Choosing the right Social Security claiming age is the single most powerful lever you have to maximize your guaranteed retirement income. By understanding the profound financial differences between claiming Social Security at 62 versus waiting until 70, you empower yourself to build a strategy that perfectly supports your lifestyle goals.

Claiming early offers immediate access to cash for travel or early retirement, while delaying guarantees the absolute highest monthly payout to protect against inflation and outliving your savings. Navigating this decision requires looking closely at your health, your savings, and your long-term vision. The following side-by-side breakdown gives you the clarity you need to confidently step into this exciting new chapter of your life.

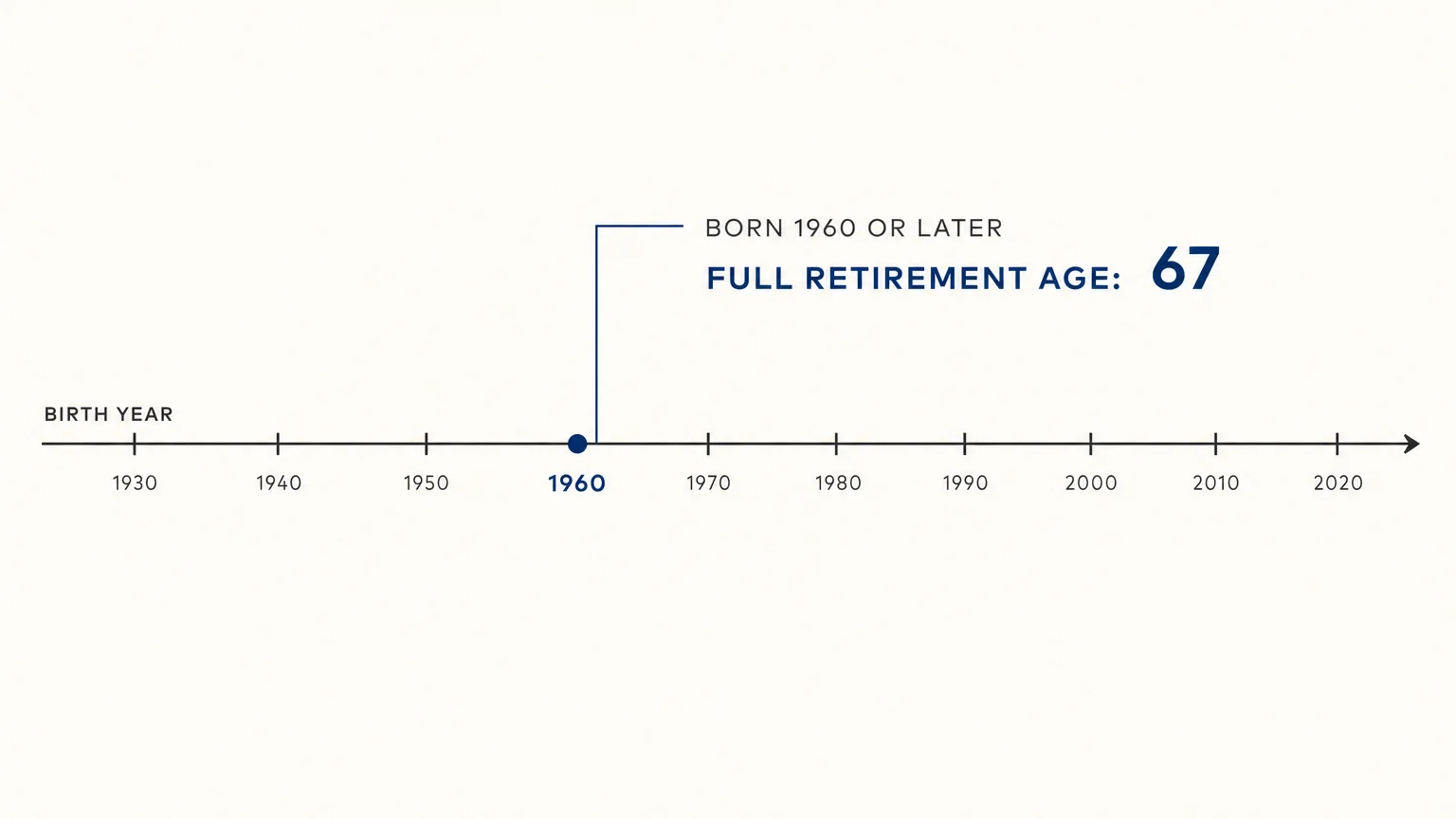

Tip #1: Understand the Baseline of Your Full Retirement Age (FRA)

Before you compare the extremes of taking benefits at the earliest or latest possible dates, you must establish your personal baseline. The Social Security Administration uses your Full Retirement Age to determine your primary insurance amount. This specific dollar figure represents the exact monthly benefit you receive if you claim at your designated target age. Depending on your birth year, your Full Retirement Age lands anywhere from 66 to 67. Anyone born in 1960 or later reaches Full Retirement Age at exactly 67.

Knowing this exact age allows you to make an accurate, informed comparison between your various options. Think of your Full Retirement Age as the foundational anchor point of your entire retirement strategy. When you claim earlier than this anchor, you face permanent financial reductions. When you delay past this anchor, you earn permanent financial increases. Without knowing your baseline, calculating your potential future income becomes a guessing game.

You can find your specific Full Retirement Age by creating a free account on the official Social Security website and viewing your personalized statement. Reviewing your statement annually helps you keep track of your earned credits and your projected payouts. Securing this foundational number gives you the confidence to start mapping out your timeline. Taking the time to verify your primary insurance amount completely transforms how you view your future financial landscape.

Many people mistakenly assume they can receive their full benefit at age 65 simply because that is the eligibility age for Medicare. Separating your Medicare timeline from your Social Security claiming age prevents incredibly costly miscalculations. You gain immense peace of mind when you build your plans around accurate, personalized data rather than outdated assumptions.

Leave a Reply