Tip #2: Calculate the Cost of Claiming Social Security at 62

Choosing to claim Social Security at 62 opens the door to immediate financial freedom, but it comes with a steep, permanent cost. The age of 62 represents the absolute earliest opportunity you have to start receiving your retirement benefits. Stepping away from the workforce at this age gives you the precious time and energy to travel the world, pursue neglected hobbies, or spend irreplaceable years watching your grandchildren grow.

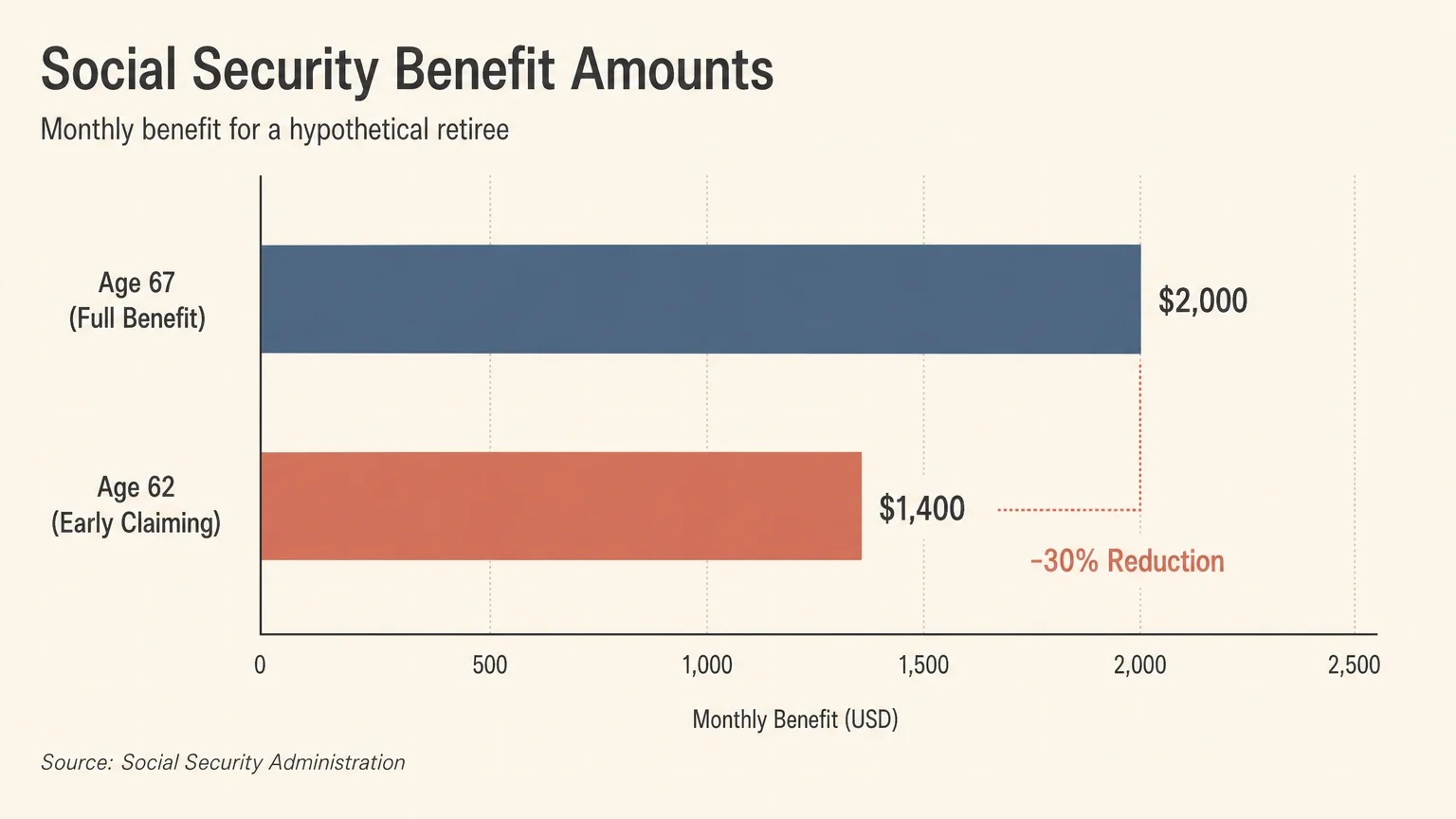

However, the system reduces your monthly payout significantly for every single month you claim before reaching your Full Retirement Age. If your Full Retirement Age is 67, claiming at 62 slashes your monthly checks by a full 30 percent. If your primary insurance amount sits at two thousand dollars, claiming at 62 drops your actual monthly income to just fourteen hundred dollars. You must accept this reduced amount for the rest of your life; it does not automatically reset to the higher amount when you turn 67.

You must also closely consider the annual earnings limit if you plan to continue working while receiving early benefits. The government withholds a portion of your benefits if your income from a job exceeds a specific threshold prior to your Full Retirement Age. This temporary withholding often catches ambitious part-time workers entirely by surprise, disrupting their expected cash flow.

Claiming at 62 works best if you plan to fully retire immediately, have significant health concerns that limit your life expectancy, or possess enough supplementary investments to offset the smaller monthly checks. If you have built a massive nest egg and simply want the government to start paying you back as soon as possible, claiming early provides a steady, immediate stream of supplemental cash.

Leave a Reply