Protecting your hard-earned nest egg guarantees you can fully enjoy your retirement without financial stress or surprise tax bills. Navigating the complex tax codes surrounding retirement accounts requires vigilance; even a minor oversight can cost you thousands of dollars in penalties. You spent decades building your wealth, so you deserve to keep as much of it as possible. By recognizing and avoiding common pitfalls associated with IRA rules and IRA investing, you gain complete confidence in your financial future. Whether you are already taking distributions or carefully planning your next move, understanding these crucial guidelines empowers you to maximize your savings. Let us explore the smartest ways to safeguard your assets and ensure your golden years remain truly blissful.

Tip #1: Ignoring Required Minimum Distributions (RMDs)

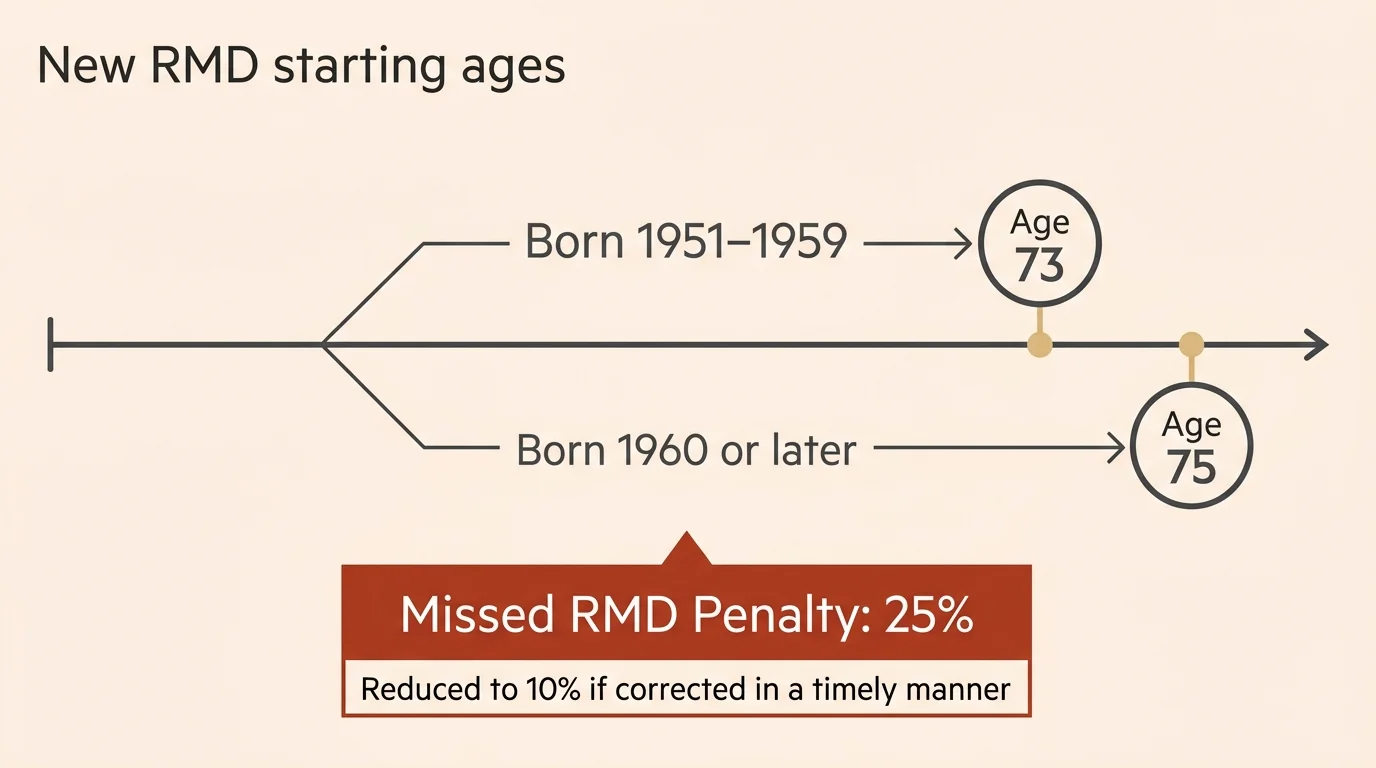

When you consistently save in a traditional IRA, the federal government gracefully defers your income taxes, allowing your money to compound rapidly. However, the IRS eventually demands their share. Required Minimum Distributions (RMDs) represent the mandatory amount you must withdraw from your tax-deferred accounts each year once you reach a certain age. Thanks to legislative changes in the SECURE Act 2.0, the starting age for RMDs recently increased. If you were born between 1951 and 1959, you must begin taking withdrawals at age 73. If you were born in 1960 or later, your RMDs do not begin until age 75. Failing to take these mandatory withdrawals on time ranks among the most costly IRA mistakes you can make in retirement planning. The Internal Revenue Service imposes a severe 25% penalty on the amount you should have withdrawn. You can potentially reduce this penalty to 10% if you correct the error in a timely manner, but avoiding the penalty entirely remains your best financial strategy. Set up automatic withdrawals with your financial institution to satisfy this strict requirement well before the December 31 deadline.

Tip #2: Missing the Spousal IRA Opportunity

Many couples mistakenly assume that once one spouse permanently stops working, that partner can no longer actively contribute to a retirement fund. This widespread misconception deprives countless families of valuable tax-advantaged growth. The IRS generally requires you to show earned income to legally contribute to an IRA. However, a helpful special provision allows a non-working spouse to utilize their working partner’s earned income to fund their own separate account. Financial professionals refer to this strategy as a Spousal IRA. If you are happily retired but your spouse continues to earn a healthy salary, your spouse can contribute the maximum allowable amount to their own IRA and simultaneously fund a separate IRA in your name. For the 2024 tax year, the individual contribution limit stands at $7,000, plus a beneficial $1,000 catch-up contribution if you are aged 50 or older. Utilizing a Spousal IRA essentially doubles your household’s annual retirement savings limit overnight. You strategically maximize your current deductions with a traditional IRA, or you build substantial tax-free income by choosing a Roth IRA. Discuss this lucrative strategy with your spouse today to capitalize on every available avenue.

Tip #3: Failing to Name or Update Beneficiaries

Major life transitions—such as a joyous new marriage, a painful divorce, the birth of a grandchild, or the passing of a cherished loved one—dramatically alter the trajectory of your financial legacy. Despite these profound life changes, many well-intentioned seniors forget to periodically update the critical beneficiary designations attached to their retirement accounts. You must internalize one critical rule: your beneficiary forms legally supersede the instructions written in your last will and testament. If your official will states that your current spouse inherits your entire estate, but your IRA documentation still incorrectly lists your ex-spouse as the primary beneficiary, the brokerage firm will legally transfer those funds directly to your ex-spouse. This preventable tragedy consistently causes immense emotional devastation and severe financial distress for surviving family members. Make it a non-negotiable annual habit to meticulously review the primary and contingent beneficiaries officially listed on all your retirement accounts. Verify that their full legal names, current contact information, and exact Social Security numbers remain accurate. Naming contingent beneficiaries actively guarantees that your hard-earned assets easily transition to your secondary choices if your primary beneficiary passes away before you do.

Tip #4: Misunderstanding the 60-Day Rollover Rule

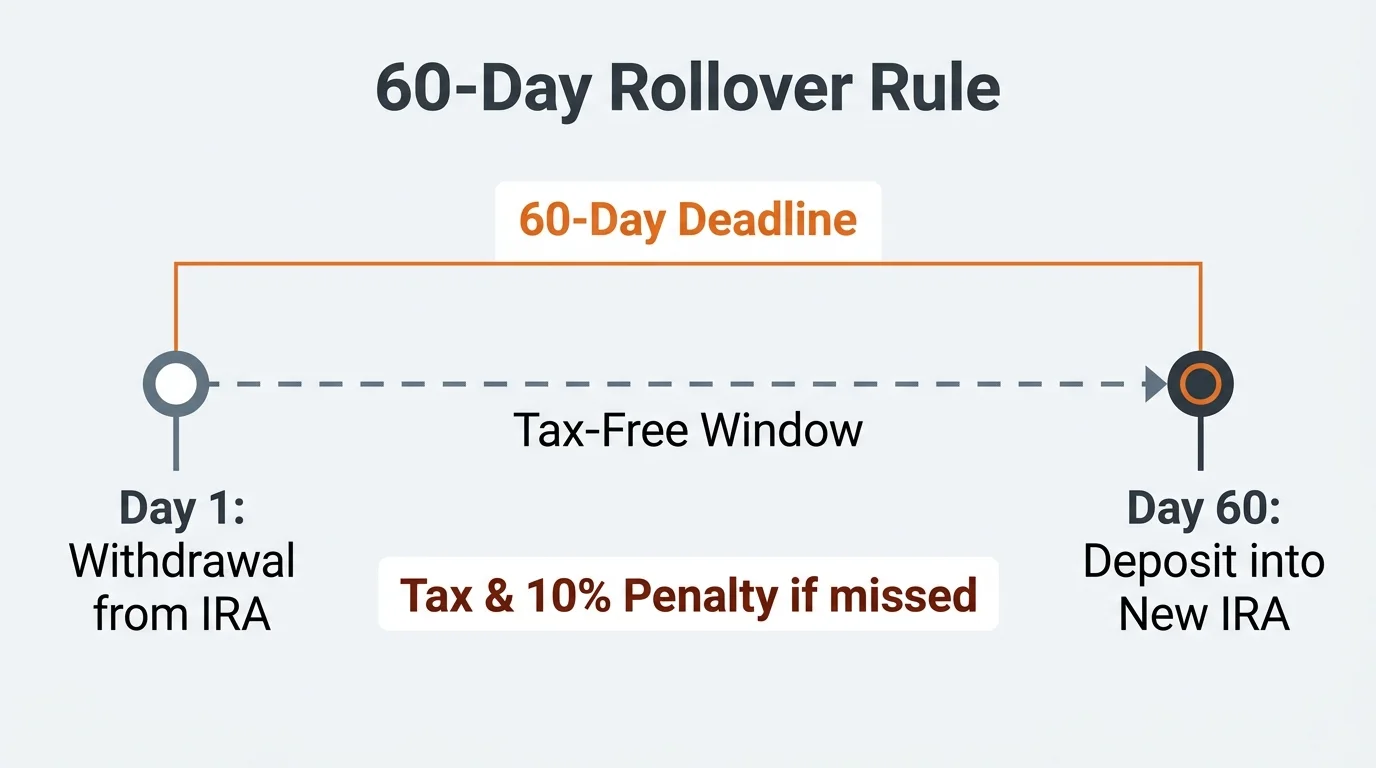

Moving your funds from one specific retirement account to another securely gives you far greater control over your various investments. However, executing this seemingly simple transfer incorrectly can instantly trigger severe tax consequences. When you perform an indirect rollover, the financial institution sends the funds directly to you in the form of a physical check or direct deposit. You then have exactly 60 strict days to deposit that entire sum of money into a brand-new qualified retirement account. If you miss this unforgiving deadline by even a single day, the IRS treats the entire gross amount as a fully taxable distribution. Furthermore, if you happen to be under the age of 59½, you will face an additional 10% early withdrawal penalty on top of your standard income taxes. To complicate matters, the IRS relentlessly enforces a stringent one-per-12-month rule limiting you to one indirect rollover across all your combined IRAs in any given year. The safest way to strategically move your money is through a formal direct rollover—also commonly known as a trustee-to-trustee transfer. In a direct rollover, the funds move straight from your old financial institution to your new one without ever touching your personal bank account.

Tip #5: Overlooking the Backdoor Roth Strategy

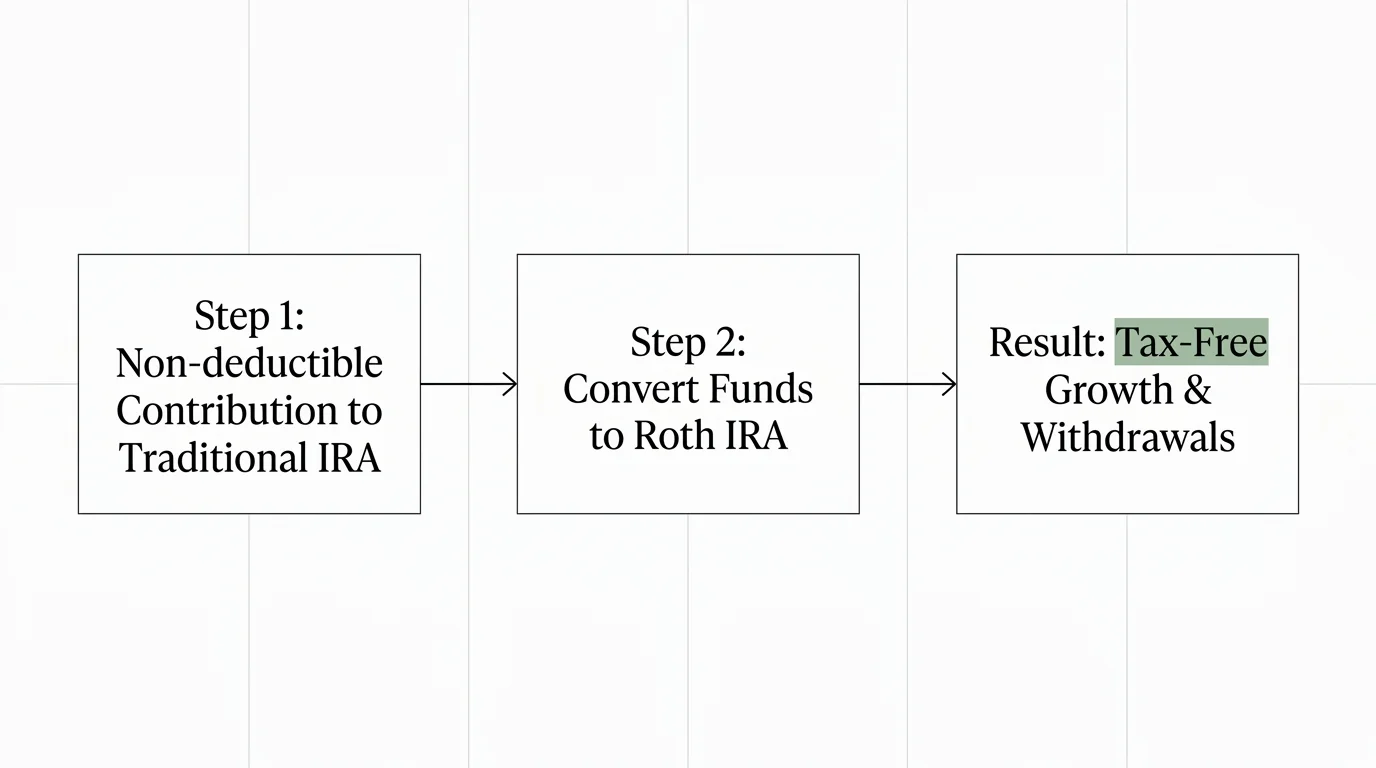

High-income earners frequently believe they earn far too much money to take advantage of the incredible tax benefits offered by Roth IRAs. The IRS intentionally phases out direct Roth contributions for married couples filing jointly when their modified adjusted gross income reaches a specific threshold—scaling between $230,000 and $240,000 for the tax year 2024. However, you can legally bypass these frustrating income limits by executing a brilliant strategy widely called the Backdoor Roth. This legitimate technique involves making a standard non-deductible contribution to a traditional IRA and then immediately converting those specific funds into a Roth IRA. Because you already paid income taxes on the initial cash contribution, the conversion process itself generates little to no additional tax liability. Once your money safely sits inside the new Roth IRA, it aggressively grows tax-free, and you will owe zero taxes on all qualified withdrawals during your eventual retirement. This proactive approach protects your accumulated wealth from future federal tax rate increases. Be mindful that this advanced strategy requires extremely careful execution and highly accurate tax reporting via official IRS Form 8606.

Tip #6: Holding Too Much Cash Instead of Investing

A remarkably common and paralyzing fear among dedicated retirees directly involves losing their life savings to wildly unpredictable stock market crashes. This intense emotional fear drives many seniors to securely keep excessively large portions of their IRA funds in pure cash or low-yielding money market funds. While meticulously preserving your initial capital feels safe and comforting in the short term, holding too much cash tragically creates a massive, silent long-term risk: devastating inflation. Inflation quietly and relentlessly erodes your true purchasing power year after year. If your blissful retirement spans 20 to 30 wonderful years, a single dollar saved today will unfortunately buy substantially less in your distant future. Truly successful IRA investing requires a balanced and pragmatic approach. You absolutely need a thoughtfully diversified portfolio that smartly includes a reliable mix of growth-oriented equities, stable bonds, and liquid cash equivalents tailored to your personal risk tolerance and exact time horizon. Equities naturally provide the vital long-term growth necessary to consistently outpace persistent inflation, while high-quality bonds offer reliable stability during scary economic downturns. Consult a dedicated financial advisor to expertly build a customized asset allocation strategy.

Tip #7: Making Ineligible Contributions

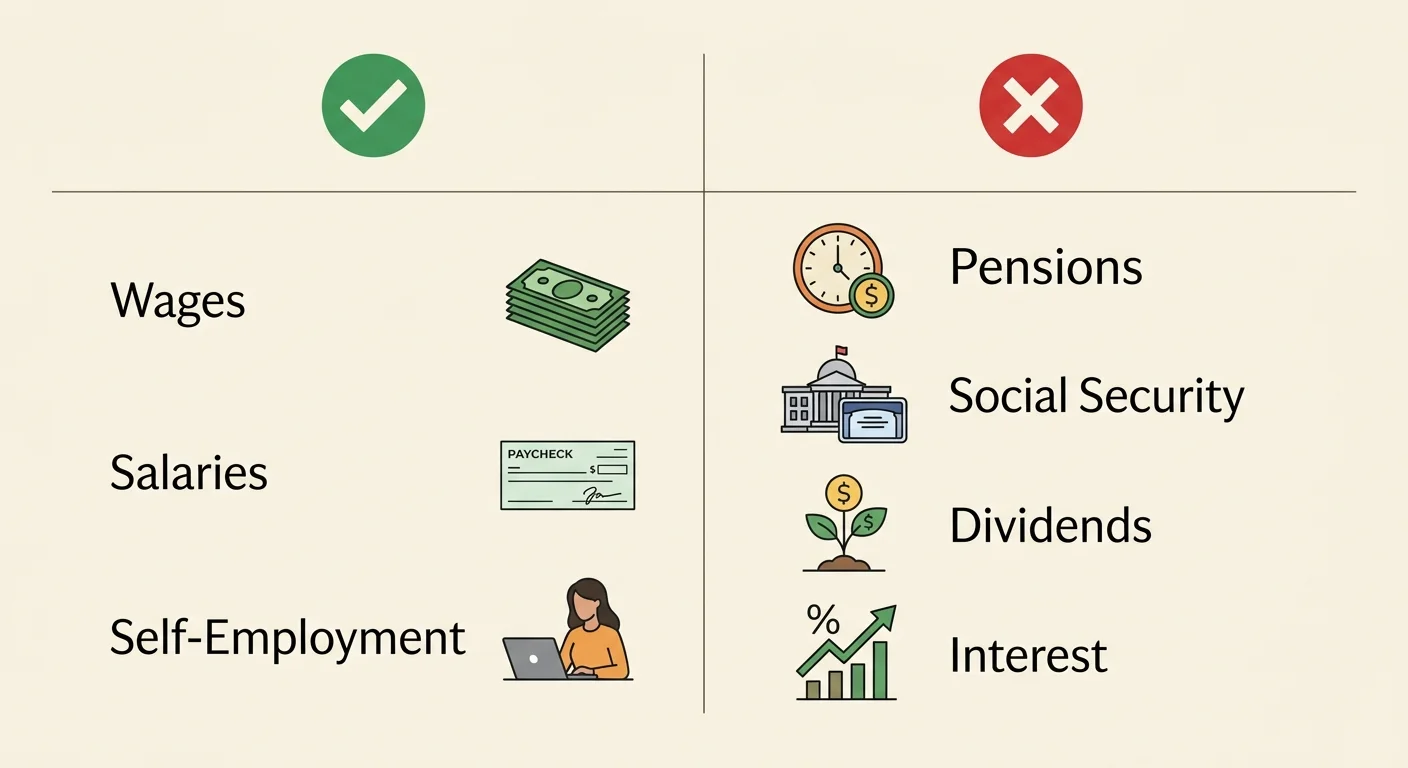

The sheer enthusiasm to rapidly save more money for your fast-approaching retirement sometimes accidentally leads to tragic violations of complex IRA rules. One highly frequent and costly error directly involves contributing significantly more money than the strict federal law currently allows. For the year 2024, the legal maximum you can collectively contribute across all your combined IRAs firmly stands at $7,000, or exactly $8,000 if you proudly qualify for the older adult catch-up contribution. If you accidentally deposit even a single solitary dollar directly over this strict limit, the IRS slaps you with a punishing 6% excise tax purely on the excess amount—every single year—until you finally remove it. Another common trap directly involves the strict earned income requirement. While the recent SECURE Act eliminated the previous age limit specifically for traditional IRA contributions, you must still generate actual taxable compensation—such as W-2 wages, typical salaries, or profitable self-employment income—to legally contribute. Standard pension payments, reliable Social Security benefits, and passive rental income simply do not qualify as true earned income. If you mistakenly make an excess contribution, carefully contact your designated brokerage immediately to request a formal return of excess contributions.

Tip #8: Forgetting About Qualified Charitable Distributions (QCDs)

Charitably inclined and incredibly generous retirees very often tragically miss out on one of the most deeply beneficial tax provisions currently available in the tax code: the Qualified Charitable Distribution (QCD). Once you officially cross the age of 70½, the IRS graciously allows you to seamlessly transfer up to exactly $105,000 per single year directly from your traditional IRA straight to a fully qualified 501(c)(3) charity. The sheer beauty of a properly executed QCD firmly lies in its incredible ability to completely satisfy your mandatory RMDs without ever adding a single taxable penny to your adjusted gross income (AGI). When you withdraw funds normally and then later write a personal check to a beloved charity, the initial withdrawal heavily increases your AGI. A drastically higher AGI can trigger far heavier taxes on your Social Security benefits and drastically increase your costly Medicare Part B and Part D premiums. By smartly utilizing a QCD, the money smoothly goes straight to the charity, completely and entirely bypassing your personal tax return. This highly streamlined process supports the beautiful causes you love while effectively keeping your total taxable income as low as humanly possible.

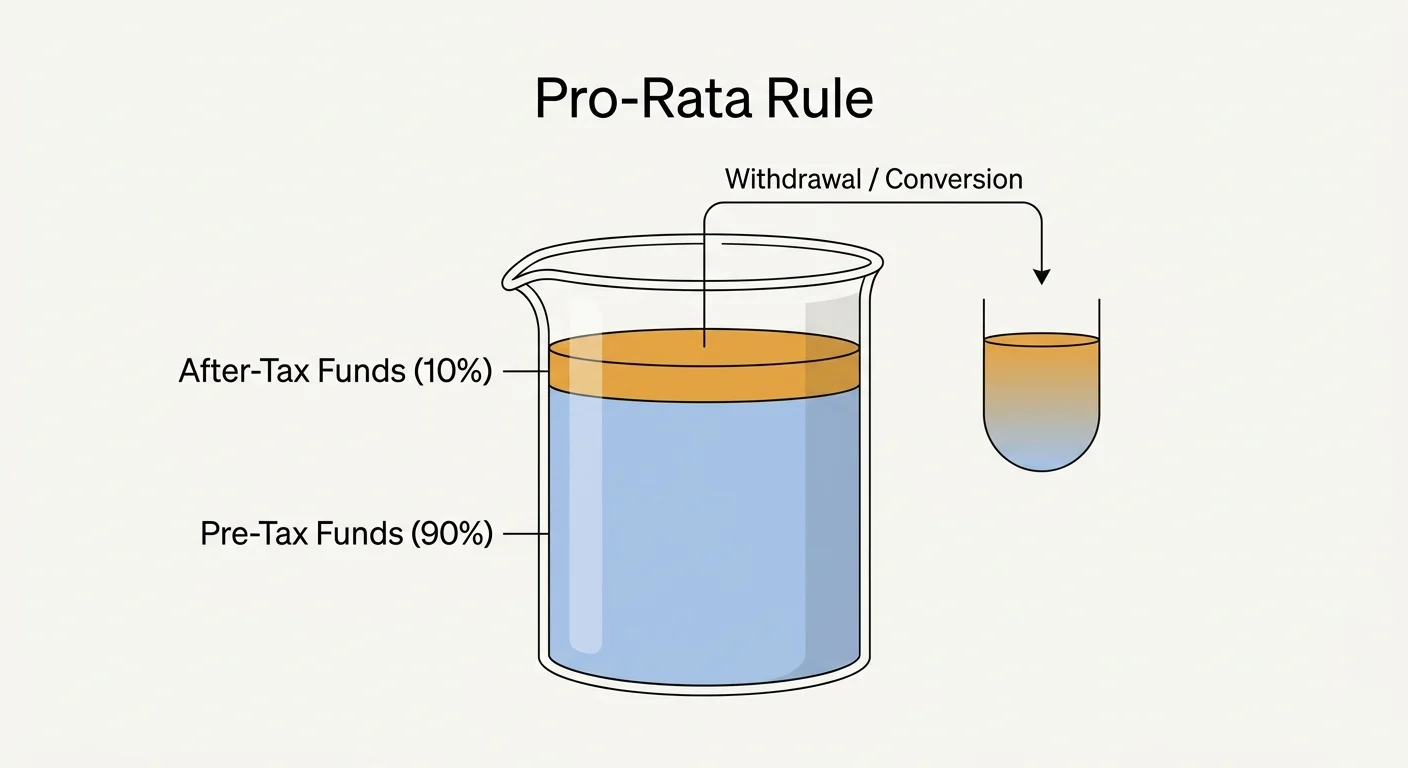

Tip #9: Triggering the Pro-Rata Rule on Conversions

Executing a highly strategic Roth conversion proudly offers truly excellent long-term tax benefits, but you absolutely must meticulously navigate the notoriously confusing pro-rata rule with extreme caution. This specific IRS regulation heavily comes into play whenever you hold a messy mix of pre-tax and after-tax funds safely scattered across any of your traditional, SEP, or SIMPLE IRAs. The IRS firmly views all your non-Roth IRAs collectively as one giant, highly blended bucket. You simply cannot individually cherry-pick only the specific after-tax dollars to efficiently convert to a Roth IRA to legally avoid paying taxes. Instead, the IRS aggressively taxes your specific conversion entirely proportionately based on the precise ratio of pre-tax to after-tax funds sitting in your total IRA balance. For instance, if your combined IRAs currently contain exactly $90,000 in untaxed pre-tax money and $10,000 in heavily taxed after-tax money, your total balance currently consists of exactly 90% pre-tax funds. If you smartly attempt to simply convert the $10,000 after-tax amount directly to a Roth, 90% of that specific conversion instantly becomes fully taxable income. Completely overlooking the complex pro-rata rule consistently results in unexpectedly massive tax bills during your retirement planning process.

Tip #10: Panicking During Market Volatility

Your daily personal behavior and emotional discipline dictate your ultimate financial success just as much as your vast knowledge of complex federal tax codes. When global macroeconomic events predictably trigger severe market corrections, helplessly watching your beloved retirement account balance steeply drop understandably causes intense personal anxiety. The immediate human impulse is to rapidly sell your diverse investments and furiously move everything directly to cash to quickly stop the terrifying bleeding. However, blind panic selling during a severe market downturn easily ranks as one of the most fundamentally destructive retirement accounts errors you can commit. When you tragically sell purely out of fear, you instantly lock in highly temporary paper losses and guarantee you will miss the eventual and highly lucrative market rebound. Historically, the robust stock market aggressively recovers from every single major crash and continues to eventually reach brand-new historic highs. Your glorious retirement securely spans multiple decades; it is absolutely a long marathon, not a frantic sprint. To successfully maintain your crucial emotional equilibrium, maintain a healthy cash reserve completely outside of your core investment portfolio to easily cover your immediate daily needs without selling stocks at a devastating loss.

The Takeaway: Living a More Blissful Retirement

Your beautifully earned golden years should fundamentally represent a glorious period of immense joy, deep relaxation, and profound personal fulfillment. You worked tirelessly for multiple decades to proudly build a substantial nest egg that comfortably supports your grandest dreams, whether that boldly involves traveling the wide world, generously spoiling your precious grandchildren, or simply enjoying perfectly quiet, peaceful mornings sipping coffee on your sunny porch. By deeply and actively avoiding these incredibly common and easily preventable missteps, you firmly protect your beloved wealth from unnecessary federal taxes and extremely severe IRS penalties. Successfully managing your critical retirement accounts effectively requires ongoing daily education and consistently proactive decision-making.

You now rightfully possess the practical knowledge to bravely and confidently manage your tricky required minimum distributions, quickly update your essential beneficiaries, and brilliantly optimize your advanced tax strategies. Always deeply remember that complex financial regulations frequently and unexpectedly change, so consistently staying highly informed provides your best personal defense against any unexpected financial setbacks. Embrace a totally holistic and comprehensive approach to your ongoing financial well-being. Smartly partner with a trusted fiduciary financial advisor and a highly qualified tax professional who can generously offer brilliant guidance securely tailored to your exact and unique personal circumstances. When you eliminate deep financial uncertainty, you completely free your soul to proudly focus on what truly matters: joyfully savoring every absolute precious moment of your incredibly well-deserved and utterly blissful retirement.

Frequently Asked Questions

Can I still contribute to my IRA if I am already retired?

You can legally contribute to an individual retirement account only if you or your married spouse officially have actual earned income successfully reported for the current tax year. The IRS strictly defines actual earned income as pure taxable compensation directly generated from actively working, such as standard salaries, hourly wages, service tips, or net business earnings from active self-employment. Passive financial income sources—including monthly Social Security benefits, standard pension payouts, lucrative rental property income, and standard stock dividends—simply do not qualify. If you happily take on a fun part-time job or proudly launch a small personal consulting business during your active retirement, you can confidently use those specific earnings to generously fund your account right up to the maximum annual federal limit.

How often should I review my retirement accounts?

You should proactively conduct a highly comprehensive and detailed review of your entire investment portfolio and specific account details at least once a single calendar year. A dedicated annual checkup wonderfully allows you to smartly rebalance your complex asset allocation, successfully ensuring your diverse investments still perfectly align with your current personal risk tolerance. Additionally, you should instantly review and update your numerous accounts immediately following any major, life-altering events. Beautiful marriages, painful divorces, joyous births, and tragic family deaths absolutely necessitate immediate and swift updates to your crucial beneficiary forms to firmly guarantee your hard-earned assets transfer perfectly smoothly to your originally intended heirs without any frustrating legal delays.

What is the main difference between a direct and indirect rollover?

A fully direct rollover safely occurs when your valuable funds successfully move directly from one specific financial institution straight to another without you ever physically taking personal possession of the actual money. This highly preferred method completely avoids mandatory tax withholding and totally bypasses extremely strict federal time limits. Conversely, an incredibly risky indirect rollover dangerously happens when the financial institution surprisingly makes the physical check fully payable directly to you. You then individually bear the massive, stressful responsibility of quickly depositing those massive funds into a brand-new qualified retirement account within exactly 60 strict days. Missing this highly unforgiving deadline instantly results in exceptionally hefty taxes and brutal early withdrawal penalties. Experts universally and passionately recommend direct rollovers for their supreme simplicity and absolute safety.

Do Roth IRAs have required minimum distributions?

No, the original proud owners of funded Roth IRAs absolutely do not have to ever take annoying required minimum distributions at any point during their entire natural lifetime. This wonderfully distinct and highly unique advantage beautifully allows your saved money to continuously and aggressively grow completely tax-free for as incredibly long as you happily live. You can confidently leave the vast funds completely untouched to strategically build a wonderfully substantial, entirely tax-free inheritance specifically for your beloved heirs. However, please be heavily aware that if you unfortunately inherit a Roth IRA directly from someone completely other than your married spouse, you generally must fully empty the entire account within exactly 10 years under current and strictly enforced IRS regulations.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply