your living expenses from tax-free Roth accounts can actually keep your taxable income low enough to avoid heavy taxation on your government benefits. A highly optimized, tax-efficient withdrawal strategy stretches your existing portfolio significantly further, effortlessly absorbing the shock of any future benefit reductions.

Tip #8: Consider the Deep Joy of a Phased Retirement

Retirement no longer has to be a rigid hard stop where you completely walk away from the workforce overnight. Many older adults find immense joy, profound purpose, and unmatched financial security by eagerly embracing a phased retirement. Transitioning gently into part-time work, remote consulting, or launching a small passion project allows you to stay mentally sharp while generating highly meaningful active income.

Working just two or three days a week provides enough consistent cash flow to easily cover your basic living expenses, allowing your investment accounts to continue growing untouched. This active income also makes it significantly easier to delay claiming your government benefits until age 70. Beyond the profound financial benefits, continuing to work entirely on your own terms provides vital social interaction and a strong, renewing sense of identity. You can monetize lifelong hobbies, consult casually in your previous industry, or take on a low-stress job in your community simply because you deeply enjoy the environment.

Tip #9: Collaborate With a Fiduciary Financial Expert

Navigating the intricate complexities of Medicare premiums, market volatility, shifting tax brackets, and impending Social Security changes requires highly specialized knowledge. While educating yourself is incredibly empowering and highly recommended, partnering with a credentialed expert ensures you do not accidentally overlook critical details. A fiduciary financial advisor is legally obligated to act strictly in your best interest and can provide highly objective, data-backed guidance.

A skilled fiduciary advisor will run sophisticated Monte Carlo simulations to vigorously stress-test your portfolio against the exact scenario of a 22% benefit cut in 2032. They possess the tools to identify hidden vulnerabilities in your plan and will recommend custom-tailored adjustments to your asset allocation. Treating your retirement like a thriving, well-run business means you should not hesitate to hire a brilliant chief financial officer to guide your strategy. Professional, unbiased guidance replaces nagging anxiety with unshakeable confidence, allowing you to focus entirely on thoroughly enjoying your hard-earned freedom.

The Takeaway: Living a More Blissful Retirement

The possibility of a 22% reduction in government benefits in six short years might initially sound intimidating, but it is an entirely manageable hurdle when you eagerly embrace a proactive, empowered mindset. You possess the time, the intelligent tools, and the ultimate capability to adjust your financial trajectory right now. By aggressively increasing your personal savings, intentionally delaying your claiming age, creatively diversifying your revenue streams, and permanently lowering your fixed overhead, you actively build an impenetrable financial shield around your wealth.

Your golden years should be characterized by deep peace, exciting adventure, and boundless joy, not overshadowed by political gridlock or unpredictable, shifting government policies. Use this projected 2032 deadline not as a source of fear, but as a highly powerful catalyst to optimize every single facet of your financial life today. When you confidently take complete ownership of your retirement income, you guarantee that your future remains exceptionally bright, deeply secure, and wonderfully blissful, regardless of what ultimately happens in Washington.

Frequently Asked Questions

Will I lose my entire Social Security check in 2032?

Absolutely not. The heavily discussed projected depletion of the Old-Age and Survivors Insurance Trust Fund only affects the program’s surplus reserves. The Social Security program is continuously funded by an ongoing payroll tax collected from current workers. If Congress takes zero corrective action by 2032, incoming tax revenues will still be sufficient to comfortably pay roughly 78% of your promised monthly benefits. The system is definitely not going bankrupt; it is simply facing a structural revenue shortfall that limits maximum payouts.

How can I accurately estimate my future benefits if cuts happen?

You can effortlessly find your most accurate projections by creating a free, secure account on the official Social Security Administration website. Once you download your current earnings statement, locate the estimated monthly benefit for your desired retirement age. Multiply that specific number by 0.78. This very simple math provides a highly realistic, conservative estimate of your monthly income if the automatic 22% reduction eventually takes effect.

Will Congress step in to prevent these Social Security changes?

Historically, Congress has always successfully intervened to protect this critical government program before a major crisis occurs. In 1983, very similar financial shortfalls were effectively addressed through bipartisan legislation that gradually increased the full retirement age and slightly adjusted payroll taxes. While we cannot accurately predict the exact legislative fix for 2032, lawmakers currently have several highly viable options at their disposal, including raising the earnings cap subject to payroll taxes, increasing the overall tax rate, or further adjusting the full retirement age for younger generations.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply