Maximizing your retirement income requires understanding one specific regulation that catches countless older adults off guard: the Retirement Earnings Test. If you claim your Social Security benefits before reaching your full retirement age while continuing to work, the government temporarily withholds a portion of your monthly check once your earnings exceed a strict limit. This unexpected reduction can severely disrupt your retirement planning and leave you scrambling to cover living expenses. Fortunately, mastering this rule empowers you to make strategic decisions about when to claim your hard-earned money. By learning exactly how your continued employment impacts your payout, you can optimize your financial strategy and protect your financial future.

Tip #1: Grasp the Mechanics of the Retirement Earnings Test

Filing for your benefits early often seems like a brilliant strategy to boost your immediate cash flow. Many proactive seniors decide to claim their Social Security benefits at age sixty-two while maintaining a part-time or even full-time job. They envision a comfortable lifestyle funded by dual income streams. However, the Social Security Administration enforces a strict limitation on this approach through the Retirement Earnings Test.

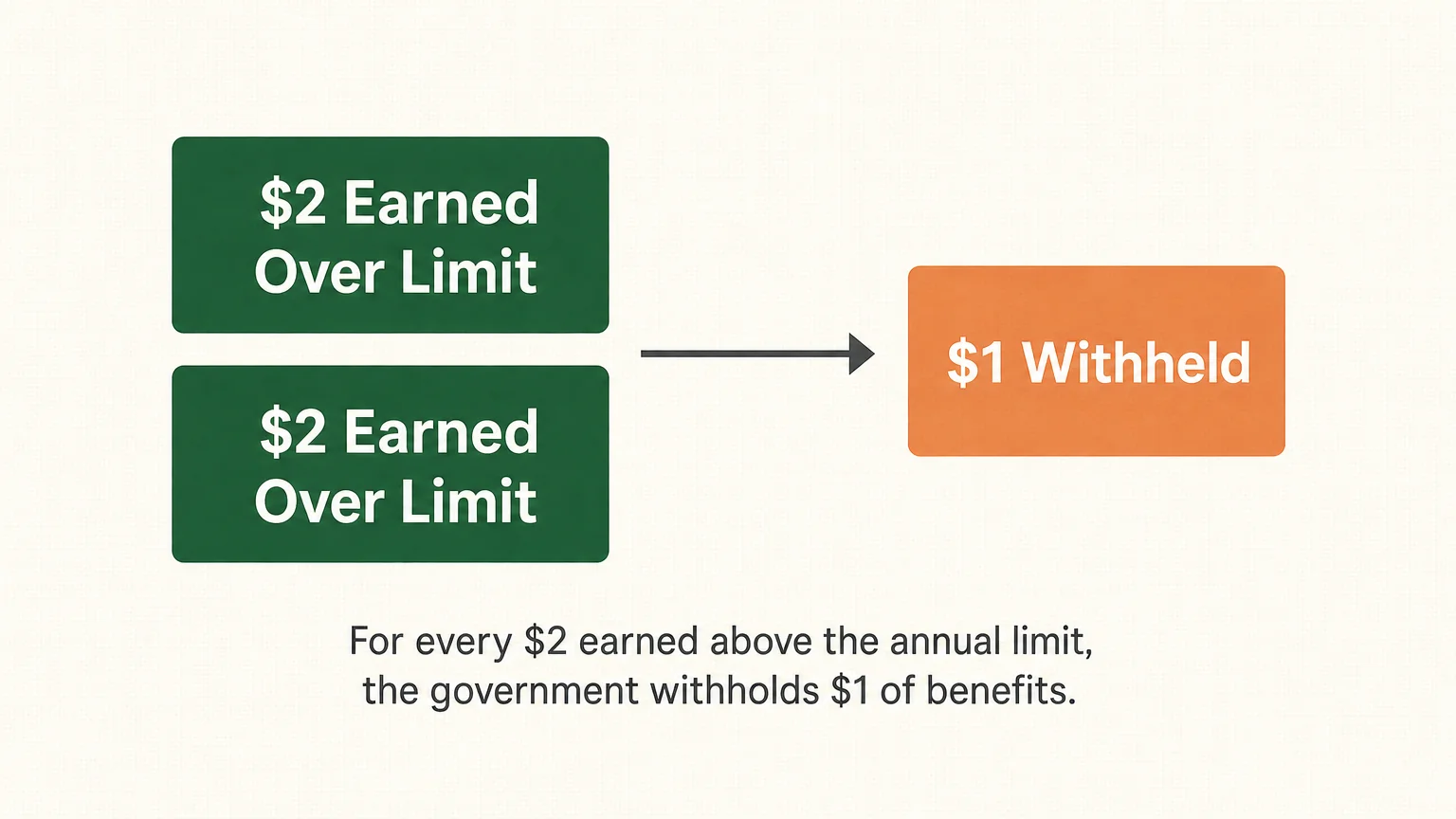

If you have not yet reached your full retirement age, the government applies a specific formula to your earnings. For every two dollars you earn above the annual limit, the Social Security Administration withholds one dollar of your benefits. This drastic reduction routinely shocks retirees who simply wanted to stay active in the workforce while receiving the funds they paid into the system for decades.

Understanding this mathematical reality is crucial for your financial peace of mind. The annual earnings limit adjusts periodically based on national wage growth, meaning you must stay informed about the current threshold. When you earn a significant salary, the government might withhold your checks entirely for several months of the year to satisfy the penalty. You must accurately project your annual wages and compare them against the current earnings limit to prevent an unexpected disruption to your household budget.

The best defense against this surprising reduction is diligent retirement planning. If you plan to continue earning a substantial income, delaying your claim until you reach your full retirement age often provides the most sensible path forward. Taking control of this timeline ensures you receive the maximum possible value from your lifetime of hard work.

Tip #2: Navigate the Special Rule for Your Full Retirement Age Year

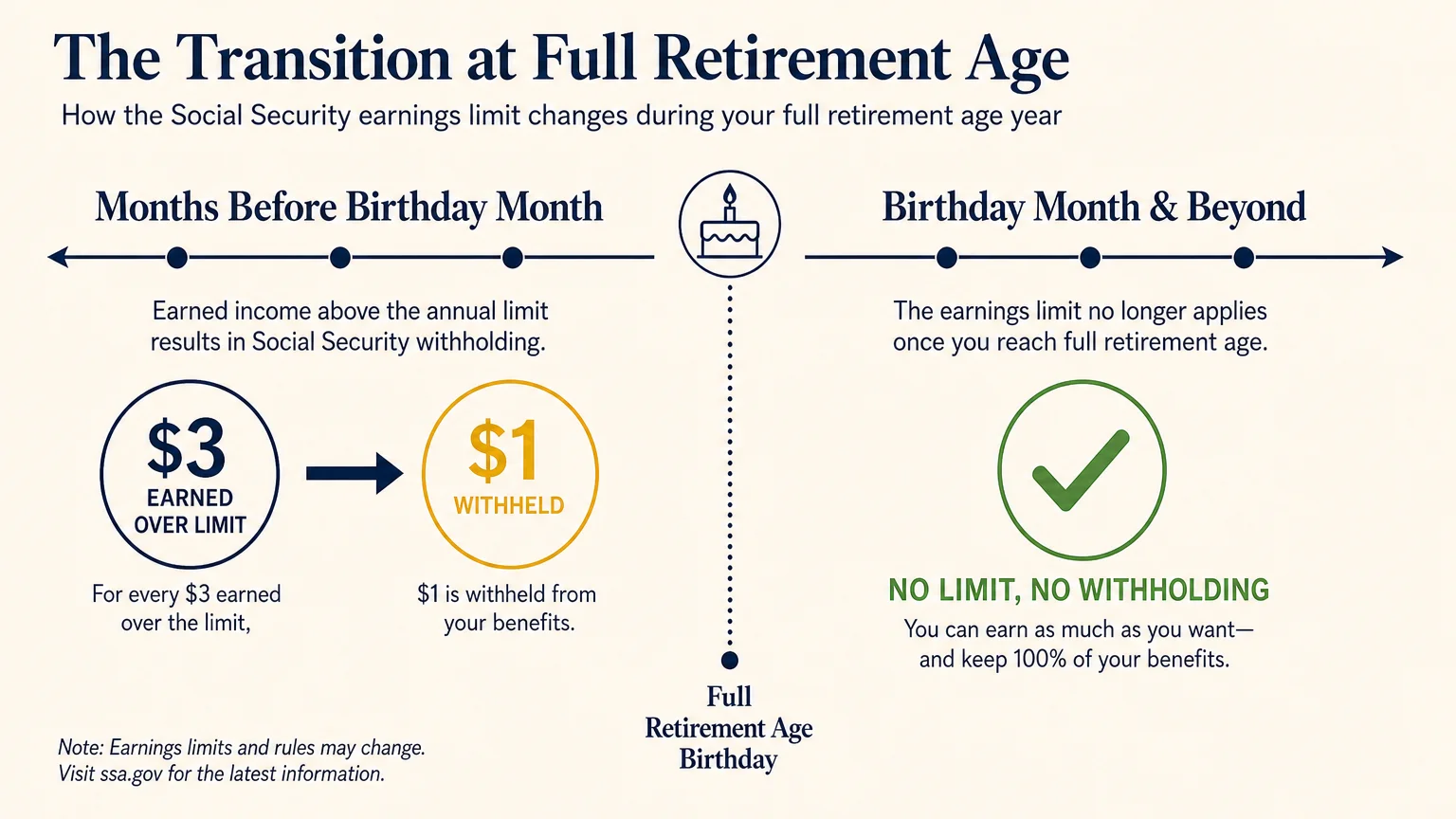

The Retirement Earnings Test features a secondary, highly nuanced rule that applies exclusively during the calendar year you reach your full retirement age. The government recognizes that you are transitioning into full eligibility, so they offer a much more generous financial cushion during this specific window of time.

In the year you hit your full retirement age milestone, the annual earnings limit jumps significantly higher than the standard threshold. Furthermore, the withholding penalty becomes far less punitive. Instead of withholding one dollar for every two dollars you earn over the limit, the Social Security Administration only withholds one dollar for every three dollars you earn above this elevated cap.

You also benefit from a vital timing distinction during this transitional year. The government only counts the wages you earn in the months prior to your birthday month. Once you officially reach the month of your full retirement age, your earnings no longer trigger any reductions whatsoever—no matter how high your salary climbs.

You can leverage this special provision to safely increase your work hours or take on lucrative consulting projects without fearing a massive benefit reduction. By timing your workflow strategically, you can maximize your employment income and smoothly cross the threshold into unrestricted Social Security benefits.

Tip #3: Realize Your Withheld Benefits Are Never Truly Lost

When older adults first encounter the Retirement Earnings Test, they often experience immense frustration. Watching the government withhold hundreds or even thousands of dollars from your Social Security checks feels like a permanent financial loss. Thankfully, one of the most uplifting aspects of Social Security rules is that this money is not actually gone forever.

The funds withheld due to the earnings limit act more like a mandatory deferral than a permanent tax. When you finally reach your full retirement age, the Social Security Administration automatically recalculates your monthly benefit amount. They adjust your payout to account for the exact number of months they withheld your checks.

Consider this practical example: if you claimed your benefits three years early but lost an entire year’s worth of checks to the earnings test, the government treats you as if you only claimed two years early. This favorable recalculation permanently increases your monthly check for the rest of your life.

Understanding this recalculation provides immense psychological relief. You can continue working with the comforting knowledge that your withheld funds will eventually flow back to you in the form of higher monthly payments. This built-in mechanism ultimately rewards your continued labor and strengthens your long-term retirement income strategy.

Tip #4: Calculate What Actually Counts as Earned Income

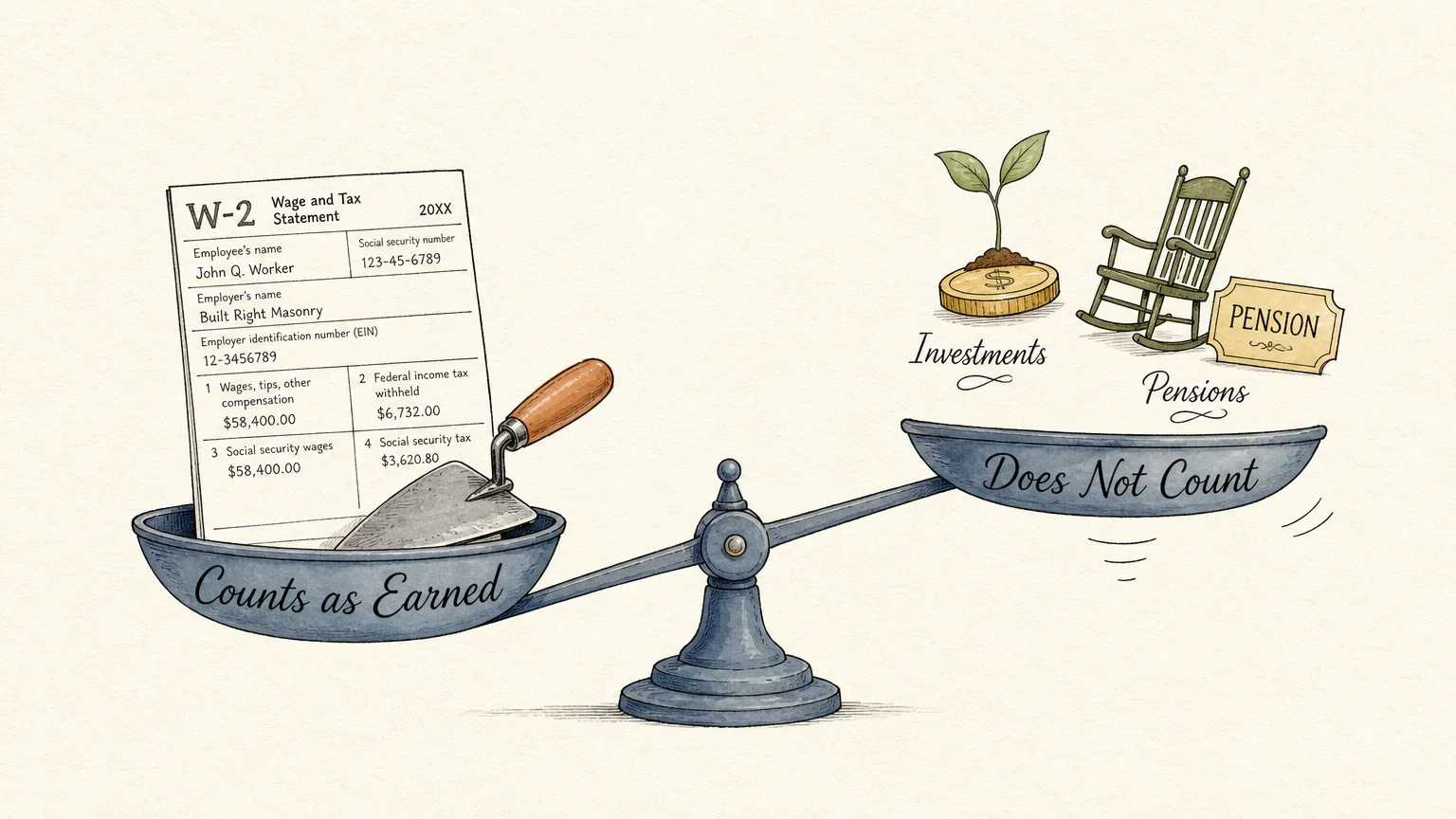

A widespread misconception about the Retirement Earnings Test involves what the government actually considers “income.” Many seniors needlessly panic, assuming that their savings, investments, or pension payouts will trigger benefit reductions. Knowing the exact definition of earned income will help you design a resilient financial plan.

The Social Security Administration strictly looks at earned wages from an employer or net earnings from self-employment. If you receive a standard W-2 form or file a Schedule C for your small business, those specific earnings count directly toward the annual limit. Bonuses, commissions, and vacation pay also fall into the category of earned income.

Conversely, unearned income remains entirely safe from the earnings test. The government ignores your standard pensions, withdrawals from your 401(k) or IRA accounts, traditional annuity payments, and capital gains. Furthermore, your rental property income, stock dividends, and bank interest will never cause the Social Security Administration to withhold your monthly checks.

You can establish passive income streams with total confidence. Renting out a spare property or drawing down your investment portfolio allows you to generate substantial cash flow while keeping your Social Security benefits perfectly intact. Separating your earned wages from your passive wealth is a cornerstone of intelligent retirement planning.

Tip #5: Protect Your Spousal Benefits from the Earnings Test

The reach of the Retirement Earnings Test extends beyond your personal checking account. If you provide derivative benefits to your family members, your decision to work while claiming early can unintentionally impact their financial stability. This ripple effect surprises countless couples every single year.

When the government withholds your monthly benefit because your wages exceeded the earnings limit, they simultaneously withhold any benefits paid to others based on your employment record. If your spouse relies on a spousal benefit tied to your work history, their check will suffer the exact same proportional reduction as yours.

This rule requires careful household coordination. If you plan to work heavily before reaching your full retirement age, you must communicate this strategy with your spouse. An unexpected drop in both of your monthly checks can derail your shared financial goals and create unnecessary stress during your golden years.

However, the reverse scenario offers a layer of protection. If your spouse works and exceeds the earnings limit, their wages will not reduce your standard retirement benefit based on your own independent work record. You must map out these intricate family dynamics to ensure your combined retirement income remains secure and predictable.

Tip #6: Prepare for Taxes on Your Remaining Social Security Benefits

Navigating the earnings limit successfully represents only one hurdle in the complex landscape of retirement finance. Even if your salary stays below the threshold and you receive your full monthly check, you might encounter another surprising rule: the taxation of your Social Security benefits.

The Internal Revenue Service utilizes a formula called “combined income” to determine if your benefits are taxable. You calculate this figure by taking your adjusted gross income, adding any nontaxable interest you receive, and then adding exactly half of your total Social Security benefits for the year. If this final number exceeds certain base amounts, a portion of your benefits becomes subject to federal income tax.

Depending on your total combined income, up to eighty-five percent of your Social Security benefits could face taxation. Because the base thresholds for this tax rule have not been updated for inflation in decades, an increasing number of middle-class retirees find themselves paying federal taxes on their benefits each year.

You must factor this potential tax burden into your withdrawal strategy. Consulting with a tax professional allows you to manage your required minimum distributions and other taxable income sources effectively. By controlling your combined income carefully, you can minimize the taxes levied on your Social Security checks and preserve your overall wealth.

Tip #7: Review Your Annual Social Security Update to Stay on Track

The rules governing your retirement benefits evolve constantly. Inflation adjustments, changing wage indexes, and shifting policy details require you to remain vigilant and adaptable. Relying on outdated information can lead to costly mistakes and missed financial opportunities.

You should prioritize reading your official Social Security update every single year. By creating a secure online account directly through the Social Security Administration, you gain instant access to your personalized statements. These documents highlight your estimated future benefits, verify your recorded earnings history, and outline the specific age at which you reach full retirement.

Monitoring your annual cost-of-living adjustment provides another vital layer of preparation. When the government increases your monthly payout to combat inflation, this extra money can subtly change your tax bracket or your reliance on outside income. Staying informed about these numerical shifts allows you to tweak your budget proactively.

Embrace the habit of conducting an annual review of your retirement strategy. Checking your updated statements against your current working status guarantees you will never be caught off guard by the earnings test or related regulations. Knowledge is your most powerful asset when securing a blissful, worry-free retirement.

The Takeaway: Living a More Blissful Retirement

Navigating the complex maze of Social Security rules does not have to be a stressful endeavor. While the Retirement Earnings Test frequently catches well-intentioned workers by surprise, you now possess the knowledge to avoid its hidden pitfalls. Understanding how your earned income interacts with your claiming age allows you to make confident, empowering choices about your future.

Remember that the rules are designed to balance the system, not to punish you for staying active. Whether you choose to delay your claim, manage your work hours carefully, or lean on passive investments, you hold the power to shape your financial destiny. By continuously educating yourself and optimizing your retirement income strategy, you ensure your golden years remain full of freedom, joy, and profound peace of mind.

Frequently Asked Questions

Does the earnings limit apply after I reach Full Retirement Age?

No, the Retirement Earnings Test disappears entirely once you reach your full retirement age month. From that moment forward, you can earn an unlimited amount of money from your employer or your business without triggering any reductions to your Social Security benefits.

How does the Social Security Administration know how much I am earning?

The government tracks your income primarily through the W-2 forms submitted by your employer and the tax returns you file each year. Because there is often a delay in this reporting, the Social Security Administration may discover you exceeded the limit after they have already paid you. In these cases, they will withhold future checks to recover the overpayment.

Can I change my mind if I claimed early and hate the earnings test penalty?

Yes, you have options. If you realize your early claim was a mistake, you can formally withdraw your application within the first twelve months of receiving benefits, provided you repay all the money you and your family received. Alternatively, once you reach your full retirement age, you can voluntarily suspend your benefits to earn delayed retirement credits, which will boost your monthly payout later.

Are Medicare premiums still deducted if my check is reduced to zero?

If the earnings test reduces your monthly Social Security check to zero, the government cannot automatically deduct your Medicare Part B premiums. You will receive a direct bill from the Centers for Medicare & Medicaid Services. You must pay this premium directly to maintain your essential health coverage.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply