Planning your senior finances carefully guarantees you can travel, explore new hobbies, and spoil your grandchildren without losing sleep over sudden bills. Understanding hidden retirement costs early gives you the power to stretch your savings and maintain a rich, active social life. Many Americans step away from their careers only to encounter unexpected financial hurdles that threaten their peace of mind. By identifying the exact retirement expenses that often shock new retirees, you can adjust your retirement budgeting strategy today. Staying ahead of these surprises ensures your transition remains an exciting chapter filled with endless opportunities for personal growth, joyful family connections, and stress-free daily living.

Lifestyle Idea #1: Funding Your Rising Healthcare Premiums and Out-of-Pocket Costs

Navigating the complex landscape of healthcare requires proactive retirement planning, since medical expenses represent a massive financial shock for new retirees. Many individuals mistakenly assume Medicare covers every health-related bill; however, standard coverage leaves significant gaps. You must account for Medicare Part B premiums, Part D prescription drug plans, and potential surcharges if your retirement income exceeds certain thresholds. Furthermore, deductibles and co-payments accumulate rapidly when you face unexpected health challenges. Estimates show a single sixty-five-year-old retiring today might need over one hundred fifty thousand dollars saved strictly for healthcare. To protect your senior finances, consider purchasing a supplemental Medigap policy to absorb out-of-pocket costs. By dedicating a specific portion of your monthly retirement budgeting strictly to medical care, you eliminate the anxiety of sudden doctor bills. Take time to review your prescriptions annually; switching your Part D plan can yield substantial savings. Exploring Health Savings Accounts (HSAs) before you stop working also provides a tax-advantaged buffer for future medical necessities. This financial security empowers you to stay active, prioritize preventative care, and fully enjoy your golden years.

Lifestyle Idea #2: Financing Relocation, Downsizing, and Aging in Place Upgrades

Transforming your current residence into a comfortable haven for your later years demands careful financial foresight. You might envision a seamless transition to a vibrant 55-plus community, yet the actual costs of downsizing frequently catch Americans off guard. Real estate agent commissions, moving company fees, and new furniture purchases consume a significant portion of your liquid assets. Conversely, if you choose to age in place, your beloved family home will likely require practical modifications. Widening doorways, installing walk-in showers with secure grab bars, and upgrading lighting systems to prevent falls cost thousands of dollars. Comprehensive aging-in-place renovations easily surpass twenty thousand dollars. Even basic maintenance—such as hiring landscapers or roofers—adds recurring line items to your budget. Additionally, moving to a different state involves hidden retirement costs like shifting property tax rates, varying homeowner association fees, and unexpected utility deposits. Assess your housing strategy early by requesting quotes from local contractors or real estate professionals. Establishing a dedicated housing fund guarantees your living environment remains a sanctuary rather than a financial burden.

Lifestyle Idea #3: Covering Unexpected Taxes on Social Security and Pensions

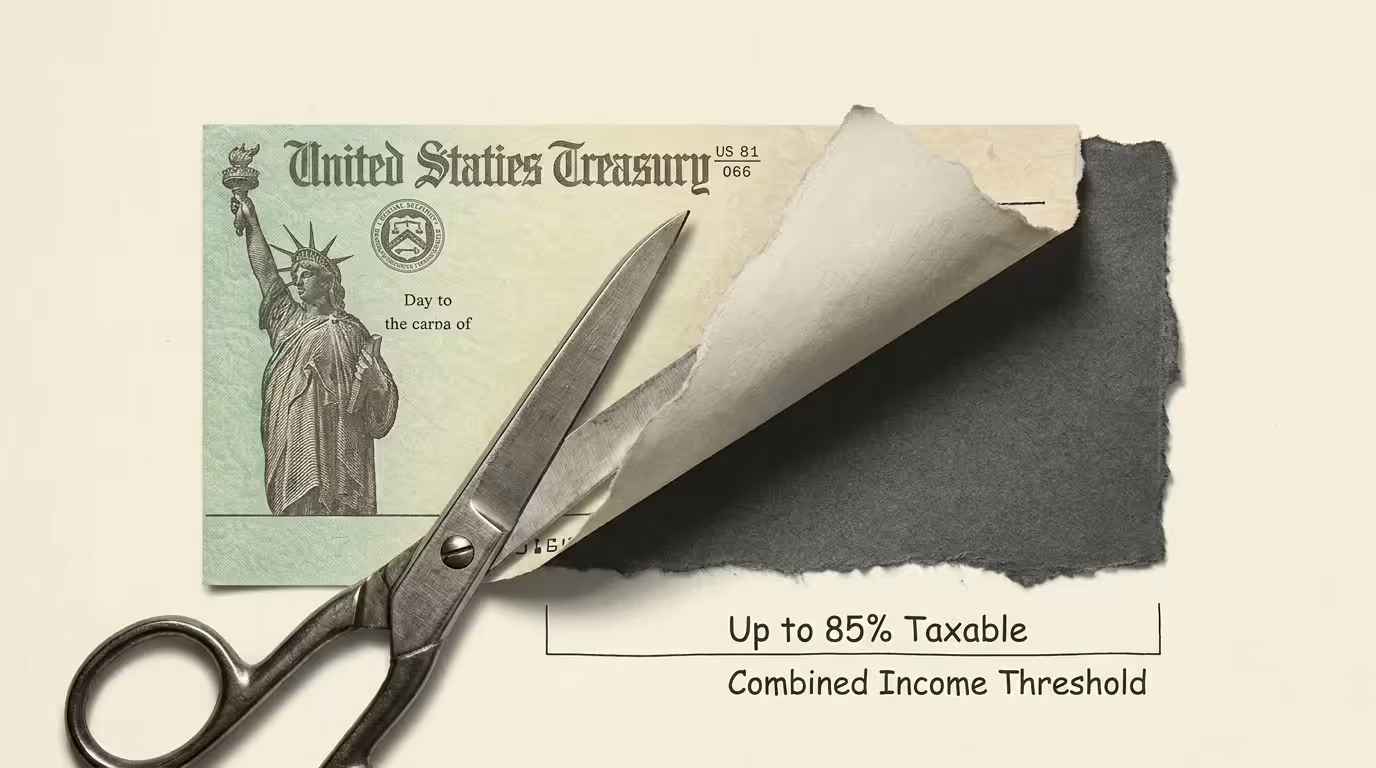

Managing your tax burden in retirement requires an entirely new set of strategies compared to your working years. Many new retirees experience profound shock when they realize the Internal Revenue Service still demands a considerable share of their income. Depending on your combined income, up to eighty-five percent of your Social Security benefits could be subject to federal income taxes. Furthermore, distributions from traditional 401(k)s and standard Individual Retirement Accounts (IRAs) trigger ordinary income tax liabilities. As you reach age seventy-three, Required Minimum Distributions (RMDs) force you to withdraw specific amounts from these accounts, potentially pushing you into a higher tax bracket. State taxes also vary wildly; while some states exempt pension income, others tax it heavily. Partner with a fiduciary financial advisor to develop a tax-efficient withdrawal strategy. Executing Roth IRA conversions during lower-income years or utilizing Qualified Charitable Distributions (QCDs) can dramatically reduce your lifetime tax bill. Educating yourself on the tax implications of your investments translates directly into financial freedom, giving you the confidence to spend your hard-earned money without fearing a massive bill.

Lifestyle Idea #4: Managing the High Price of Dental, Vision, and Hearing Care

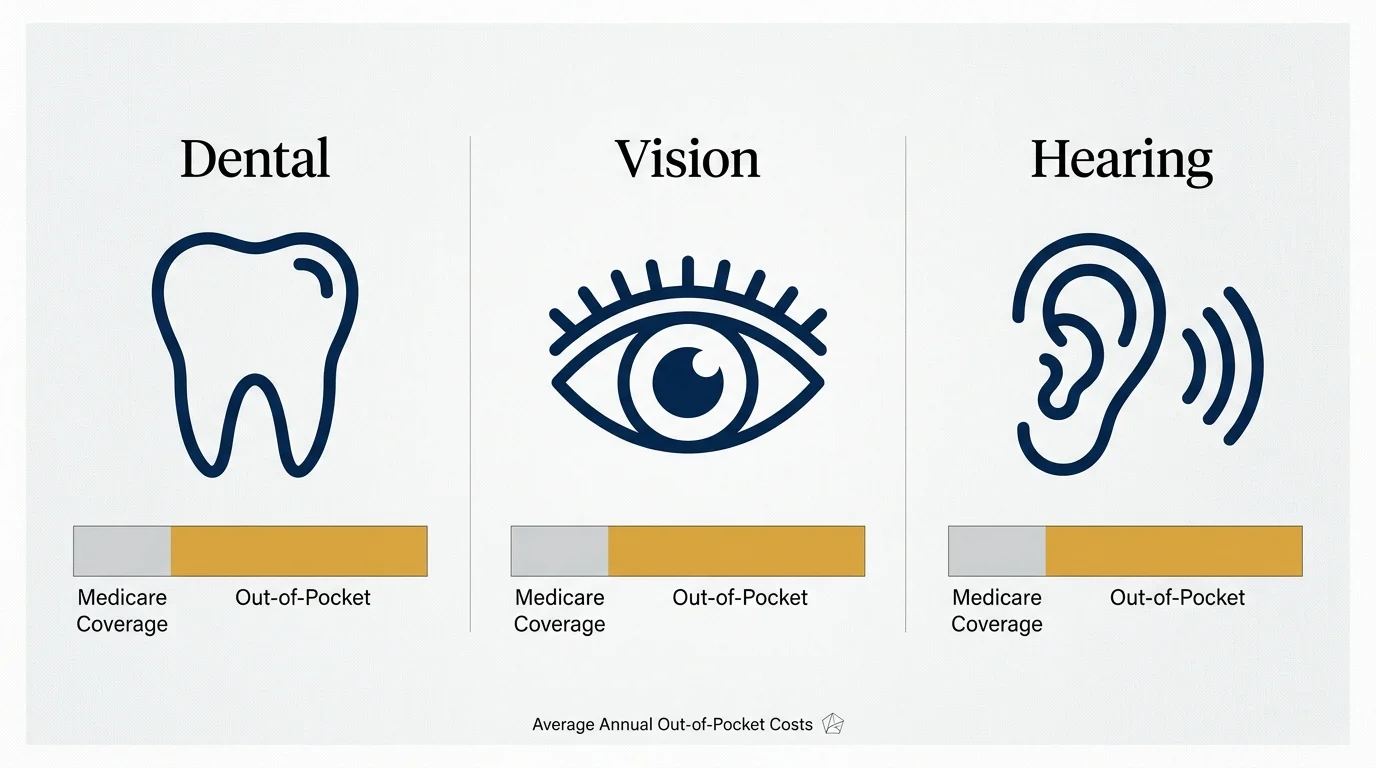

Maintaining your sensory health and a radiant smile is vital for your overall well-being, yet traditional Medicare completely excludes routine dental, vision, and hearing care. Retirees often face intense sticker shock when confronting the cost of a single dental implant, which can easily exceed three thousand dollars. Similarly, a quality pair of modern hearing aids frequently costs between four and six thousand dollars—an expense you must shoulder entirely out of pocket unless you carry specialized insurance. Neglecting these areas due to cost leads to isolation; hearing loss significantly hampers your ability to engage in lively conversations or enjoy theatrical performances. Protect your senior finances by exploring standalone dental and vision insurance policies or evaluating Medicare Advantage plans that include supplementary benefits. Alternatively, establish a sinking fund within your savings strictly dedicated to hearing and dental maintenance. Proactive care is equally important; regular check-ups prevent minor issues from escalating into expensive surgeries. Prioritizing these out-of-pocket costs in your retirement budgeting ensures you remain fully engaged with your community and favorite activities.

Lifestyle Idea #5: Budgeting for Increased Leisure, Hobbies, and Travel Spending

Embracing a schedule where every day feels like a Saturday is the ultimate reward for decades of hard work, but this newfound freedom carries substantial hidden retirement costs. During the initial active phase of retirement—often called the go-go years—your spending on entertainment, dining out, and travel will likely surge past your previous working-year levels. You now possess the time to join exclusive clubs, take month-long European river cruises, or invest heavily in expensive hobbies like woodworking. Without the forty-hour workweek occupying your time, continuously spending money becomes a genuine temptation. To balance your zest for life with financial prudence, implement a dynamic spending plan. Allocate a specific monthly allowance for guilt-free leisure activities. Take advantage of senior discounts, travel during off-peak seasons, and seek out free community events that provide deep fulfillment without the hefty price tag. Tracking these expenses for the first six months after you quit working provides a realistic baseline for your future budget. Structuring your recreational spending allows you to vigorously explore the world while safeguarding your nest egg.

Lifestyle Idea #6: Supporting Adult Children and Spoiling Grandchildren

Fostering deep connections with your family brings immeasurable joy, yet your generosity can quietly undermine your long-term financial stability. Many Americans significantly underestimate the amount they spend assisting adult children with down payments, subsidizing weddings, or funding college education through 529 plans. Even everyday spoiling—like buying extravagant holiday gifts, paying for summer camps, or covering the tab during large family dinners—adds up to thousands of dollars annually. While sharing your wealth feels rewarding, you cannot secure a loan to fund your retirement; your children, however, can borrow for their education or housing needs. Protect your senior finances by establishing clear, loving boundaries regarding financial assistance. Communicate openly with your family about your fixed income and shifting priorities. Consider gifting your time and wisdom—such as hosting weekly family dinners, teaching your grandchildren a valuable skill, or planning affordable local outings—which creates priceless memories without jeopardizing the funds you need for your own future care. Generosity should never force you into a precarious financial position later in life.

Lifestyle Idea #7: Paying for Long-Term Care and In-Home Assistance

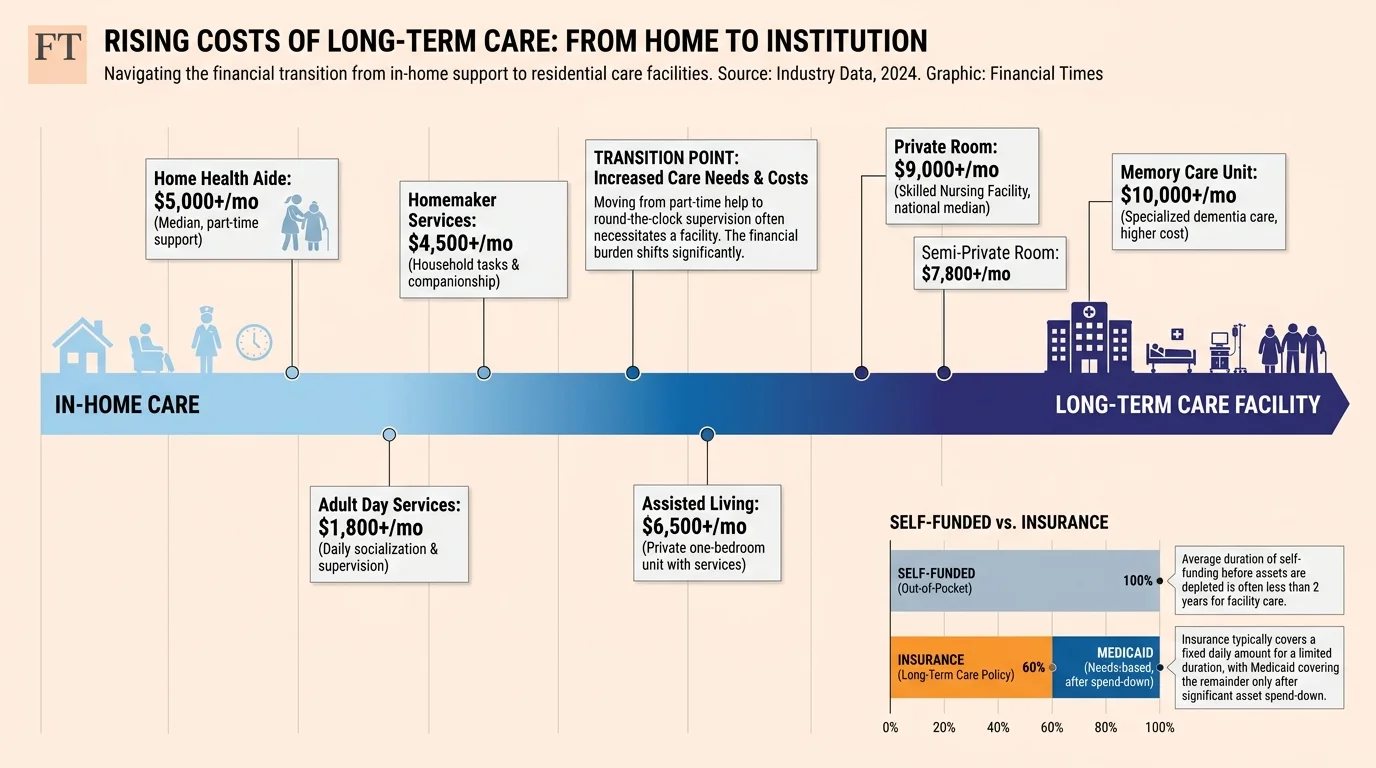

Planning for your future mobility and personal care needs remains one of the most critical aspects of retirement planning. The staggering cost of long-term care represents the most significant financial threat to unprepared retirees. Standard health insurance and Medicare do not cover custodial care, which includes assistance with daily activities like bathing, dressing, and eating. Whether you eventually require a home health aide, transition to an assisted living facility, or need specialized memory care, the expenses are astronomical. Industry data reveals a private room in a nursing home regularly exceeds one hundred thousand dollars annually, a figure that continues to rise with inflation. To prevent this expense from wiping out your life savings, you must explore your funding options well before the need arises. Look into long-term care insurance policies, hybrid life insurance products with long-term care riders, or strategically earmarking a portion of your portfolio for self-funding. Discuss your preferences with your family early on, clearly outlining your wishes for in-home care versus facility living. Confronting this uncomfortable topic today guarantees your final years are characterized by dignity and comfort.

Lifestyle Idea #8: Replacing the Hidden Perks and Benefits Provided by Your Employer

Stepping away from your career means leaving behind a subtle web of financial subsidies that quietly supported your lifestyle for decades. Most professionals severely underestimate the cash value of employer-provided perks until they have to purchase them independently. You will instantly lose access to subsidized group life insurance, matching 401(k) contributions, employer-sponsored health savings account deposits, and potentially comprehensive disability coverage. Beyond insurance, you must now cover the full cost of your cell phone plan, high-speed internet, professional association dues, fitness center memberships, and even everyday office supplies that you previously took for granted. Before you hand in your retirement notice, conduct a thorough audit of every benefit your company currently provides. Research the open market to determine exactly how much it will cost to replace these essentials. Many companies offer transition assistance or allow you to port certain insurance policies at a favorable rate; investigate these options thoroughly. Accounting for these hidden retirement costs ensures your initial budget reflects reality, preventing cash flow shortages during your first year of freedom.

Lifestyle Idea #9: Keeping Up with Inflation and the Rising Cost of Daily Living

Safeguarding your purchasing power against the relentless creep of inflation is the ultimate test of your retirement budgeting strategy. When you quit working, you rely on a relatively fixed income derived from savings, pensions, and Social Security. Historically, inflation averages around three percent annually, meaning the cost of everyday goods—from groceries and utilities to gasoline—will double over a twenty-four-year retirement period. A budget that feels incredibly comfortable at age sixty-five might leave you struggling to afford basic necessities by age eighty. Many conservative investors make the critical error of shifting their entire portfolio into low-yield bonds or cash, inadvertently guaranteeing their money will lose its value over time. To combat this silent wealth destroyer, you must maintain a diversified investment portfolio that includes growth-oriented assets like equities or real estate. Regularly review your asset allocation with a financial professional to ensure your investments outpace the rising cost of living. Consider implementing a dynamic withdrawal strategy that adjusts your spending based on current market performance and inflation rates. Embracing a long-term growth mindset transforms your nest egg into a resilient financial engine.

Putting It into Practice: Small Steps for Big Changes

Transforming your awareness of these hidden retirement costs into actionable financial security begins with a few straightforward steps. First, embrace the power of tracking your expenses diligently for three to six months. Use a simple spreadsheet or a dedicated budgeting app to monitor exactly where your money flows; this real-world data exposes vulnerabilities in your retirement planning before they become crises. Next, schedule a comprehensive review of your insurance policies, specifically targeting healthcare, Medicare supplements, and long-term care options. Gathering quotes and comparing coverage ensures you are not overpaying while highlighting areas where you might be dangerously underinsured.

It is equally crucial to initiate honest conversations with your family. Discuss your boundaries regarding financial support for adult children and clarify your preferences for aging in place or future assisted living. Establishing mutual expectations eliminates tension and protects your senior finances. Finally, partner with a certified financial planner who acts as a fiduciary. A professional can stress-test your portfolio against inflation, optimize your tax withdrawal strategies, and build a resilient framework for your future. By taking these decisive, practical actions today, you reclaim control over your financial destiny and step into retirement with unwavering confidence.

Frequently Asked Questions

How can I adjust my budget if I have already retired and am facing these hidden costs?

If you are already navigating post-career life, start by performing a ruthless audit of your discretionary spending. Identify unused memberships or luxury travel habits you can temporarily pause. Redirect those funds toward an emergency reserve for healthcare and home maintenance. You might also explore flexible income streams, such as consulting, monetizing a hobby, or taking a low-stress part-time job. Adjusting your tax withdrawal strategy with a professional frees up immediate cash flow.

Does Medicare cover any aspect of long-term care or nursing homes?

A dangerous misconception is that standard Medicare pays for long-term facility care. In reality, Medicare only covers short-term, skilled nursing rehabilitation—typically up to one hundred days following a hospital stay. It does not cover custodial care, such as assistance with dressing, bathing, or eating, which constitutes the bulk of long-term care needs. To cover these expenses, you must rely on personal savings, long-term care insurance, or Medicaid, though the latter requires exhausting nearly all personal assets.

What is the most effective way to help my grandchildren financially without hurting my retirement?

The safest approach utilizes tax-advantaged tools requiring fixed, manageable contributions rather than open-ended support. Funding a 529 college savings plan allows you to contribute regular amounts that grow tax-free. Alternatively, buy savings bonds or set up a modest custodial account. Most importantly, integrate these contributions into your formal retirement budgeting plan as a fixed expense. Never withdraw from your primary retirement accounts or delay necessary medical care to fund gifts for your family.

How do I account for inflation if I do not want to risk my money in the stock market?

While preserving capital is a priority as you age, completely avoiding the stock market exposes you to severe inflation risk. If you are risk-averse, consider diversifying with Treasury Inflation-Protected Securities (TIPS) or high-yield certificates of deposit. However, maintaining at least a small, broadly diversified allocation in high-quality dividend-paying stocks is universally recommended by experts to ensure your income keeps pace with the rising cost of daily living over a twenty-year horizon.

For resources on retirement living, travel, and finance, visit AARP. Official information on Social Security is available at SSA.gov. For travel advisories, consult the U.S. Department of State.

Disclaimer: This article provides lifestyle suggestions for informational purposes. Financial, legal, or travel decisions should be made in consultation with qualified professionals.

Leave a Reply