Opening a letter to find a Social Security overpayment notice can feel jarring, but you have clear, manageable options to resolve the issue without disrupting your financial peace. By understanding the rules governing your Social Security benefits, you can swiftly navigate the appeals process, request a waiver, or establish a realistic repayment plan that protects your retirement finances. Many beneficiaries successfully handle these letters each year by taking methodical, informed steps. Instead of letting panic set in, treat this notice as a straightforward administrative hurdle. Review the details carefully, gather your personal records, and utilize the official channels designed to support you.

Tip #1: Read the Notice Carefully and Verify the Facts

The moment you receive an SSA notice regarding an overpayment, your first and most crucial step is to read every page thoroughly. The Social Security Administration sends these letters to explain exactly why they believe you received more money than you were entitled to; they also outline the specific timeframes involved and the total amount owed. Common triggers for these notices include exceeding the earning limits while taking early retirement benefits, failing to report a pension from non-covered work, or simple administrative delays within the agency itself. Do not assume the government is automatically correct.

Take a deep breath and compare the information in the letter against your own financial records. Look closely at the dates in question. Did you actually earn the amount they claim during those specific months? Was your marital status accurately recorded during that timeframe? Human error happens frequently within large administrative systems, and data entry mistakes occur more often than you might think. By gathering your pay stubs, tax returns, and bank statements, you empower yourself to verify their claims. If you discover a discrepancy between your records and their assertions, you hold the key evidence needed to challenge the notice successfully.

Tip #2: Act Quickly to Protect Your Rights

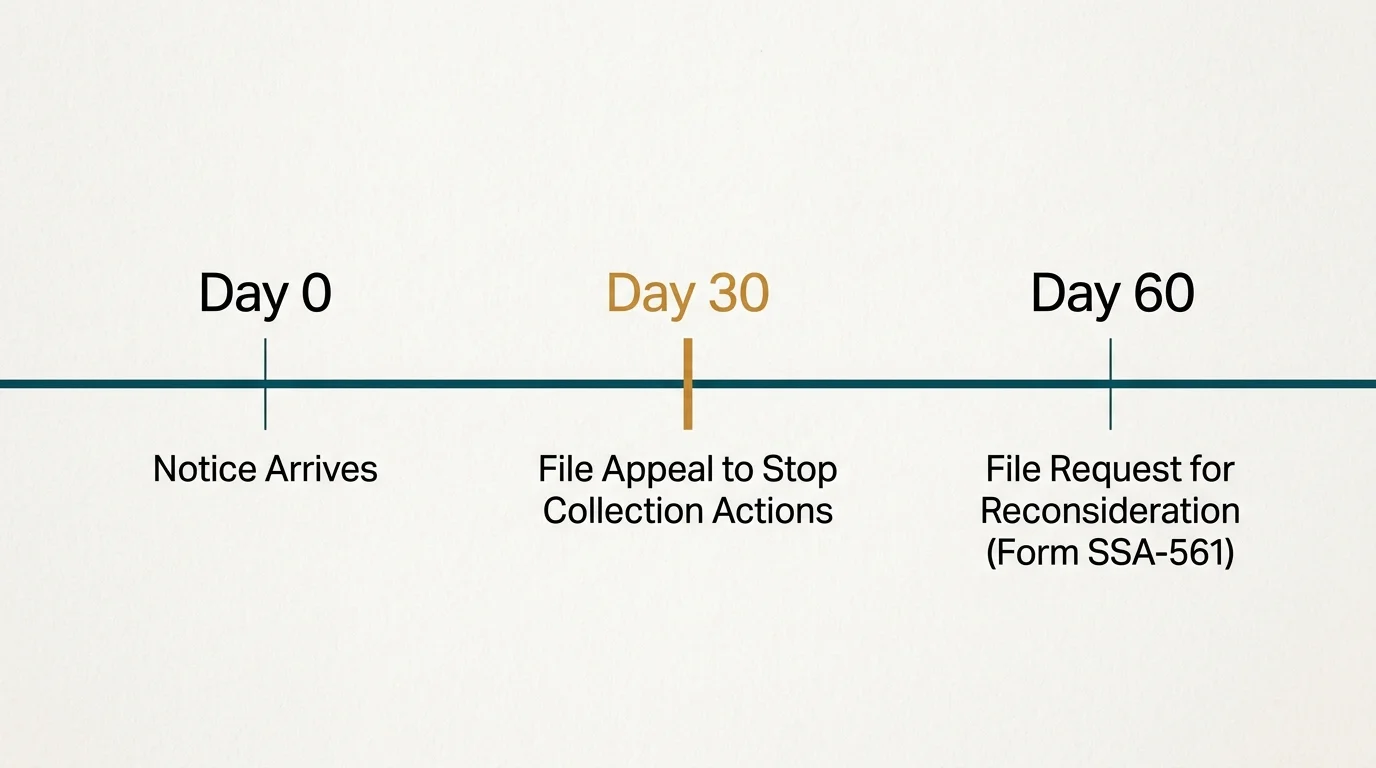

Time is of the essence when dealing with any government correspondence. The SSA operates on strict deadlines, and missing them can limit your options or trigger automatic deductions from your future checks. You generally have 30 days from the date on the notice to file an appeal if you want to stop the agency from beginning collection actions while your case is reviewed. If you agree that you owe the money but simply cannot afford to pay it back immediately, this same 30-day window is critical for setting up a specialized repayment arrangement.

Even if you miss the initial 30-day mark, you still possess rights. You have up to 60 days to file a formal appeal—known as a Reconsideration—if you believe the overpayment is entirely incorrect. Responding quickly demonstrates that you are acting in good faith and taking the matter seriously. Draft your responses, fill out the necessary forms, and submit them as soon as possible. Whenever you mail documents back to the agency, use certified mail with a return receipt requested. This provides you with concrete, undeniable proof that you met your deadlines and protected your Social Security benefits.

Tip #3: File an Appeal If You Disagree With the Decision

If your review of the facts reveals that the agency made a mistake, you should confidently file an appeal. An appeal is your formal way of telling the government that their records are incorrect and that you do not actually owe the stated amount. To initiate this process, you will need to submit Form SSA-561, officially titled “Request for Reconsideration.” On this form, you can clearly explain why you believe the overpayment calculation is wrong and attach the supporting documents you gathered during your initial review.

When you file an appeal, your case is handed over to a different representative who was not involved in the original decision. This fresh set of eyes ensures a fairer evaluation of your situation. For example, if the agency claims you exceeded your allowable earnings for the year, but your W-2 proves otherwise, your appeal should be straightforward and highly effective. You have the right to request a formal hearing before an Administrative Law Judge if your initial reconsideration is denied. Stand firm in your convictions; advocating for yourself is a vital part of protecting your long-term retirement finances.

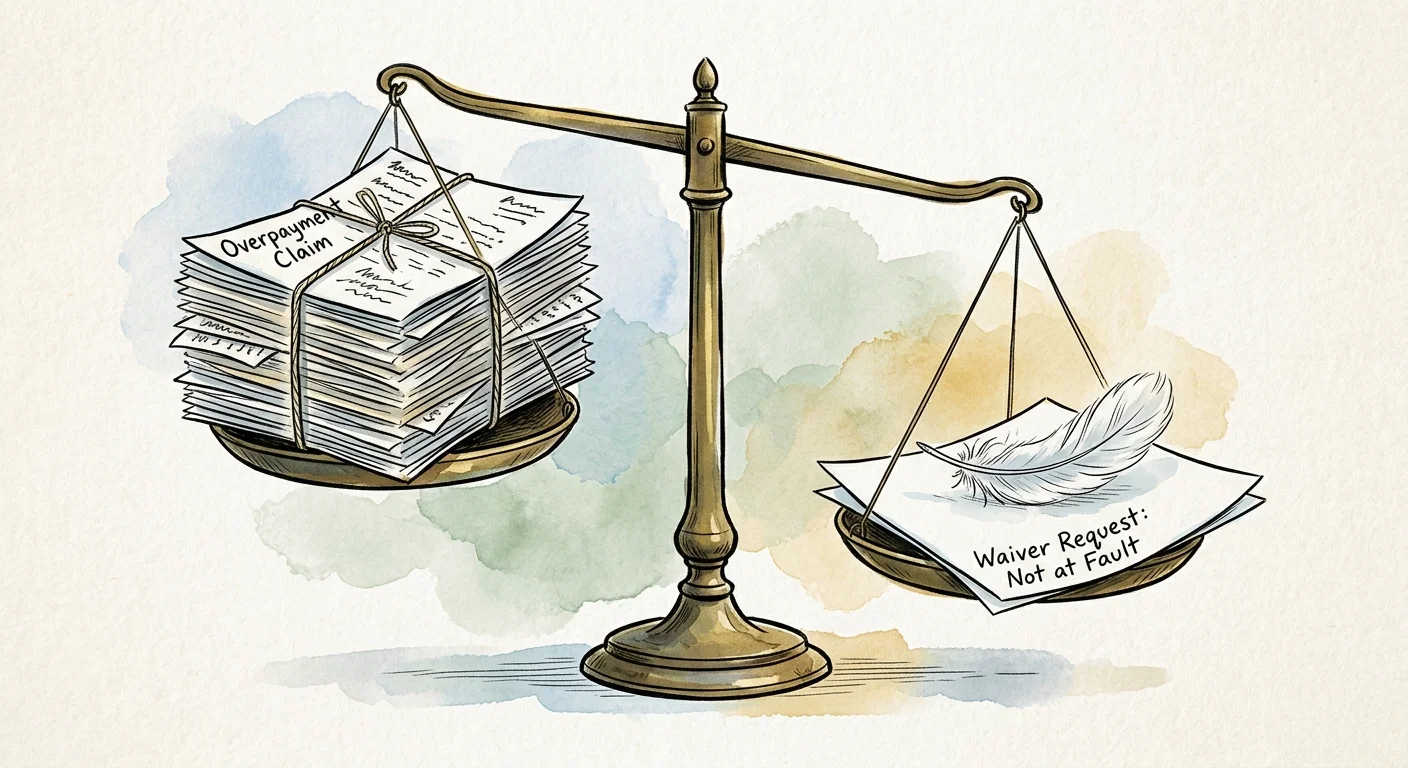

Tip #4: Request a Waiver of Overpayment Recovery

Sometimes, the agency is entirely correct about the math, but the mistake was solely their fault. If you recognize that an overpayment did occur—but you played no part in causing it—you can file for a waiver using Form SSA-632. Requesting a waiver asks the government to forgive the debt entirely. To qualify for this relief, you must prove two specific things: first, that you were entirely “without fault” in causing the overpayment, and second, that paying back the money would cause you severe financial hardship or would be blatantly unfair.

Proving you are without fault means showing that you provided all required information to the agency on time and honestly, yet they still paid you incorrectly. Proving financial hardship requires you to detail your monthly income and essential expenses—such as rent, groceries, and vital medical bills—to demonstrate that you need every dollar of your current check to survive. In 2024, the agency implemented favorable policy updates that shift the burden of proof away from beneficiaries in certain situations involving administrative errors. This progressive change makes it vastly easier for honest retirees to obtain waivers. Never feel ashamed to request a waiver; the process exists specifically to protect seniors from bearing the brunt of bureaucratic mistakes.

Tip #5: Negotiate a Manageable Repayment Plan

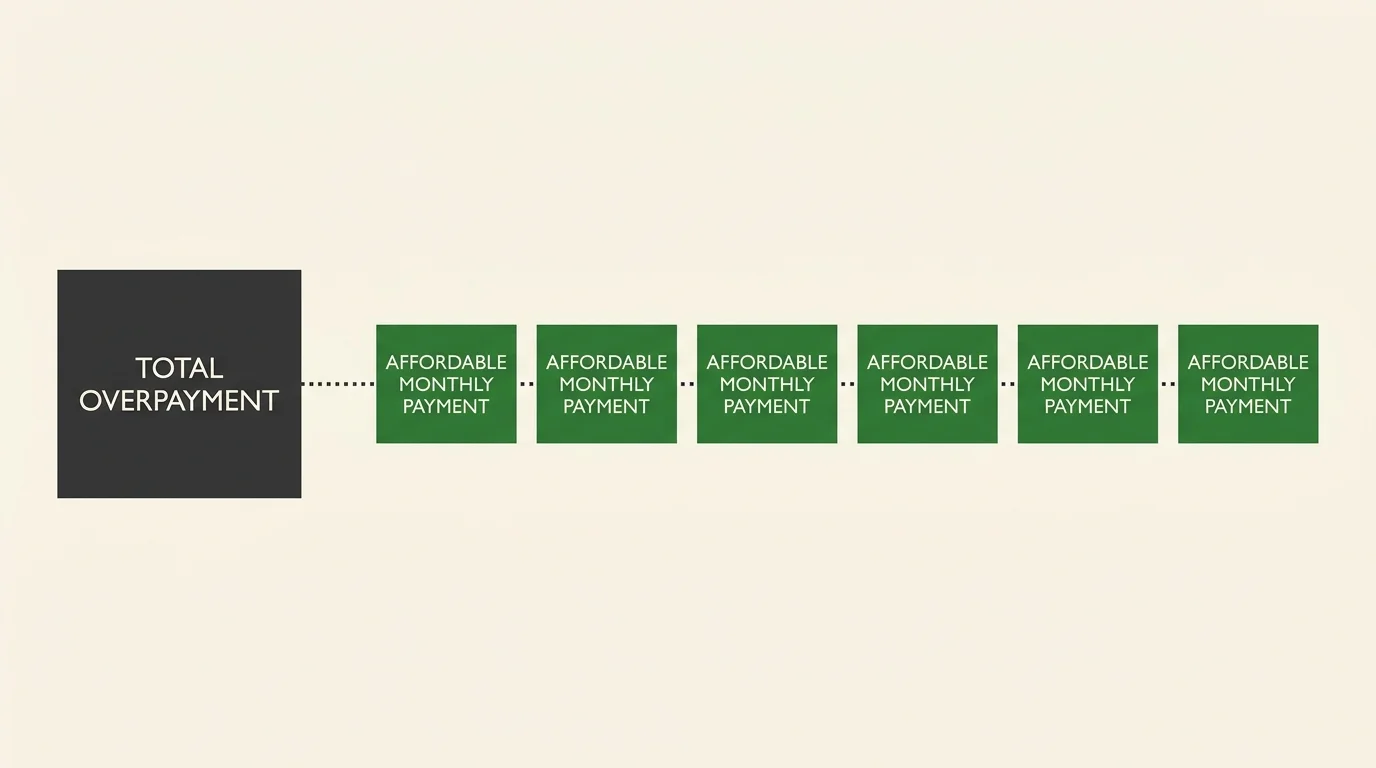

If you do not qualify for a waiver and your appeal is unsuccessful, you still have excellent options to manage the debt without sacrificing your peace of mind. Standard repayment rules dictate that the agency wants their money back, but they are increasingly flexible about how they collect it. Historically, the agency might have attempted to withhold 100 percent of your monthly check until the debt was satisfied. Fortunately, a major policy shift enacted in March 2024 completely changed this harsh practice. Now, the default maximum withholding rate is capped at just 10 percent of your total monthly benefit.

This 10 percent cap ensures that you continue receiving the vast majority of your expected income, safeguarding your retirement finances from sudden collapse. Furthermore, if even a 10 percent reduction causes you genuine hardship, you have the right to negotiate an even lower monthly payment. You can contact your local office to explain your budget constraints and propose a longer-term repayment schedule that stretches out up to 60 months. By proactively reaching out and communicating your financial reality, you dictate the terms of your repayment rather than letting the agency dictate them to you.

Tip #6: Maintain Meticulous Records of Your Communications

Navigating a Social Security overpayment requires treating your documentation like gold. Every time you call the agency, visit a field office, or send an email, create a dedicated entry in a notebook. Write down the date, the exact time of your conversation, the name of the representative you spoke with, and their direct extension if they provide one. Always ask for a confirmation number for any forms you submit over the phone or online. Having a detailed paper trail is your best defense if paperwork gets lost in the system or if a representative gives you conflicting information down the line.

Organize your physical documents in a single, secure folder. Keep a copy of the original SSA notice, copies of every form you submit, your certified mail receipts, and any subsequent letters you receive. If you ever need to escalate your case to a supervisor or seek outside assistance, handing over a neatly organized log of your communications instantly establishes your credibility. It shows that you are organized, responsible, and fully engaged in resolving the issue. Good record-keeping dramatically reduces your stress because you never have to rely on your memory alone when complex questions arise.

Tip #7: Update Your Personal Information Promptly to Prevent Future Issues

Once you successfully resolve your current notice, your next goal is to prevent the situation from ever happening again. Overpayments almost always stem from outdated information lingering in the federal system. You have the power to stop these issues at the source by keeping your personal profile rigorously updated. If you take on a part-time job to supplement your retirement finances, report your estimated earnings immediately. If you get married, divorced, or experience the passing of a spouse, notify the agency without delay, as these life events directly impact your benefit calculations.

The easiest way to manage your information is by creating and actively using a secure “my Social Security” account online. This portal allows you to review your current benefit details, update your direct deposit information, and check for any outstanding alerts directly from your computer or smartphone. Make it an annual habit to log in and verify that your address, income estimates, and personal details are completely accurate. Taking this proactive stance empowers you to enjoy your benefits safely, knowing you have minimized the risk of future administrative surprises.

The Takeaway: Living a More Blissful Retirement

Receiving an overpayment letter is undoubtedly stressful in the moment, but it is entirely manageable when you approach it with a clear head and a solid strategy. You hold significant power in this process, whether you are asserting your rights through an appeal, requesting a hardship waiver, or negotiating a gentle repayment plan under the newly improved repayment rules. Your retirement years are meant to be a time of joy, exploration, and relaxation. By facing this administrative challenge head-on and utilizing the proper channels, you can quickly put the matter behind you. Trust in your ability to advocate for yourself, lean on the resources available to you, and return your focus to the blissful, fulfilling retirement you have worked so hard to achieve.

Frequently Asked Questions

Will an overpayment notice instantly stop my current monthly checks?

No, your checks will not stop instantly. The agency must give you written notice before taking any action. If you file an appeal or request a waiver within 30 days of receiving the letter, they will pause any collection efforts until they make a final decision on your case. This grace period gives you the breathing room you need to organize your retirement finances and respond properly.

What happens if I simply ignore the letter?

Ignoring the notice is the one action you should avoid. If you do not respond, the agency will eventually begin recovering the money by withholding a portion of your monthly Social Security benefits. Under the new 2024 guidelines, they will generally withhold 10 percent of your monthly check by default. In extreme cases of ignored debt, they can intercept federal income tax refunds or garnish your wages if you are still working.

Can I hire professional help to resolve a complex overpayment case?

Absolutely. If your case involves a massive sum of money or spans several years of complex earning history, seeking professional guidance is a very smart move. Many older adults find immense relief by consulting with a specialized attorney or a representative from a local Legal Aid society. These professionals deeply understand the inner workings of the system and can file appeals or hardship waivers on your behalf.

How far back can the government go to collect an overpayment?

There is generally no statute of limitations for the government to collect an established overpayment debt. They can recover funds from mistakes that happened many years ago. This is precisely why it is so important to address the SSA notice the moment it arrives. Facing the issue promptly ensures you can access recent records and handle the repayment on your own terms, protecting your long-term financial stability.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply