Tip #2: Maximize Your Lifetime Earnings for a Bigger Check

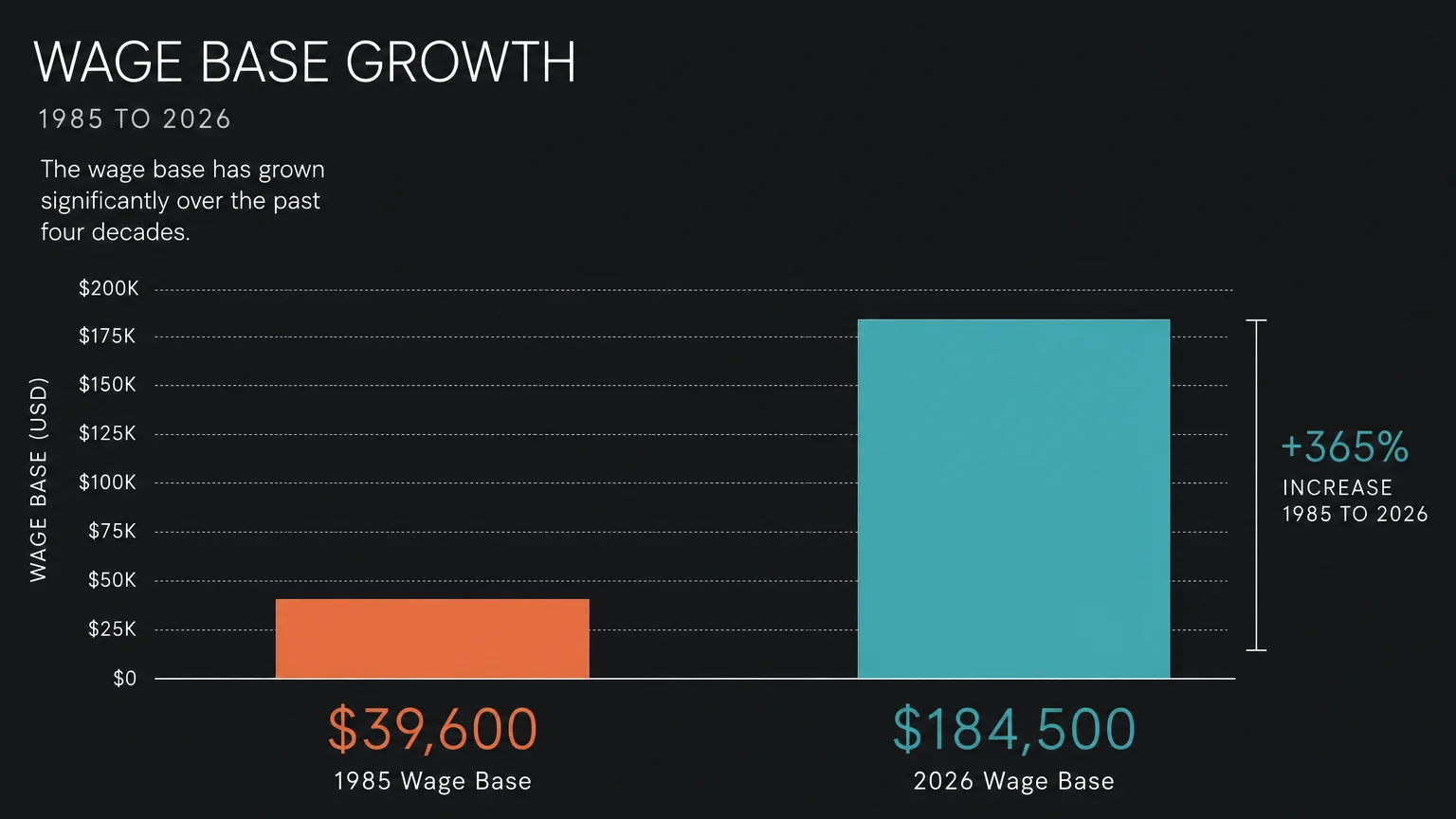

Decades ago, achieving the maximum Social Security benefit required a very different salary trajectory. In 1985, the Social Security taxable wage base—the maximum amount of your income subject to Social Security taxes—sat at $39,600. If you earned above that threshold, you stopped paying into the system for the remainder of the year. Fast forward to 2026, and that wage base has skyrocketed to $184,500. This dramatic shift highlights how wages have grown, but it also reveals a powerful strategy for boosting your own monthly check.

The Social Security Administration calculates your primary insurance amount using your highest 35 years of indexed earnings. If you do not have a full 35-year work history, the government inserts zeros for the missing years. Those zeros drag down your average and permanently shrink your benefit. Conversely, replacing low-earning years with high-earning years actively increases your future payments.

You hold the power to shape this calculation. If you took time away from the workforce to raise children or care for aging parents, consider working a few extra years in your sixties. Even a fun, part-time job or a lucrative side hustle can replace a zero-income year on your permanent record. Every dollar counts toward pushing your average higher.

Furthermore, routinely check your earnings record on the official Social Security website. Mistakes happen; an employer might misreport your income, or a clerical error could cheat you out of valuable credits. Correcting a missing year of income guarantees you receive every penny you deserve. Treat your earnings record like a vital financial document, because it directly dictates the outcome of any future Social Security payment comparison you might run.

Take a proactive approach to your career’s twilight years. Many older adults discover that transitioning into consulting or freelance work offers both mental stimulation and a solid financial payoff. When you continue working, you continue paying into the system, steadily raising your lifetime average. Over time, pushing out those low-earning years from your twenties or thirties yields a surprisingly robust increase in your baseline benefit. Your earning power remains a valuable tool, so use it strategically to maximize your golden years.

Thank you. Very informative.

Except that those 479 USD in 1985 had much more purchasing power that these 1,976 USD in 2026.

Exactly, who’s do the think they are kidding.

Thanks

To people who get disabled prior to retirement when you change over from disability to retirement you get the shaft because disability is based on the previous 10 years of income and when you turn 65 thats all you get credit for on your SSI thats thanks to the stupid law that got passed when he was president

How do you get 1976.00 per month? I don’t get anywhere near that.

Another big difference is that SS didn’t get taxed back then. Regardless of what they say, I’m paying income taxes on SS

I think my social security benefit is less than I supposed to be. could you take a look? thanks!

I’m not sure what location this writer lives in but you can’t even get a one bedroom apartment for that tiny monthly payment. We get forced into paying into the system and then not given enough money to live on. Welcome to Socialism that never works.

I am without job and have not been receiving any help from social security.

My socials security monthly amount has not changed

my social security monthly has not changed