Maximizing your retirement income means knowing exactly which funds you can collect without triggering the Social Security earnings test. If you claim your benefits before reaching full retirement age, you can still bring in substantial cash from specific sources—like investments, pensions, and real estate—without losing a single dime of your monthly check. Understanding the difference between earned wages and passive revenue allows you to build a robust financial safety net while fully protecting your Social Security benefits. By strategically tapping into these eleven approved funding streams, you gain the freedom to travel, invest in hobbies, and enjoy your golden years without worrying about arbitrary income limits or sudden reductions in your government payments.

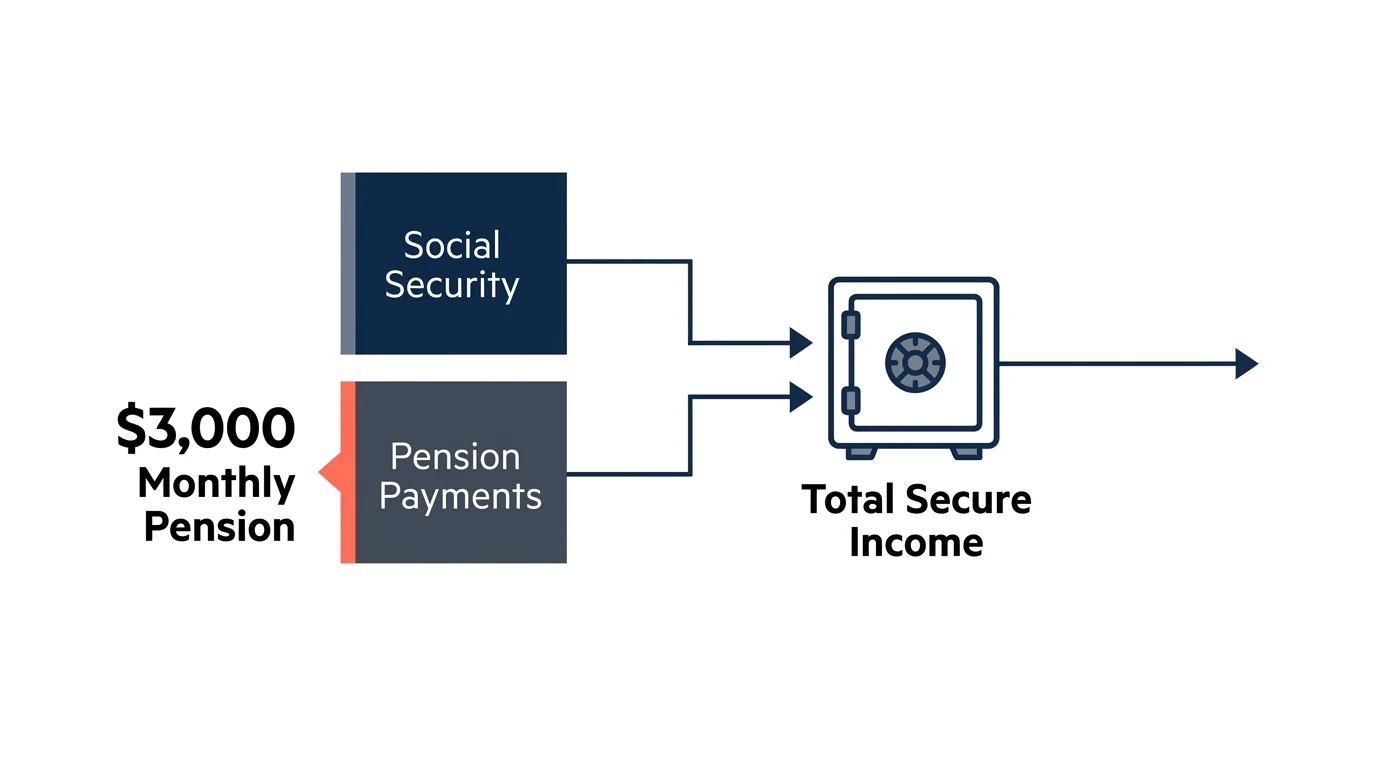

Tip #1: Pension Payments

When you transition into your golden years, a traditional pension serves as a reliable anchor for your everyday finances. Social Security categorizes defined-benefit pensions as non-work income, meaning you can collect substantial monthly payouts from a former employer without ever threatening your Social Security benefits. For instance, if you worked as a teacher or a corporate executive and secured a $3,000 monthly pension, the Social Security Administration completely ignores this amount when calculating your annual earnings limit. Many public sector pensions also include built-in cost-of-living adjustments, which aggressively protect your purchasing power against inflation over the long haul. Because the government classifies these payouts strictly as non-earned income, you can confidently rely on this money to pay your mortgage or fund your travel plans. You should review your summary plan description to understand exactly how your pension pays out over time. Sometimes, electing a joint-and-survivor option slightly reduces your initial monthly payout but guarantees your spouse will continue receiving funds later; a strategic move that provides crucial peace of mind for your shared future.

Tip #2: Annuity Payouts

Purchasing an annuity effectively allows you to build your own personal pension, and the IRS views these distributions as entirely separate from earned wages. Whether you hold a fixed, variable, or indexed annuity, the monthly checks you receive will never trigger the Social Security earnings test. Imagine you rolled a portion of your savings into an immediate annuity that guarantees $1,500 a month for life. None of that $18,000 annual passive income counts against your Social Security limit. This makes annuities a highly effective tool for bridging the gap between your essential living expenses and your guaranteed retirement income. To leverage this strategy successfully, work with a fiduciary financial advisor to shop around for the most competitive annuity rates available in the marketplace. Prioritize products with low administrative fees and strong provider ratings to ensure your investment remains completely secure for decades to come.

Tip #3: IRA and 401(k) Distributions

Many older adults mistakenly assume that pulling money out of their retirement accounts counts as current income in the eyes of the Social Security Administration. Fortunately, distributions from traditional IRAs, Roth IRAs, 401(k)s, and 403(b)s strictly qualify as investment withdrawals rather than earned wages. You can safely withdraw $50,000 or even $100,000 from your 401(k) to fund a dream vacation, renovate your kitchen, or cover unexpected medical bills without facing a single deduction from your Social Security checks. However, you must stay mindful of the broader tax implications associated with these accounts. While traditional 401(k) withdrawals trigger ordinary income taxes and potentially increase your Medicare premiums, they still fly completely under the radar of the Social Security earnings threshold. If you want to maintain complete control over your tax bracket, pulling funds from a Roth IRA represents the ultimate strategy. Roth withdrawals are entirely tax-free and invisible to the government when assessing your income.

Tip #4: Dividend Yields from Stocks

Building a robust portfolio of dividend-paying stocks offers an excellent pathway to generating steady passive income throughout your post-career life. Companies that consistently distribute a portion of their profits to shareholders provide a growing income stream that the government classifies strictly as investment returns. If you hold shares in established blue-chip companies or broad market index funds, your quarterly dividend checks will not reduce your Social Security benefits, regardless of how much wealth you accumulate. For example, a $300,000 portfolio with a 4 percent dividend yield generates $12,000 in annual cash flow. You can use this money to cover everyday bills or systematically reinvest it to purchase more shares. Look into “Dividend Aristocrats”—companies that have steadily increased their shareholder payouts for 25 consecutive years—to establish a highly reliable and inflation-resistant component of your overall retiree finances.

Tip #5: Interest from Bonds and Savings Accounts

In today’s shifting economic landscape, conservative investments like certificates of deposit (CDs), Treasury bonds, and high-yield savings accounts deliver impressive returns with virtually zero risk to your principal balance. The interest you accumulate through these secure vehicles qualifies as unearned income, keeping your Social Security benefits perfectly intact. If you park $100,000 in a high-yield savings account earning 4.5 percent, you effortlessly generate $4,500 over the course of a single year. To maximize this opportunity, consider building a CD or Treasury ladder. By purchasing bonds that mature at staggered intervals—such as three, six, nine, and twelve months—you ensure continuous access to liquid cash while simultaneously locking in competitive interest rates. Exploring municipal bonds can also provide you with interest income that is often entirely exempt from federal taxes, further shielding your hard-earned wealth from unnecessary erosion.

Tip #6: Capital Gains from Asset Sales

Downsizing your primary home or selling off a profitable stock portfolio represents a massive influx of cash, but you can breathe easy knowing these transactions fall completely outside the scope of the Social Security earnings test. Capital gains result from the natural appreciation of an asset over time, not from physical labor or active employment. If you sell a rental property and net a $150,000 profit, or if you liquidate a highly appreciated mutual fund, the Social Security Administration ignores this windfall when verifying your income limits. Take advantage of this clear rule to optimize your living situation. If maintaining a large family home feels burdensome, selling it allows you to unlock significant equity, move to a more manageable space, and utilize the surplus funds to travel or invest. Remember to review the primary home exclusion rules; single filers can typically exclude up to $250,000 of capital gains from the sale of a primary residence, keeping the lion’s share of your equity in your pocket.

Tip #7: Rental Property Income

Owning real estate stands out as one of the most lucrative and reliable ways to fund your post-career lifestyle. As long as you do not work as a licensed real estate professional who actively manages properties as a primary business, your monthly rent checks classify exclusively as passive income. Whether you rent out a cozy vacation cabin, a spare bedroom, or a multi-family apartment building, this revenue bypasses the Social Security earnings penalty entirely. A retiree collecting $2,000 a month from a residential rental property enjoys a $24,000 annual boost to their standard of living without jeopardizing their government benefits. To make this income stream truly passive, consider hiring a reliable local property management company. While they typically charge a fee of 8 to 12 percent of the monthly rent, they expertly handle tenant screening, maintenance requests, and rent collection; freeing you up to fully enjoy your newfound freedom without the headaches of being a landlord.

Tip #8: Inheritances and Trust Fund Distributions

Receiving an inheritance often comes during a difficult time of personal loss, but you do not need to worry about it negatively impacting your carefully established retirement income. The Social Security Administration explicitly exempts inherited assets—whether you receive a sudden lump sum of cash, an inherited IRA, or ongoing monthly distributions from a family trust. Because this wealth stems from a transfer of assets rather than active employment or hourly labor, your Social Security benefits remain completely shielded. If you find yourself managing an unexpected inheritance, take the time to consult an estate planning attorney or a fiduciary financial advisor. They can help you invest the windfall strategically, perhaps allocating funds toward long-term care insurance, high-yield dividend funds, or aggressive debt elimination, ensuring the legacy you received supports your financial well-being for decades to come.

Tip #9: Unemployment Compensation

Many seniors choose to work part-time or consult during their early retirement years to stay mentally sharp, socially active, and financially engaged. If you take on a part-time job and subsequently lose it through no fault of your own, you maintain the absolute legal right to file for unemployment benefits. The government considers unemployment compensation as a temporary safety net rather than earned wages, meaning these weekly checks will not count toward your Social Security earnings limit. For instance, if you receive $400 a week in state unemployment benefits while diligently searching for a new part-time role, your Social Security checks continue without any interruption. This valuable exemption provides a critical financial buffer, allowing you to bridge the gap between jobs without forcing you to dip prematurely into your 401(k) or personal savings accounts.

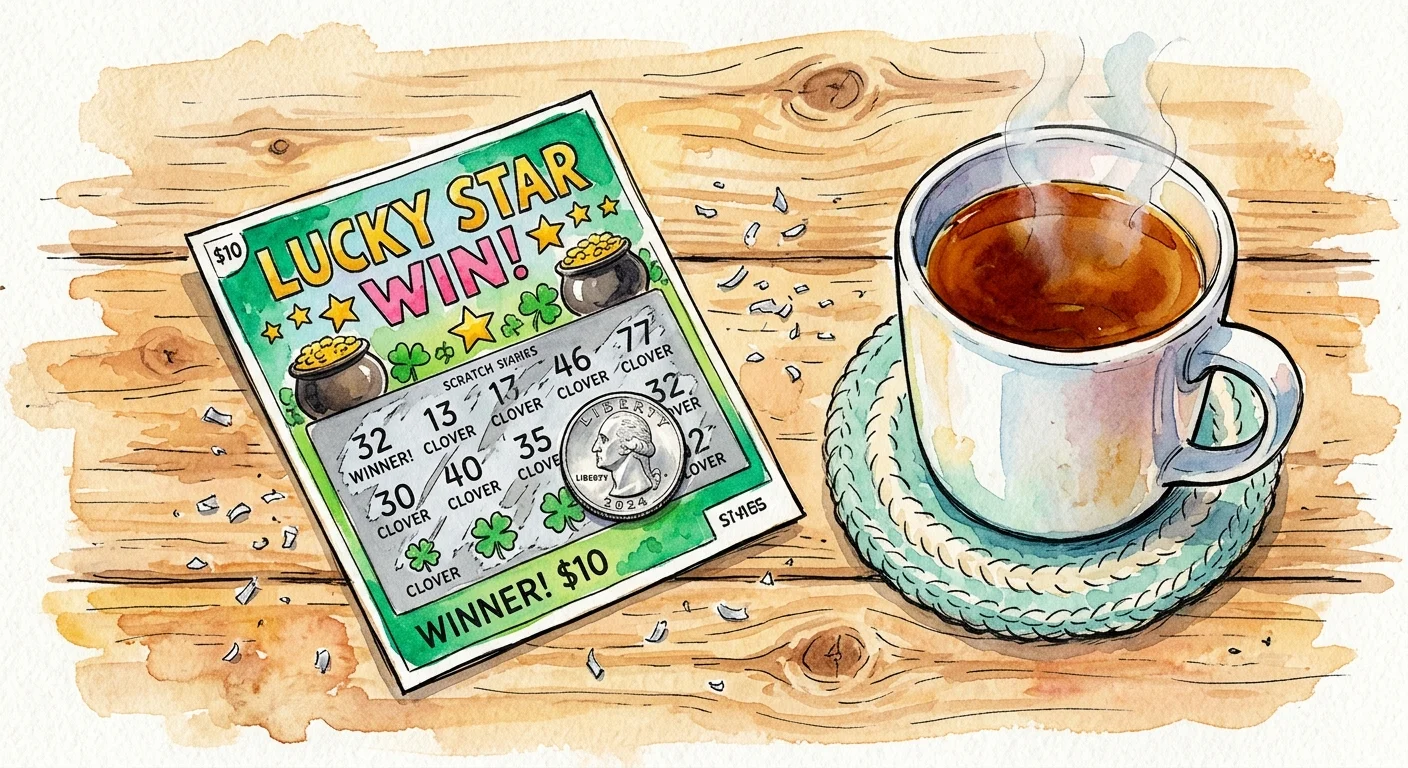

Tip #10: Lottery Winnings and Prize Money

While winning the lottery or hitting a massive jackpot at the casino relies entirely on luck, the financial mechanics behind how these funds interact with your retirement benefits remain crystal clear. Prize money, casino payouts, and lottery winnings qualify strictly as unearned income. If you happen to win $10,000 on a scratch-off ticket or take home a substantial cash prize from a nationwide sweepstakes, your Social Security payments stay completely protected from any earnings-related reductions. Naturally, you must still report these winnings to the IRS, as the federal government and most state governments subject gambling profits to standard income taxes. Remember to keep meticulous records of any gambling losses; tax laws often allow you to deduct those verified losses against your winnings, thereby heavily reducing your overall tax burden while entirely protecting your Social Security payouts.

Tip #11: Financial Gifts from Family and Friends

Generosity within a family can take many beautiful forms, and receiving financial support from your loved ones will never trigger an administrative penalty on your Social Security record. Whether your adult children help cover the cost of a luxury family cruise, gift you a reliable vehicle, or simply transfer cash into your checking account to help with mounting medical expenses, the Social Security Administration views these transactions purely as non-work revenue. Current IRS regulations allow individuals to gift up to $18,000 per year, per recipient, without even having to file a gift tax return. This means a married couple could potentially gift you up to $36,000 annually, completely tax-free. You can gracefully accept this heartfelt support with immense gratitude and absolute peace of mind, knowing your foundational retirement income remains entirely secure and unaffected.

The Takeaway: Living a More Blissful Retirement

Navigating the complex landscape of retiree finances does not have to feel like an uphill battle. By clearly distinguishing between the wages you earn through active work and the passive income you generate through savvy investments, real estate, and strategic planning, you hold the power to maximize your wealth safely. The Social Security earnings limit only applies to traditional labor; it was never designed to penalize you for making smart financial choices or building a broadly diversified portfolio. As you move forward, embrace the incredible opportunity to expand your personal revenue streams. Lean confidently into dividend-paying stocks, explore the reliable stability of fixed annuities, and do not fear tapping into the substantial home equity you built over a lifetime of hard work. When you structure your assets intelligently, you unlock a dynamic, completely stress-free lifestyle where your money works tirelessly for you—leaving you entirely free to focus on family, exciting travel, and the blissful moments that define your golden years.

Frequently Asked Questions

Do I need to worry about the Social Security earnings limit after I reach full retirement age?

No; the earnings limit disappears entirely the exact month you reach your full retirement age (FRA). Once you hit that specific milestone, you can earn an unlimited amount of money from any source—including traditional hourly wages, lucrative salary positions, and active self-employment—without facing any reduction whatsoever in your Social Security benefits.

If my Social Security benefits are reduced due to high earned income before my FRA, is that money gone forever?

Fortunately, the money withheld by the government is not lost permanently. When you finally reach your full retirement age, the Social Security Administration automatically recalculates your benefit amount to give you strict credit for the months they withheld your payments. This adjustment effectively results in a higher monthly check for the rest of your life, rewarding you for your continued hard work.

Does passive income affect the taxation of my Social Security benefits?

Yes. While passive income does not reduce your base benefit amount through the traditional earnings test, it does actively increase your “combined income.” If your combined income (calculated as your adjusted gross income plus nontaxable interest plus half of your Social Security benefits) exceeds specific IRS thresholds, up to 85 percent of your Social Security benefits may become subject to federal income taxes. You should collaborate closely with a qualified tax professional to map out a highly efficient withdrawal strategy that minimizes your tax burden.

For a wide range of resources for older adults, visit AARP and the National Council on Aging (NCOA). Health information is available from the National Institute on Aging.

Disclaimer: This article is for informational and inspirational purposes only. It is not a substitute for professional medical, financial, or psychological advice. Please consult with a qualified expert for guidance tailored to your individual needs.

Leave a Reply