Safeguarding your hard-earned nest egg ensures profound peace of mind when sudden economic shifts threaten your financial stability. By proactively adjusting your financial planning strategies today, you can confidently weather any market downturn without ever sacrificing your lifestyle. A retirement recession does not have to derail your dreams of traveling, supporting loved ones, or enjoying leisurely days. Economic cycles are entirely natural; preparing for them simply requires a few calculated adjustments to your retirement savings and income streams. You have already done the difficult work of accumulating wealth over your lifetime. Now, focusing on strategic recession planning allows you to protect those valuable assets and maintain absolute control over your retiree finances.

Tip #1: Build a Robust Cash Reserve for Immediate Needs

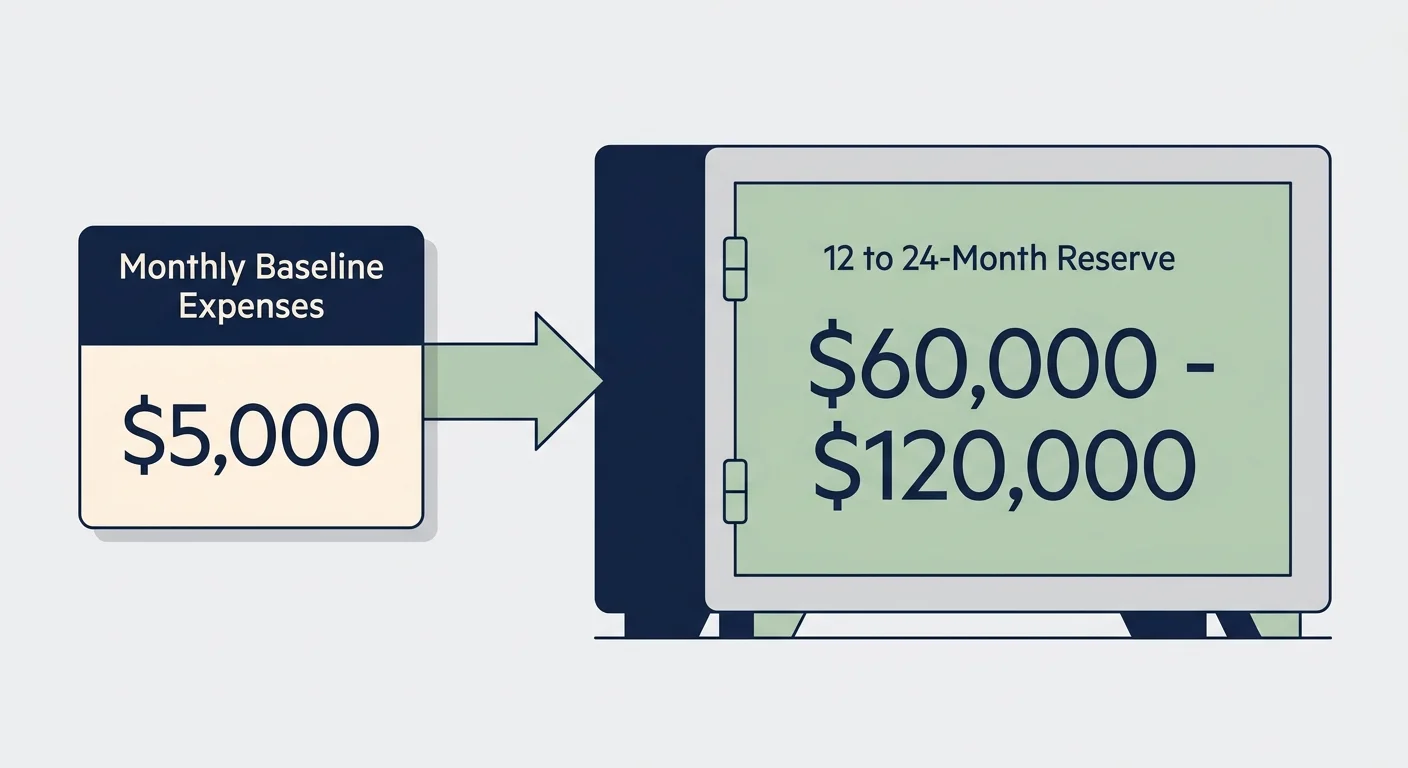

To avoid selling your long-term investments during a sudden market downturn, you must secure highly liquid assets to cover your immediate living expenses. Financial experts generally recommend that retirees keep one to two years of essential living expenses entirely in cash or cash equivalents. This protective strategy creates a vital buffer between your daily life and Wall Street volatility; it ensures you never have to liquidate stocks when equity prices plunge.

Consider utilizing high-yield savings accounts, short-term certificates of deposit, or secure money market funds to store this cash. These reliable vehicles offer safety and often yield enough interest to help combat inflation. Calculate your essential annual expenses—such as your housing, food, utilities, and healthcare—to determine exactly how much cash you require on hand. For example, if your baseline living expenses total five thousand dollars a month, aiming for sixty thousand to one hundred twenty thousand dollars in liquid savings provides incredible peace of mind. With a solid cash reserve firmly in place, a retirement recession simply becomes background noise rather than a legitimate threat to your retiree finances. You retain the absolute freedom to let your long-term investments recover naturally.

Tip #2: Rebalance and Diversify Your Investment Portfolio

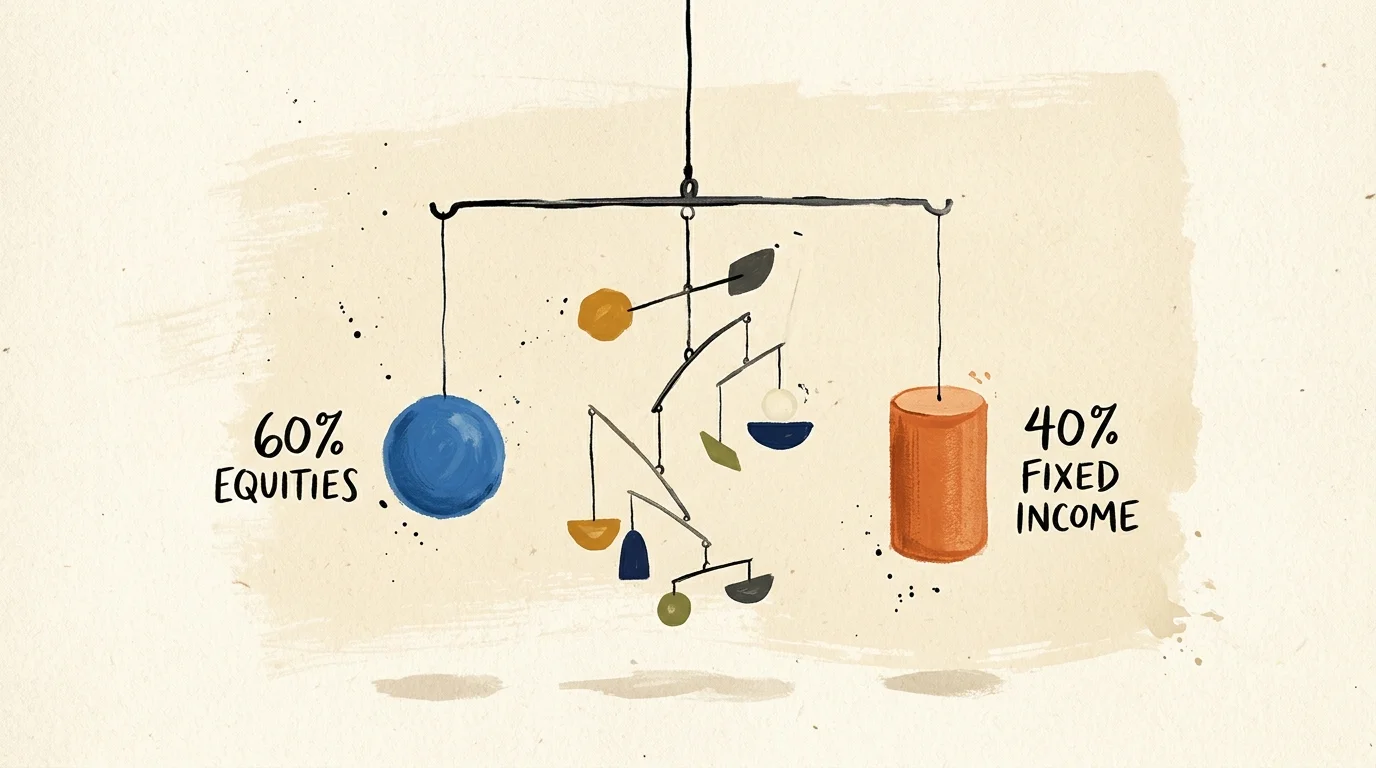

A thriving, prolonged bull market often inflates the value of equities, which can quietly skew your original asset allocation and expose you to unnecessary risk. Rebalancing your portfolio involves intentionally selling some of your high-performing stocks and purchasing more conservative assets like bonds or fixed-income securities. You want your retirement savings to reflect your current risk tolerance and timeline, not the aggressive growth targets you held in your thirties.

Revisit the classic balanced portfolio—allocating sixty percent to equities and forty percent to fixed income—as a starting baseline, but adjust it according to your specific financial planning needs. Ensure your equities are broadly diversified across different economic sectors and global geographies so that a targeted industry slump does not decimate your wealth. Solid recession planning demands you review these critical allocations at least annually. Adding high-quality, dividend-paying stocks can also be an incredibly smart move. Established companies with a strong history of paying consistent dividends often demonstrate remarkable resilience during economic slowdowns. They supply you with a steady, reliable stream of passive income, cushioning the blow if overall share prices temporarily decline.

Tip #3: Eradicate High-Interest and Variable Rate Debt

Carrying debt into your golden years is increasingly common, but entering an economic downturn with high-interest obligations can severely strain your monthly budget. Credit card balances and adjustable-rate loans act as a massive, continuous drain on your resources, especially when inflation or interest rates remain elevated. Prioritize paying down these toxic, wealth-destroying debts immediately.

By eliminating a lingering credit card balance that charges twenty percent interest, you effectively guarantee yourself a twenty percent return on your money—a feat virtually impossible to achieve consistently in the stock market. If you hold a mortgage, carefully evaluate whether paying it off completely aligns with your overarching goals. While a low, fixed-rate mortgage might not demand immediate liquidation, wiping out your monthly housing payment dramatically lowers your baseline living expenses. This strategic reduction gives you immense flexibility if your investment income unexpectedly shrinks. Consolidating smaller, high-interest debts into a single, lower-interest personal loan can also streamline your monthly cash flow. This maneuver leaves far more capital available to fund your desired lifestyle and bolster your emergency cash reserves.

Tip #4: Stress-Test Your Monthly Withdrawal Strategy

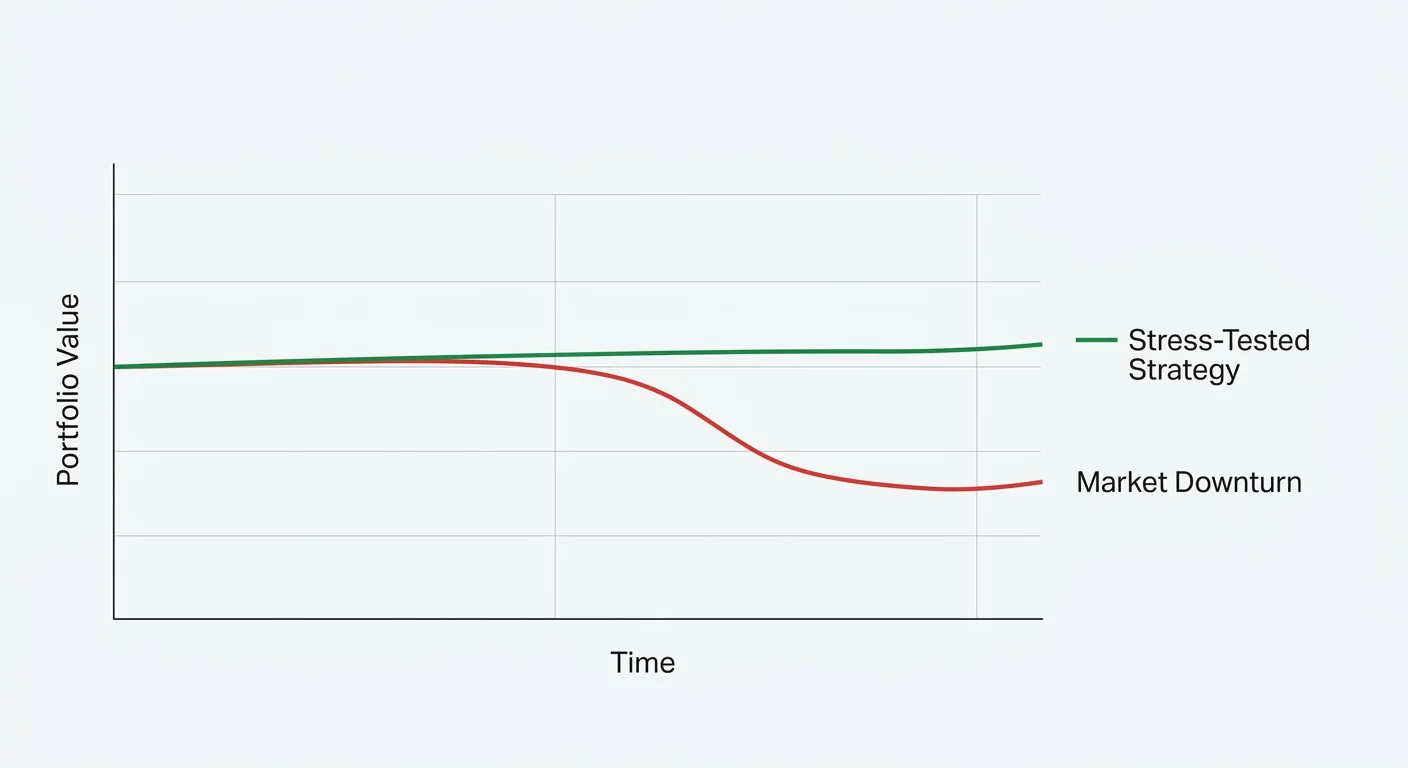

The famous four percent rule offers a fantastic mathematical starting point for retirement withdrawals, but a rigid, unyielding adherence to it during a recession can spell financial disaster. Stress-testing your withdrawal rate means running hypothetical scenarios to see exactly how your portfolio holds up if the stock market drops by twenty or thirty percent. You need a dynamic, flexible withdrawal strategy rather than a static one.

For example, if your portfolio loses significant value during a bear market, you might decide to temporarily lower your withdrawal rate to three percent. This tactical retreat preserves your principal balance and allows your money to capture the eventual market rebound fully. Many highly successful retirees utilize a guardrail approach—setting specific portfolio thresholds that dictate exactly when to give themselves an income raise and when to tighten their belts slightly. Applying this proactive level of scrutiny to your retiree finances guarantees that you remain entirely in control of your destiny. Proactively adjusting your monthly draw preserves the longevity of your nest egg and ensures you never outlive your hard-earned money.

Tip #5: Optimize Your Guaranteed Fixed Income Streams

Relying solely on an investment portfolio introduces inherent market risk, which you can beautifully mitigate by maximizing your guaranteed fixed-income sources. Social Security benefits, private pensions, and certain fixed annuities provide a dependable financial foundation regardless of broader economic conditions. If you have not yet claimed your Social Security benefits, strongly consider delaying your application.

Every single year you wait past your full retirement age until age seventy increases your monthly payout by a guaranteed eight percent. This substantial, permanent boost acts as an incredible inflation hedge and a permanent upgrade to your baseline retirement income. If you already receive your government benefits, evaluate whether a portion of your stock portfolio should be strategically shifted into a fixed income annuity. A fixed annuity operates exactly like a personal pension; you hand over a lump sum to a highly rated insurance company in exchange for a guaranteed monthly check for the rest of your life. Establishing robust guaranteed income covers your absolute necessities—housing, healthcare, and groceries—so your market-based retirement savings only need to fund your discretionary spending and fun leisure activities.

Tip #6: Audit and Trim Your Discretionary Spending

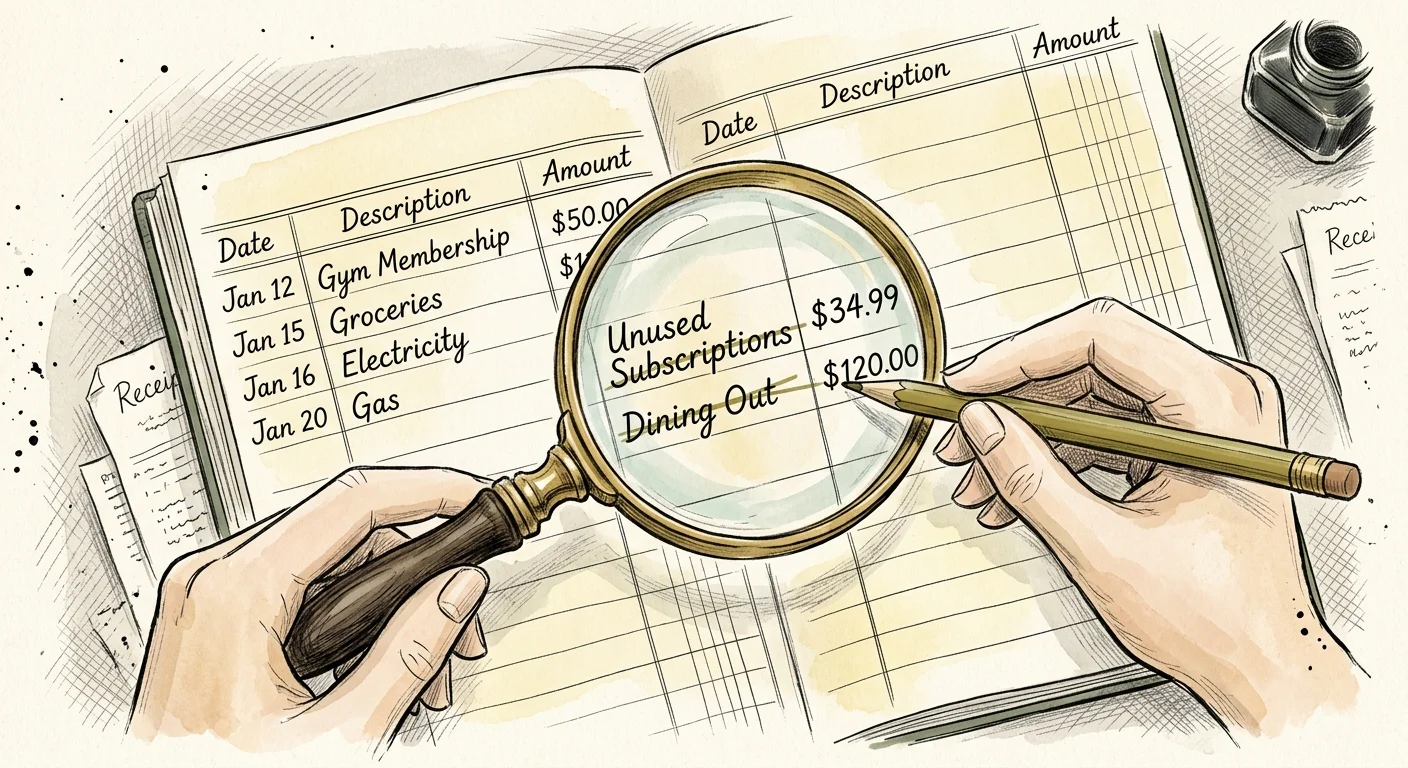

A looming recession provides the perfect, practical excuse to perform a comprehensive audit of your monthly expenses and identify areas for painless reduction. Trimming the excess fat from your budget does not mean sacrificing your happiness or locking yourself indoors; it simply involves actively prioritizing what truly brings you joy.

Sit down with your recent bank statements and clearly categorize your spending into mandatory needs versus optional wants. You will likely discover redundant digital subscriptions, excessive dining out, or creeping utility costs that you can easily eliminate. Channel the money you save directly back into your liquid cash reserve. Establishing a leaner recession budget ahead of time empowers you to flip a financial switch the exact moment the economy falters. For instance, you might seamlessly swap an expensive international vacation for a beautiful domestic road trip, or trade pricey country club meals for intimate, joyful dinner parties at home. Having this contingency plan drafted completely removes the panic from your recession planning. You will already know exactly which expenses to cut without ever feeling deprived of a rich life.

Tip #7: Plan Proactively for Rising Healthcare Costs

Healthcare stands as one of the largest and most unpredictable expenses you will face in your golden years, and general inflation often drives these medical costs significantly higher during times of economic turmoil. Fidelity Investments routinely estimates that a retired couple will need hundreds of thousands of dollars just to cover out-of-pocket medical expenses. You must proactively insulate your budget against these inevitable medical shocks.

Review your comprehensive Medicare coverage during the annual open enrollment period to ensure your specific plan still meets your evolving medical needs and covers your daily prescriptions cost-effectively. Failing to optimize your Medicare choices can easily result in thousands of dollars in wasted premiums or unexpected out-of-pocket expenses. Consider building a dedicated healthcare emergency fund entirely separate from your standard living expense buffer. If you qualified and contributed to a Health Savings Account during your working years, remember that these funds offer unparalleled triple-tax advantages for medical costs. Shielding your retiree finances from unexpected medical bills ensures that a sudden illness or physical injury does not force you to liquidate your precious investments at the absolute bottom of a market cycle.

Tip #8: Explore Passion Projects That Generate Extra Income

Retirement officially signifies the end of your primary, stressful career, but it certainly does not mandate the total end of your earning potential. Taking on a flexible part-time job, accepting a consulting role, or monetizing a beloved hobby provides a fantastic dual benefit: it generates valuable extra cash flow and keeps you deeply, mentally engaged.

Earning an additional five hundred to a thousand dollars a month significantly relieves the immense pressure on your retirement savings. You can joyfully use this supplemental income to cover your grocery bills, fund your expensive hobbies, or continually pad your emergency cash reserve. Look for unique opportunities that offer schedule flexibility and genuine personal enjoyment. You might tutor local students in your specific area of expertise, sell beautiful handmade crafts online, consult independently for your former industry, or work two days a week at a peaceful local garden center. The ultimate goal is not to return to the exhausting daily grind, but to leverage your lifetime of valuable skills in a thoroughly low-stress environment. Cultivating this extra income stream creates a powerful financial shock absorber.

Tip #9: Collaborate With a Fiduciary Financial Advisor

Navigating the intricate complexities of recession planning, strategic tax optimization, and proper asset allocation often requires a dedicated professional perspective. Partnering with a licensed fiduciary financial advisor ensures you have a true expert in your corner who is legally obligated to act entirely in your best interest.

An experienced advisor can provide an objective, emotionless review of your current financial planning strategies, which proves absolutely invaluable when sensationalist news headlines tempt you to panic-sell your beloved investments. They possess advanced financial software to run Monte Carlo simulations—a brilliant mathematical tool that rigorously stress-tests your portfolio against thousands of potential historical market scenarios. Sit down with your chosen advisor to openly discuss your true risk tolerance, thoroughly review your estate planning documents, and explicitly confirm that your asset allocation beautifully aligns with your long-term goals. Having a trusted professional validate your personal strategy dramatically boosts your daily confidence. You can rest easy knowing that an experienced, watchful set of eyes has scrutinized your comprehensive plan. A strong advisory relationship transforms financial anxiety into profound reassurance.

The Takeaway: Living a More Blissful Retirement

Preparation inevitably breeds profound confidence. Taking proactive, thoughtful steps today to fortify your financial foundation completely neutralizes the lingering fear of an impending economic downturn. By intentionally building a substantial cash buffer, systematically eliminating toxic debt, and thoroughly optimizing your guaranteed income streams, you construct an impenetrable fortress around your retirement dreams. You have spent decades working diligently, saving responsibly, and planning meticulously for this beautiful chapter of your life.

A retirement recession is merely a temporary, passing season in the broader economic climate. With the absolute right strategy firmly in place, you can sail through it completely unscathed. Embrace these nine smart moves today so you can spend all of your tomorrows doing exactly what you love—whether that means traveling the world, volunteering passionately in your local community, or simply savoring quiet, uninterrupted mornings with your family. Your golden years are meant to be deeply joyful and expansive, not overshadowed by constant market anxiety. Take total control of your financial destiny, celebrate your brilliant preparedness, and step confidently into the future with profound optimism and grace.

Frequently Asked Questions

How long does a typical recession last, and how does it actually impact retirees?

Historically, economic recessions last anywhere from ten to eighteen months, though the subsequent stock market recovery can occasionally take slightly longer. For retirees, the absolute primary impact is the distinct threat of rapid portfolio depletion if you are suddenly forced to sell your stocks at depressed prices to cover mandatory living expenses. This mathematical reality is exactly why having highly liquid cash reserves is so crucial to your long-term success.

Should I completely avoid the stock market if a major recession is coming?

Absolutely not. Fleeing the stock market completely exposes your wealth to severe inflation risk, meaning your money will steadily lose its purchasing power over time. Stocks historically provide the necessary long-term growth required to sustain a modern retirement that could easily last thirty years. Instead of entirely abandoning equities, focus closely on appropriately diversifying your holdings and firmly ensuring your asset allocation matches your personal risk tolerance.

Is it too late to adjust my financial plan if the economy is already noticeably slowing down?

It is never too late to take active control of your comprehensive financial planning. Even if a visible downturn has already begun, you can still successfully audit your monthly budget, trim your discretionary spending, and immediately optimize your portfolio withdrawal strategy. Making smart adjustments right now will always yield far better results than doing nothing at all. Consult directly with a financial professional to determine the safest, most effective immediate moves for your specific situation.

Does inflation heavily factor into recession planning for my overall retirement savings?

Yes, inflation remains a highly critical component of any successful long-term financial strategy. During a recession, central banks frequently adjust national interest rates specifically to combat inflation. You must actively ensure your investment portfolio contains robust assets that consistently outpace inflation over time, such as high-quality equities and certain real estate investments, while simultaneously maintaining enough stable fixed-income assets to comfortably cover your immediate, daily expenses.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply