Tip #4: Factor in Your Break-Even Point

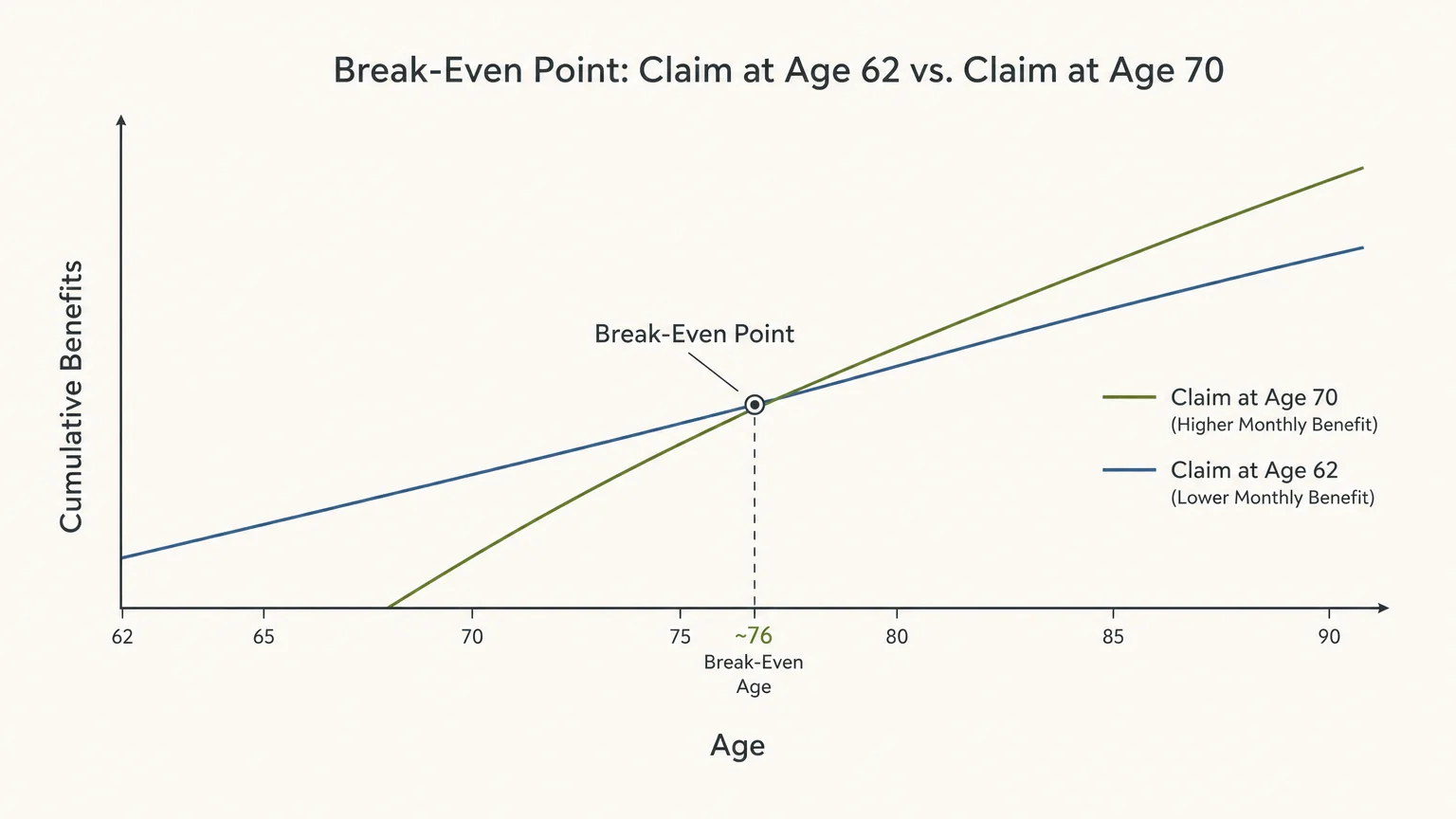

Comparing early and delayed claims requires you to deeply examine the mathematical concept of the break-even point. The break-even point highlights the exact age when the total accumulated dollars from a delayed, higher payout finally surpass the total accumulated dollars from an early, lower payout. Knowing this crossover age allows you to frame your final decision around realistic life expectancy rather than just monthly amounts.

When you claim at 62, you receive eight full years of monthly checks before the 70-year-old claimant receives a single dime. Those eight years of early income create a massive, undeniable financial head start. If you receive fourteen hundred dollars a month starting at 62, you collect over one hundred and thirty-four thousand dollars by the time you reach your seventieth birthday.

The person who bravely waited until 70 must live long enough for their larger monthly checks to make up for that lost time and missed income. In most standard scenarios, the break-even age falls somewhere between 78 and 82. If you expect to live vibrantly well into your late eighties or nineties, delaying to 70 provides far more total wealth over your lifetime.

Conversely, if chronic health issues suggest a significantly shorter life expectancy, claiming early ensures you actually get to enjoy the money you paid into the system over your working career. Understanding the break-even math prevents you from making a purely emotional choice, anchoring your strategy in practical, long-term realities.

Leave a Reply