The gap between the $479 average Social Security check of 1985 and the robust $1,976 payment in 2026 illustrates how benefits adapt to protect your purchasing power. Understanding these historical leaps empowers you to make smarter choices about your retirement timeline.

You hold the keys to unlocking a higher monthly benefit by mastering the system’s modern rules. While the world has changed dramatically since the mid-eighties, the core promise of financial security remains intact.

By leveraging today’s expanded earnings limits, annual cost-of-living adjustments, and strategic claiming ages, you can actively maximize your lifetime income.

Let us explore these striking differences and discover practical ways to optimize your financial future.

Tip #1: Embrace the Power of the Cost-of-Living Adjustment (COLA)

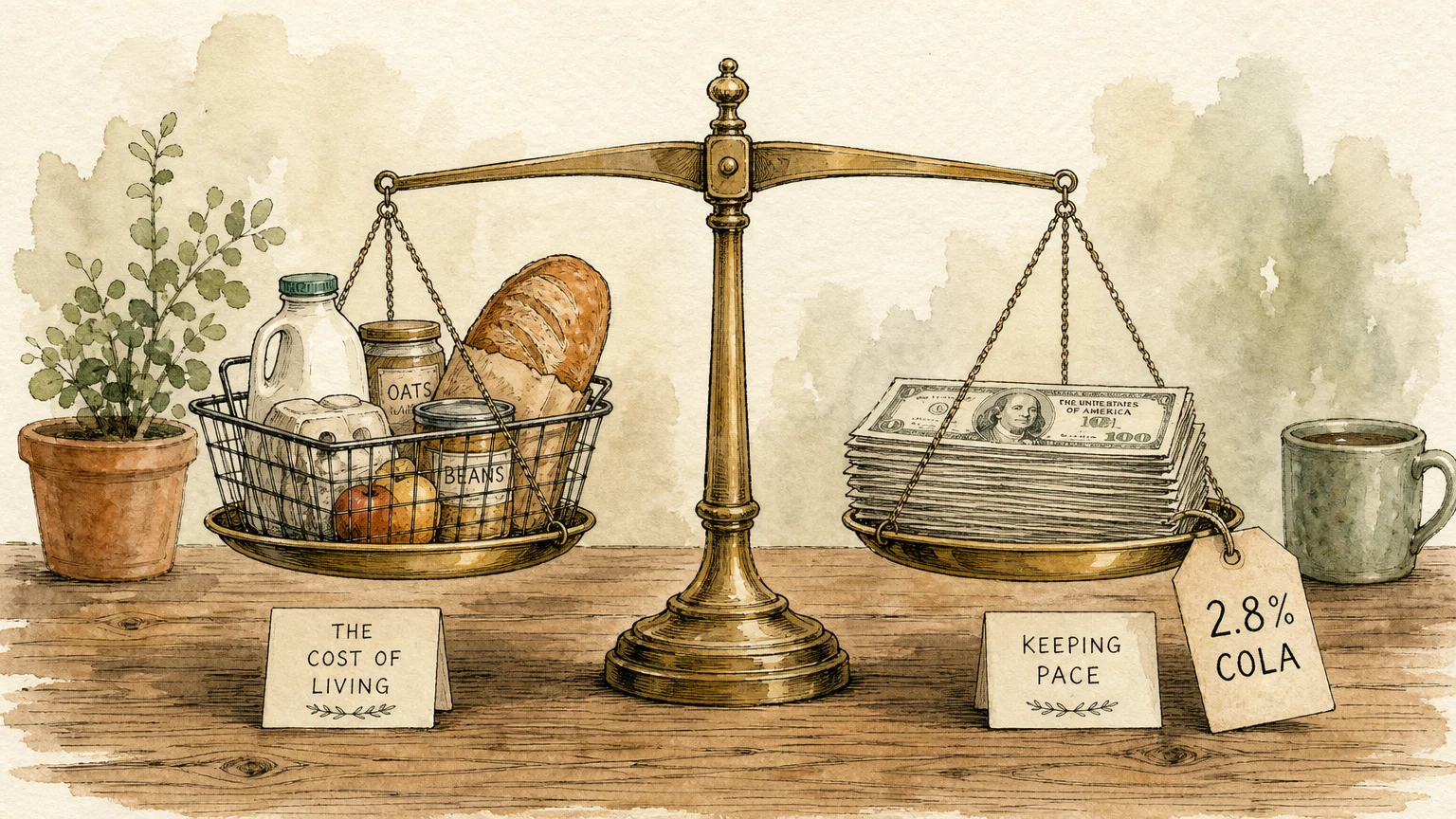

Look closely at the numbers, and you quickly realize the sheer impact of inflation over forty years. In 1985, the Social Security Administration distributed an average monthly benefit of just $479 to retired workers. Back then, a gallon of gas cost around a dollar, and rent took a much smaller bite out of the household budget. Today, the economic landscape looks entirely different; thankfully, your benefits have evolved alongside it. Looking at Social Security 2026 data, following a 2.8% Cost-of-Living Adjustment (COLA), that average Social Security payment surged to approximately $1,976 per month.

You can thank the annual COLA for this essential growth. Introduced automatically in 1975, the COLA ensures your buying power does not erode as the cost of groceries, utilities, and healthcare climbs. The government recalculates this adjustment every October using the Consumer Price Index for Urban Wage Earners and Clerical Workers. When inflation rises, your monthly check increases to help bridge the gap. Without this vital feature, a fixed $479 payment would leave modern retirees struggling to pay even a fraction of their monthly bills.

To make the most of this system, actively factor the annual COLA into your financial planning. Instead of guessing your future income, wait for the official October announcement to adjust your household budget for the upcoming year. Use this yearly bump as an opportunity to review your spending habits. Allocate the extra funds toward essential needs like prescriptions or utility bills, ensuring your most critical expenses remain fully funded.

Keep in mind that rising Medicare Part B premiums often absorb a portion of your COLA increase. Because the government automatically deducts Medicare premiums from your Social Security check, a premium hike can take a bite out of your net gain. Review your year-end benefit statements carefully to understand exactly how much extra cash will actually hit your bank account in January. By tracking these numbers, you maintain total control over your monthly cash flow and prevent unexpected budget shortfalls.

Thank you. Very informative.

Except that those 479 USD in 1985 had much more purchasing power that these 1,976 USD in 2026.

Exactly, who’s do the think they are kidding.

Thanks

To people who get disabled prior to retirement when you change over from disability to retirement you get the shaft because disability is based on the previous 10 years of income and when you turn 65 thats all you get credit for on your SSI thats thanks to the stupid law that got passed when he was president

How do you get 1976.00 per month? I don’t get anywhere near that.

Another big difference is that SS didn’t get taxed back then. Regardless of what they say, I’m paying income taxes on SS

I think my social security benefit is less than I supposed to be. could you take a look? thanks!

I’m not sure what location this writer lives in but you can’t even get a one bedroom apartment for that tiny monthly payment. We get forced into paying into the system and then not given enough money to live on. Welcome to Socialism that never works.

I am without job and have not been receiving any help from social security.

My socials security monthly amount has not changed

my social security monthly has not changed