Your financial peace of mind hinges on understanding how the annual COLA adjustment actually impacts your bottom line against rising inflation costs. We break down exactly how your Social Security increase measures up to soaring grocery bills, skyrocketing utility rates, and climbing property taxes so you can build a resilient budget. Balancing senior finances requires looking beyond the headline percentage to see the real-world math dictating your daily expenses. You will discover practical ways to stretch your retirement income, tap into local assistance programs, and optimize your spending habits. Grasping the gap between your benefits and actual living costs gives you the power to make proactive choices, ensuring your golden years remain comfortable, secure, and genuinely fulfilling.

Tip #1: Decode How the COLA Adjustment Actually Works

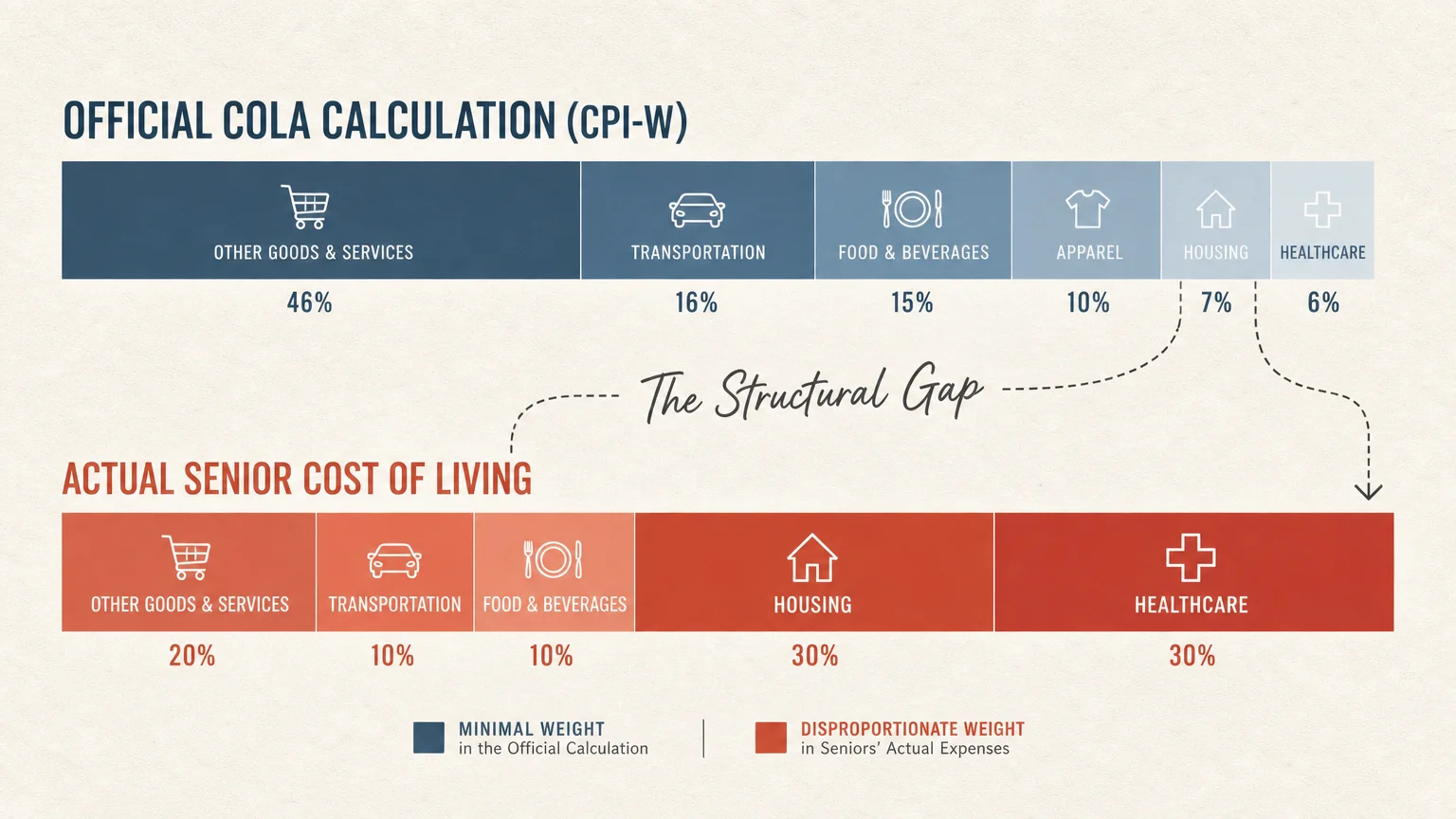

The federal government uses the Consumer Price Index for Urban Wage Earners and Clerical Workers to calculate your annual COLA adjustment. This specific index tracks the spending habits of younger, working-class Americans who typically allocate significantly less of their monthly budget to healthcare and housing than you do. Because older adults spend disproportionately more on medical care and prescription drugs, the official metric often fails to capture the true burden on senior finances. When a Social Security increase is announced, it relies on economic data pulled from the third quarter of the previous year; this structural delay means the adjustment inherently lags behind the real-time prices you pay at the register today.

You might notice your monthly benefit goes up by fifty dollars, but your combined utility and grocery bills jump by one hundred dollars within the same timeframe. Grasping this structural gap helps you realize that you are not doing anything wrong with your budget. The system simply relies on a generalized formula that does not perfectly mirror your lived reality. You can take control by maintaining a personal inflation journal for a few months. Track exactly what you spend on utilities, food, and pharmacy runs. Comparing your personal inflation rate against the official government figures provides absolute clarity. Acknowledging this discrepancy empowers you to take charge of your spending rather than passively relying on the annual increase to cover every newly elevated expense.

Tip #2: Strategize Your Grocery Shopping to Combat Rising Food Prices

Food costs remain one of the most volatile components of your daily budget. Supermarket prices fluctuate wildly based on supply chain disruptions, fuel costs, and unpredictable agricultural yields. To shield your retirement income from these persistent inflation costs, you must adopt a highly strategic approach to grocery shopping. Start by planning your meals around weekly store circulars and loss leaders; these are specific items retailers sell at a deep discount just to get you through the front door. Build your weekly menu around these heavily discounted proteins and seasonal vegetables rather than deciding what you want to eat and paying full premium prices for the ingredients.

You can further reduce expenses by embracing store brands, which often roll off the exact same manufacturing lines as their premium-priced counterparts. Make a strict habit of checking the unit price on shelf tags to ensure you actually get the best deal, as packaging sizes frequently shrink while prices remain exactly the same—an economic phenomenon known as shrinkflation. Consider expanding your culinary skills to include more plant-based meals a few times a week; beans, lentils, and chickpeas provide exceptional nutrition at a fraction of the cost of beef or poultry. Furthermore, pay close attention to the physical layout of your local grocery store. Retailers intentionally place the most expensive, highly processed items exactly at eye level. Looking down at the bottom shelves often reveals substantial savings that keep your grocery budget fully intact.

Tip #3: Fortify Your Home Against Escalating Energy Rates

Keeping your living space comfortable year-round requires significantly more money today than it did a decade ago. Energy providers continually pass their increased operational and fuel costs directly to consumers, making utility bills a massive, unpredictable drain on senior finances. You can actively fight back by optimizing your home for maximum energy efficiency. Begin by requesting a professional home energy audit; many utility companies offer this service completely free of charge and will even provide complimentary LED lightbulbs, smart power strips, or low-flow showerheads during the technician’s visit. Seal drafts around your aging windows and doors using inexpensive silicone caulking to prevent your climate-controlled air from escaping into the neighborhood.

You should also consider adjusting your thermostat by just a few degrees—setting it slightly warmer in the summer and slightly cooler in the winter. Wearing layered clothing indoors allows you to remain perfectly comfortable while significantly reducing the heavy workload on your heating and cooling systems. Additionally, unplug phantom energy drainers—such as coffee makers, guest room televisions, and charging blocks—when they are not in active use. These modern devices constantly draw a small amount of electricity, which silently inflates your monthly statement. Finally, contact your utility provider immediately to request enrollment in a level-billing or budget-billing program. This service averages your annual energy usage into twelve predictable monthly payments, completely preventing severe bill shock during extreme weather months.

Tip #4: Navigate Soaring Housing Costs and Property Taxes

Whether you rent your home or own it outright, the roof over your head likely represents your single largest and most rigid monthly expense. Renters face steep annual lease renewals, while homeowners grapple with spiking property insurance premiums and climbing tax assessments driven by artificially inflated home values. If you own your property, research your local and state tax codes today to identify senior-specific exemptions. Many municipalities offer a property tax freeze for adults over the age of sixty-five who meet specific income thresholds. This crucial legislative benefit locks your tax rate in place, permanently shielding you from future assessment hikes that could threaten your ability to stay in your home.

Do not assume your current tax assessment is inherently accurate. Local governments utilize mass appraisal techniques that often overlook the specific nuances or deferred maintenance of your individual property. If your assessment seems unreasonably high, you have the absolute right to file a formal appeal with your county assessor’s office. If you currently rent your living space, establishing open and proactive communication with your landlord pays massive dividends. Propose signing a longer-term lease, such as twenty-four months, in exchange for locking in your current rental rate. When local housing costs become entirely disproportionate to your Social Security increase, downsizing to a more manageable space or relocating to a vibrant region with a lower cost of living provides a powerful way to reclaim total control over your financial destiny.

Tip #5: Manage the Hidden Threat of Rising Healthcare Expenses

Medical expenses relentlessly consume a large portion of your monthly budget, and these specific costs historically rise much faster than general consumer goods. Even when you receive a favorable COLA adjustment, a simultaneous increase in your standard Medicare Part B premium often absorbs a significant chunk of that extra money before the check ever reaches your bank account. You must proactively manage your healthcare spending to preserve your overall financial health and ensure you receive the care you deserve. Dedicate serious time during the annual Medicare Open Enrollment period to meticulously review your Part D prescription drug coverage. Formulary lists change every single year; a medication that cost you ten dollars last year might unexpectedly jump to a higher pricing tier this year.

Input your current prescriptions into the official Medicare website tool to mathematically verify the most cost-effective plan for your specific pharmaceutical needs. Consider the immense benefits of utilizing a preferred mail-order pharmacy for medications you take on a permanent basis. Many comprehensive insurance plans offer a ninety-day supply of maintenance drugs at a drastically reduced copay compared to picking up a thirty-day supply at your local neighborhood pharmacy. Do not hesitate to ask your primary care physician if therapeutic alternatives or generic versions exist for your expensive brand-name medications. Taking these diligent, highly calculated steps ensures your medical care continuously supports your physical vitality without unnecessarily depleting your hard-earned retirement income.

Tip #6: Maximize Returns on Your Guaranteed Cash Reserves

Protecting your principal remains paramount during your golden years, but letting your savings languish in a traditional bank account paying near-zero interest actively damages your long-term purchasing power. As inflation costs steadily diminish the absolute value of your dollar, you must ensure your emergency funds and cash reserves work just as hard as you did to earn them. High-yield savings accounts and certificates of deposit currently offer some of the most attractive, risk-free interest rates seen in decades. Moving a portion of your liquid assets from a legacy brick-and-mortar institution to a reputable online bank instantly generates a brand new stream of passive retirement income.

These modern online institutions carry the exact same Federal Deposit Insurance Corporation protections as your local branch down the street, strictly guaranteeing the absolute safety of your deposits up to the federal limit. You can easily link these lucrative high-yield accounts directly to your primary checking account, allowing you to transfer funds quickly whenever a sudden financial need arises. You should also investigate Series I Savings Bonds backed directly by the federal government. These unique financial instruments are specifically designed to protect your purchasing power by offering a dynamic interest rate tied directly to current inflation metrics. Evaluate your current banking structure today and calculate exactly how much extra money you could generate simply by relocating your stationary cash.

Tip #7: Tap Into Essential Community and Federal Assistance Programs

Far too many older adults leave valuable financial benefits on the table due to a lack of simple awareness or a misplaced sense of personal pride. These robust state and federal assistance programs exist specifically to support your senior finances; you actively paid into this vast system through decades of hard work and taxation, and you fully deserve to utilize these critical safety nets today. The Low Income Home Energy Assistance Program provides direct financial grants to help immediately cover the mounting costs of heating and cooling your home. The Supplemental Nutrition Assistance Program offers a reliable monthly stipend loaded onto a discreet debit card, directly subsidizing your essential grocery trips.

Furthermore, the Medicare Savings Programs can completely cover your Part B premiums, annual deductibles, and co-insurance if you meet the specific income and asset limits for your state. Reach out to your local Area Agency on Aging this week to schedule a comprehensive, confidential benefits screening. Their expert counselors will gently guide you through the various application processes, helping you navigate the complex paperwork with absolute ease. Many utility providers, telecom companies, and even local transit authorities also offer unadvertised senior discount rates. Combining these hyper-local discounts with sweeping federal grants creates an impenetrable financial fortress around your bank account, significantly elevating your daily quality of life.

The Takeaway: Living a More Blissful Retirement

Flourishing in your golden years demands a pragmatic blend of financial vigilance and an unwavering optimistic mindset. While escalating expenses for daily necessities present undeniable challenges, you possess the life wisdom and the fierce resourcefulness to adapt your lifestyle effectively. By deeply understanding the mechanics of your COLA adjustment and aggressively optimizing your household spending, you strip away the anxiety typically associated with shifting economic tides. Small, intentional changes to how you purchase groceries, cool your home, and manage your pharmacy runs compound rapidly, creating a wide, comforting buffer of financial security.

Remember that actively seeking out community resources, claiming your rightful tax exemptions, and transitioning to high-yield banking options serves as a powerful testament to your proactive intelligence, not a sign of defeat. You hold the ultimate authority to shape your retirement experience from this day forward. Implementing these highly practical strategies ensures your retirement income continuously supports the vibrant, joyful, and deeply fulfilling life you so richly deserve.

Frequently Asked Questions

Why does my Social Security increase feel noticeably smaller than my actual rising expenses?

The federal government calculates your annual adjustment using an inflation index based entirely on younger wage earners, not retirees. Because you likely spend a much larger percentage of your retirement income on housing and healthcare—categories that inflate very rapidly—the standard percentage bump often falls short of covering your true, specialized daily costs.

Can I formally appeal my Medicare premium surcharge if my financial situation recently changed?

Yes; if you experienced a qualifying life-changing event such as a permanent reduction in work hours, marriage, divorce, or the loss of a company pension, you can file an appeal using Form SSA-44. This official process asks the administration to recalculate your premium based on your current senior finances rather than relying on your historical tax returns from two years ago.

Are there specific, reliable programs to help offset high inflation costs for my home utilities?

Absolutely. The Low Income Home Energy Assistance Program provides federally funded grants specifically to assist older adults with utility bills and minor weatherization projects. Contact your local community action agency or Area Agency on Aging to determine your exact eligibility and start the straightforward application process today.

How can I better protect my fixed monthly budget from future economic shifts?

The absolute best defense involves a deliberate combination of fixed-expense reduction and highly active cash management. Lock in local property tax freezes, permanently switch to level-billing for your utilities, and keep your liquid savings housed in high-yield accounts. Consistently reviewing your out-of-pocket medical costs ensures your budget remains highly resilient regardless of the economic climate.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply